In the vast and often intricate landscape of personal finance, retirement planning stands as a cornerstone for achieving long-term financial security. While many individuals are familiar with the concept of an Individual Retirement Arrangement (IRA), a lesser-known but equally powerful tool exists for married couples: the Spousal IRA. This financial vehicle, designed specifically to accommodate situations where one spouse may not have earned income, plays a crucial role in ensuring both partners can build a robust retirement nest egg. For those navigating the complexities of the financial world, understanding the nuances of a Spousal IRA is essential for maximizing savings and securing a comfortable future together.

The world of retirement accounts can feel like a digital labyrinth. From understanding tax advantages to choosing the right investment vehicles, the sheer volume of information can be overwhelming. This is where a Spousal IRA shines, offering a streamlined approach for married couples to bolster their retirement savings. Whether you’re a seasoned investor or just beginning to explore your financial options, this guide will demystify the Spousal IRA, covering its purpose, eligibility, contribution limits, and the significant benefits it offers. We’ll also touch upon how it integrates with broader financial planning strategies, a key concern for anyone interested in personal finance, investing, and building online income.

Understanding the Core Concept: What Exactly is a Spousal IRA?

At its heart, a Spousal IRA is not a separate type of IRA account with unique rules. Instead, it’s a provision within the established IRA framework that allows a working spouse to contribute to an IRA on behalf of their non-working or lower-earning spouse. This is a fundamental distinction. The account itself is still either a Traditional IRA or a Roth IRA, inheriting all the tax benefits and investment options associated with those designations. The “spousal” aspect refers solely to the source of the contribution and the eligibility of the recipient.

Imagine a scenario where one partner in a marriage is the primary breadwinner, while the other spouse focuses on managing the household, raising children, or pursuing education without a significant income. Without the Spousal IRA provision, the non-working spouse would have no direct avenue to contribute to their own tax-advantaged retirement account. This could lead to a significant disparity in retirement savings between the partners, potentially impacting their quality of life in later years. The Spousal IRA effectively bridges this gap, ensuring that both individuals have the opportunity to save for retirement, regardless of their individual earned income.

The IRS regulations are clear on this. For a contribution to be considered a spousal contribution, the contributing spouse must have earned income during the year that is at least equal to the total of their own IRA contributions plus the spousal contribution. For example, if a working spouse contributes the maximum to their own Traditional IRA ($6,500 in 2023, for those under 50) and also wants to contribute the maximum to a Spousal IRA for their partner ($6,500 in 2023), they must have earned income of at least $13,000 for that tax year. This ensures that the contribution is genuinely funded by earned income and not from other sources like investment gains or gifts.

Eligibility Requirements: Who Qualifies for a Spousal IRA?

The eligibility for a Spousal IRA is straightforward, centered around marital status and earned income. To be eligible to contribute to a Spousal IRA for your spouse, you must be legally married at the end of the tax year for which you are making the contribution. This means that if you get married during the year, you can establish and contribute to a Spousal IRA for that tax year, provided you meet the other criteria.

The crucial requirement is that the contributing spouse must have sufficient earned income. As mentioned, this earned income must be equal to or greater than the sum of the contributions made to both the contributing spouse’s IRA and the Spousal IRA. “Earned income” generally includes wages, salaries, tips, commissions, and net earnings from self-employment. It does not typically include income from investments, pensions, annuities, or alimony.

There are no strict income limitations for contributing to a Traditional IRA, meaning that even high-income earners can contribute to a Spousal Traditional IRA. However, the deductibility of those contributions may be phased out if the contributing spouse is covered by a retirement plan at work and their modified adjusted gross income (MAGI) exceeds certain thresholds. For Roth IRAs, there are MAGI limits for contributions, which apply to both the contributing spouse’s own Roth IRA and any Spousal Roth IRA established on behalf of their partner. If the couple’s MAGI exceeds these limits, they may not be able to contribute directly to a Roth IRA or a Spousal Roth IRA. However, backdoor Roth IRA strategies can still be an option in such cases.

Crucially, the spouse for whom the IRA is being established does not need to have any earned income of their own. This is the primary purpose of the Spousal IRA – to allow individuals who are not actively earning an income to participate in retirement savings. This inclusivity makes it a vital tool for couples where one partner may be a stay-at-home parent, a student, or otherwise not gainfully employed.

