A pledge loan, also known as a collateral loan or securities-based loan, is a type of financing where an individual or business borrows money by using existing assets as collateral. Unlike traditional loans that often require proof of income and a strong credit history, a pledge loan leverages the value of assets already owned. This can include a wide range of liquid and semi-liquid assets, making it a flexible and often faster way to access capital. Understanding the mechanics, advantages, and potential drawbacks of pledge loans is crucial for anyone considering this financial instrument.

The Mechanics of a Pledge Loan

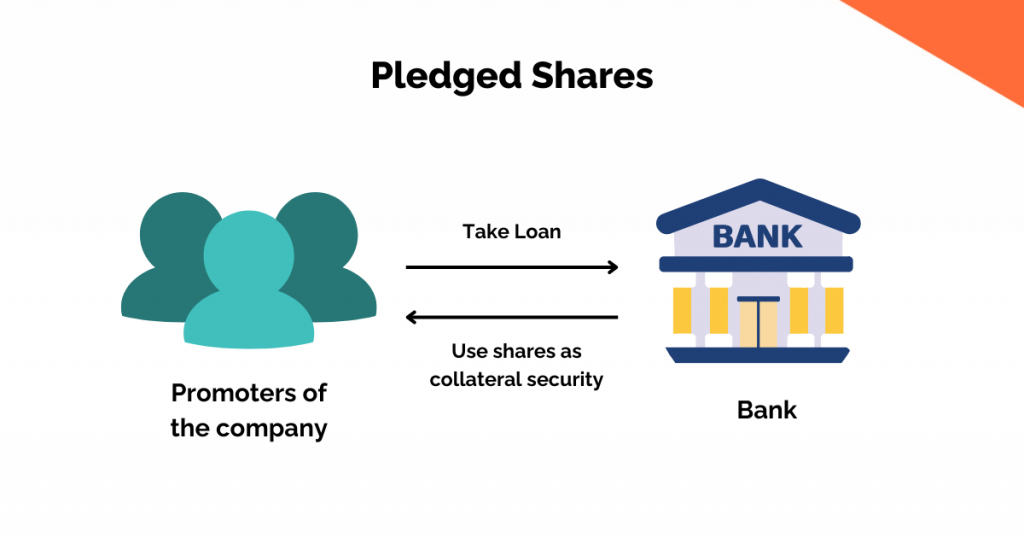

At its core, a pledge loan involves a borrower offering specific assets as security to a lender. The lender then provides a loan, the amount of which is typically a percentage of the collateral’s value. This percentage is known as the loan-to-value (LTV) ratio. If the borrower defaults on the loan, the lender has the right to seize and sell the pledged assets to recoup their losses. This fundamental principle of collateralization is what differentiates pledge loans from unsecured loans.

Types of Collateral Accepted

The versatility of pledge loans stems from the variety of assets that can be pledged. Lenders are generally looking for assets that are easily valued and can be readily liquidated if necessary. Common examples include:

Securities and Investments

This is perhaps the most frequent form of collateral for pledge loans. It encompasses a broad spectrum of investment vehicles:

- Stocks and Bonds: Publicly traded stocks and high-quality bonds (like government or corporate bonds) are highly liquid and their market value is readily ascertainable. Lenders will typically advance a percentage of the current market value.

- Mutual Funds and Exchange-Traded Funds (ETFs): Similar to stocks, the value of these diversified investment portfolios is transparent and fluctuates with the market.

- Certificates of Deposit (CDs): While less volatile than market-based securities, CDs can also serve as collateral, often with a higher LTV ratio due to their stability.

- Annuities: Certain types of annuities can be pledged, though their valuation and liquidity can be more complex.

Other Pledgable Assets

While securities are prevalent, other assets can also be used:

- Cash and Savings Accounts: Pledging cash held in savings accounts or money market accounts is one of the most straightforward forms of collateral. This often allows for the highest LTV ratios.

- Life Insurance Policies: Whole life insurance policies with a cash surrender value can be pledged. The loan amount is typically a percentage of this cash value.

- Real Estate: While less common for standard pledge loans (which usually focus on liquid assets), in some contexts, real estate can be used as collateral. However, this often falls under different loan categories like home equity loans or mortgages, which have more involved processes. For the purpose of this discussion, we will focus on more liquid forms of collateral.

- Business Assets: In a business context, receivables, inventory, or equipment can sometimes be pledged, though these often fall under specific business lending products.

The Loan-to-Value (LTV) Ratio

The LTV ratio is a critical component of any pledge loan. It dictates the maximum amount a borrower can receive against their pledged collateral. For instance, if an investor pledges $100,000 worth of stocks and the lender offers an LTV of 70%, the borrower can receive a loan of up to $70,000.

The LTV ratio varies significantly depending on the type of collateral and the lender’s risk assessment. More volatile assets, like individual stocks, will generally have lower LTV ratios compared to stable assets like cash or CDs. Market fluctuations can also impact the LTV, and lenders may issue margin calls if the value of the collateral falls below a certain threshold, requiring the borrower to either add more collateral or repay part of the loan.

Advantages of Pledge Loans

Pledge loans offer several compelling advantages, making them an attractive financing option for individuals and businesses with existing assets. These benefits primarily revolve around speed, flexibility, and potentially lower interest rates compared to other loan types.

Accessibility and Speed of Funding

One of the most significant advantages of a pledge loan is its accessibility, especially for individuals who may not qualify for traditional loans due to limited credit history or income fluctuations. Since the loan is secured by tangible assets, the lender’s risk is substantially reduced. This often translates into:

- Simplified Approval Process: The underwriting process for pledge loans is typically less rigorous than for unsecured loans. Lenders primarily focus on the value and type of collateral rather than extensive credit checks and income verification.

- Faster Funding Times: Once the collateral is pledged and the loan agreement is finalized, funds can often be disbursed much more quickly than with traditional loans. This speed is invaluable when immediate capital is needed for opportunities or emergencies.

Maintaining Ownership of Assets

A key benefit is that the borrower typically retains ownership and beneficial interest in the pledged assets. For example, if stocks are pledged, the borrower continues to receive dividends and can benefit from any appreciation in value. This is a crucial distinction from selling assets outright to raise cash. The borrower can continue to manage their investments while using them as collateral.

Potential for Lower Interest Rates

Because pledge loans are secured by collateral, they are considered less risky for lenders. This reduced risk often allows lenders to offer lower interest rates compared to unsecured personal loans or credit cards. While interest rates are not as low as, for instance, a mortgage (which is secured by real estate), they can be more competitive than many other forms of consumer credit.

Flexibility in Use of Funds

Pledge loans are generally versatile in how the borrowed funds can be used. Borrowers can access capital for a wide range of purposes, including:

- Investment Opportunities: Seizing time-sensitive investment opportunities that may offer a higher return than the interest rate on the pledge loan.

- Business Expansion: Providing working capital for a business, funding new projects, or covering operational expenses.

- Personal Expenses: Financing major purchases, covering unexpected medical bills, or consolidating debt.

- Emergency Funding: Having access to funds for unforeseen circumstances without needing to liquidate long-term investments prematurely.

Potential Risks and Considerations

While pledge loans offer numerous advantages, it is essential to be aware of the potential risks and carefully consider them before proceeding. The primary risk lies in the possibility of losing the pledged collateral if the loan cannot be repaid.

The Risk of Collateral Loss

The most significant risk associated with pledge loans is default. If a borrower is unable to make loan payments, or if the value of the pledged collateral drops significantly, the lender has the right to seize and sell the collateral to recover the outstanding loan amount. This can result in a substantial loss of assets, especially if the collateral was a significant portion of the borrower’s wealth.

Margin Calls and Collateral Value Fluctuations

For loans secured by market-based securities, fluctuations in asset values are a constant concern. Lenders often have covenants that require the collateral value to remain above a certain percentage of the loan amount. If market downturns cause the collateral value to fall below this threshold, the lender will issue a “margin call.” This requires the borrower to either:

- Deposit additional collateral: To bring the loan-to-value ratio back within acceptable limits.

- Repay a portion of the loan: To reduce the outstanding balance.

- Allow the lender to sell collateral: If the borrower cannot meet the margin call, the lender may sell some or all of the pledged assets to cover the shortfall.

Impact on Investment Strategy

Borrowers must consider how pledging their assets might impact their overall investment strategy. For instance, if a significant portion of a portfolio is pledged, it could limit the borrower’s ability to rebalance their portfolio or take advantage of new investment opportunities. It also means that any losses in the pledged assets directly affect their ability to repay the loan.

Interest Rates and Fees

While pledge loans can offer competitive interest rates, it’s crucial to understand the total cost of borrowing. This includes not only the interest rate but also any associated fees, such as origination fees, annual maintenance fees, or early repayment penalties. Borrowers should compare offers from multiple lenders to ensure they are getting the best possible terms.

Understanding Loan Covenants

Pledge loan agreements will contain specific covenants that the borrower must adhere to. These can include maintaining a certain debt-to-collateral ratio, providing regular updates on collateral value, and adhering to any restrictions on further pledging of assets. Failure to comply with these covenants can lead to default, even if loan payments are current.

Who Benefits from a Pledge Loan?

Pledge loans are not a one-size-fits-all solution. They are best suited for individuals and businesses who meet specific criteria and have particular financial needs.

Investors with Significant Liquid Portfolios

The most natural fit for pledge loans are investors who hold substantial amounts of stocks, bonds, mutual funds, or other readily marketable securities. These individuals often seek to:

- Access liquidity without selling investments: They may believe in the long-term growth potential of their portfolio and do not want to trigger capital gains taxes or miss out on future appreciation by selling.

- Leverage their assets for opportunities: They might want to invest in a real estate deal, start a new venture, or fund a significant personal purchase without disrupting their existing investment strategy.

- Manage cash flow: Investors might use pledge loans to bridge gaps in cash flow, cover large expenses, or manage wealth without liquidating assets.

Individuals Seeking Fast Access to Capital

For those who require funds quickly and have assets that can be pledged, a pledge loan offers a faster alternative to traditional lending. This can be beneficial for:

- Responding to time-sensitive opportunities: Whether it’s an investment that requires immediate capital or a business deal that needs swift execution.

- Handling emergencies: While not ideal for all emergencies, a pledge loan can be a viable option if immediate funds are needed and other avenues are too slow.

Businesses Needing Working Capital

Small and medium-sized businesses that possess valuable liquid assets or securities can utilize pledge loans to bolster their working capital. This can help them:

- Manage seasonal cash flow fluctuations: Ensuring they have enough capital during slower periods.

- Fund inventory purchases: Taking advantage of bulk discounts or securing necessary supplies.

- Cover unexpected operational costs: Maintaining smooth business operations without disrupting core activities.

In conclusion, a pledge loan is a powerful financial tool that allows individuals and businesses to borrow against the value of their existing assets. By understanding the mechanics, benefits, and risks, borrowers can determine if this type of financing aligns with their financial goals and risk tolerance, ultimately making informed decisions about accessing capital.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.