Maximizing Your Retirement Savings: Contribution Limits and Tax Benefits

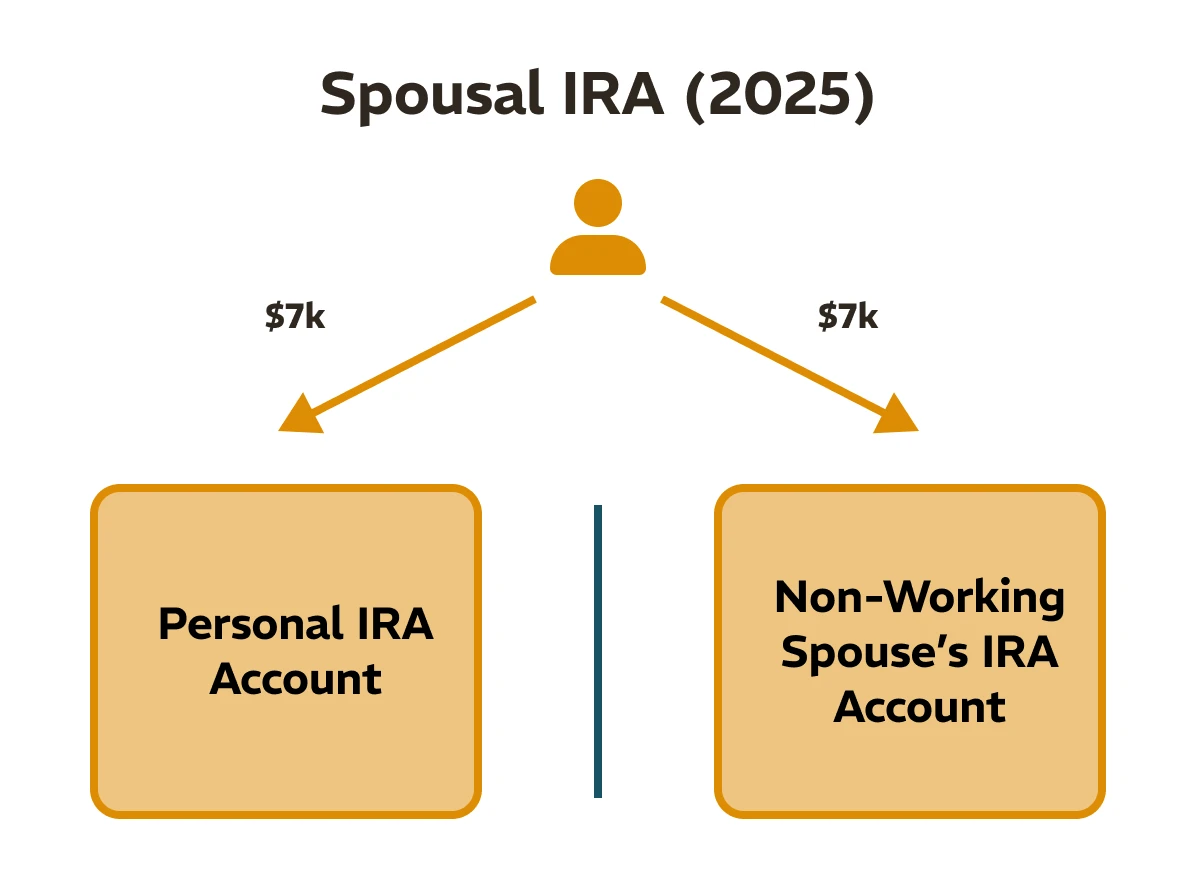

The beauty of a Spousal IRA lies in its ability to allow couples to contribute twice the standard IRA limit to their retirement accounts, effectively doubling their tax-advantaged savings potential for a single tax year. The contribution limits are set annually by the IRS and apply to the combined total of contributions made to all of a person’s IRAs (Traditional and Roth).

For example, in 2023, the maximum contribution to an IRA for individuals under age 50 was $6,500. This means a married couple, where one spouse has earned income, could contribute up to $13,000 to IRAs for the year: $6,500 to the working spouse’s IRA and $6,500 to the Spousal IRA for the non-working spouse. For individuals aged 50 and over, there’s an additional catch-up contribution allowed, which also applies to Spousal IRAs. In 2023, this catch-up contribution was an extra $1,000, bringing the total for those 50 and over to $7,500 per person, and therefore up to $15,000 for a couple.

The tax benefits are a major draw. When contributing to a Spousal Traditional IRA, the contributions are typically tax-deductible in the year they are made, reducing the couple’s taxable income. This can provide immediate tax relief and, for many, make retirement saving more affordable. The earnings within the account grow tax-deferred, meaning you don’t pay taxes on them year after year. You only pay ordinary income tax on withdrawals made during retirement.

Alternatively, a couple can opt for a Spousal Roth IRA. With a Roth IRA, contributions are made with after-tax dollars, meaning there’s no immediate tax deduction. However, the significant advantage is that qualified withdrawals in retirement are completely tax-free. This can be particularly beneficial for couples who anticipate being in a higher tax bracket in retirement or who simply prefer the certainty of tax-free income later in life.

Traditional vs. Roth Spousal IRA: Making the Right Choice

The decision between establishing a Spousal Traditional IRA or a Spousal Roth IRA hinges on a couple’s current and projected future financial circumstances, particularly their tax situation.

Spousal Traditional IRA: This is often the preferred choice for individuals who believe they are in a higher tax bracket now than they will be in retirement. The upfront tax deduction can significantly reduce their current tax liability, freeing up more immediate funds. The tax-deferred growth then allows their retirement savings to compound without annual taxation. However, it’s crucial to remember that all withdrawals in retirement will be subject to ordinary income tax rates.

Spousal Roth IRA: This option is generally more attractive for those who believe they will be in the same or a higher tax bracket in retirement than they are currently. By paying taxes on the contributions now, they lock in tax-free withdrawals later. This provides a degree of certainty and protection against future tax rate increases. It’s also a compelling option for younger couples who have many years for their investments to grow tax-free.

Several factors can influence this decision:

- Current Income and Tax Bracket: If your current income is high, the tax deduction from a Traditional IRA can be very valuable.

- Expected Future Income and Tax Bracket: If you anticipate your income to be higher in retirement, a Roth IRA’s tax-free withdrawals are more appealing.

- Age: Younger individuals have more time for tax-free compounding with a Roth IRA.

- Flexibility: Roth IRAs offer more flexibility with withdrawals of contributions (though not earnings) before retirement age without penalty or taxes, though this should generally be avoided for retirement planning.

- Estate Planning: Inherited Roth IRAs can offer tax advantages to beneficiaries.

It’s also worth noting that a couple can choose different IRA types for each spouse. For instance, one spouse could have a Traditional IRA while the other has a Roth IRA, depending on their individual circumstances and the overall family financial strategy. Consulting with a financial advisor can help a couple navigate these choices and align their Spousal IRA decisions with their broader financial goals, including any online income streams or business finance considerations.

Beyond the Basics: Advanced Considerations and Integration

While the core mechanics of a Spousal IRA are relatively straightforward, there are several advanced considerations that married couples should be aware of to truly optimize their retirement planning. Understanding these nuances can help prevent common pitfalls and maximize the long-term benefits of this powerful financial tool.

Rollovers and Transfers: Maintaining Continuity

Life can bring unexpected changes, and sometimes it’s necessary to move retirement funds from one account to another. The good news is that funds held within a Spousal IRA (whether Traditional or Roth) can generally be rolled over or transferred without penalty, similar to any other IRA.

- Rollover: This involves withdrawing funds from an existing IRA and depositing them into a new IRA within 60 days. This can be done when opening a new Spousal IRA, switching financial institutions, or consolidating accounts. It’s crucial to adhere to the 60-day rule to avoid taxes and penalties. Alternatively, direct trustee-to-trustee transfers eliminate the risk of missing the deadline.

- Roth Conversions: Funds from a Spousal Traditional IRA can be converted into a Spousal Roth IRA. This involves paying taxes on the converted amount in the year of conversion, but it allows those funds to grow and be withdrawn tax-free in retirement. This strategy is often employed when individuals anticipate higher tax rates in the future.

It’s also important to understand that if the contributing spouse passes away, the surviving spouse can typically inherit the Spousal IRA. The rules for inherited IRAs can be complex, depending on whether the beneficiary is a spouse or a non-spouse, and whether the deceased spouse had begun taking distributions. Spouses generally have more favorable options, such as treating the inherited IRA as their own.

Spousal IRA and Other Retirement Plans: A Holistic View

For couples where one or both spouses have access to employer-sponsored retirement plans like a 401(k) or 403(b), the Spousal IRA complements these plans rather than replacing them. Contributions to a Spousal IRA are independent of contributions made to employer-sponsored plans.

The key consideration here relates to the deductibility of Traditional IRA contributions. If the contributing spouse (or their spouse, if they are married filing jointly) is covered by a retirement plan at work, the deductibility of their Traditional IRA contributions (including spousal contributions) may be limited based on their modified adjusted gross income (MAGI). However, if neither spouse is covered by a retirement plan at work, then the contributions to a Spousal Traditional IRA are fully deductible, regardless of income.

For Roth IRAs, the income limitations for contributions apply regardless of whether either spouse is covered by a workplace retirement plan. If the couple’s MAGI exceeds the Roth IRA limits, they will not be able to contribute directly to a Spousal Roth IRA.

Integrating Spousal IRAs into a broader retirement strategy requires a holistic approach. This involves:

- Maximizing Employer Match: Always prioritize contributing enough to a 401(k) or similar plan to receive any employer match, as this is essentially free money.

- Utilizing Spousal IRAs: After maximizing employer matches, consider contributions to Spousal IRAs to further boost tax-advantaged savings.

- Considering Other Investment Vehicles: Depending on overall financial goals, income levels, and risk tolerance, other investment accounts like taxable brokerage accounts or HSAs may also play a role.

Effective financial planning, whether it involves managing personal finance, building online income, or understanding business finance, is about making informed decisions that align with long-term objectives. The Spousal IRA is a powerful tool that, when understood and utilized correctly, can significantly enhance a couple’s journey towards a secure and prosperous retirement. It underscores the principle that financial well-being is often a team effort, and the Spousal IRA provides a concrete mechanism for couples to work together towards their shared future.