Credit Karma is a popular platform that provides users with free access to their credit scores and reports, along with personalized recommendations for financial products. While the service itself is straightforward, understanding what constitutes a “good” credit score within the Credit Karma ecosystem can be a source of confusion. This article will delve into the nuances of credit scoring, how Credit Karma presents this information, and what benchmarks you should aim for to unlock the best financial opportunities. We will focus on the “Money” niche, exploring how credit scores directly impact your financial well-being.

Understanding Credit Scores and Their Importance

At its core, a credit score is a three-digit number that lenders use to assess your creditworthiness. It’s a snapshot of your financial behavior, reflecting how likely you are to repay borrowed money. This score plays a pivotal role in virtually every significant financial transaction you’ll encounter throughout your life.

The Mechanics of Credit Scoring

Credit scoring models, such as FICO and VantageScore, are the algorithms that calculate these crucial numbers. While Credit Karma primarily uses VantageScore, it’s important to understand the general factors that influence both. These factors are:

- Payment History: This is the most significant factor, accounting for about 35% of your FICO score. It includes whether you pay your bills on time, late payments, bankruptcies, and collections. Consistent on-time payments are the bedrock of a good credit score.

- Credit Utilization Ratio: This refers to the amount of credit you’re using compared to your total available credit. Aiming to keep this ratio below 30% is generally recommended, with lower being better. For example, if you have a credit card with a $10,000 limit, keeping your balance below $3,000 is a good strategy. High utilization can signal financial distress to lenders.

- Length of Credit History: The longer you’ve been managing credit responsibly, the more data lenders have to assess your risk. This factor contributes about 15% to your FICO score. This means avoiding closing old, unused credit accounts, as it can shorten your average credit history length.

- Credit Mix: Having a variety of credit types, such as credit cards, installment loans (like mortgages or auto loans), can also positively influence your score. Lenders like to see that you can manage different forms of credit responsibly, contributing around 10% to your FICO score.

- New Credit: Opening multiple new credit accounts in a short period can negatively impact your score, as it might be interpreted as a sign of financial instability. This factor accounts for approximately 10% of your FICO score.

Why Your Credit Score Matters: Beyond Just Loans

Your credit score isn’t just about qualifying for loans. It has far-reaching implications across various aspects of your financial life:

- Interest Rates: A higher credit score typically means you’ll qualify for lower interest rates on loans, mortgages, auto loans, and credit cards. Over the life of a loan, this can translate into thousands of dollars saved.

- Loan Approval: A good credit score is often a prerequisite for approving loan applications. If your score is too low, you might be denied credit altogether.

- Renting Apartments: Many landlords check credit scores as part of their tenant screening process. A poor score can make it harder to secure a desirable rental property.

- Insurance Premiums: In some states, insurance companies use credit-based insurance scores to determine premiums for auto and homeowners insurance. A better score can lead to lower insurance costs.

- Utility Deposits: Some utility companies may require a security deposit if you have a low credit score.

- Employment: Certain employers, particularly in sensitive industries, may review credit reports as part of their background checks.

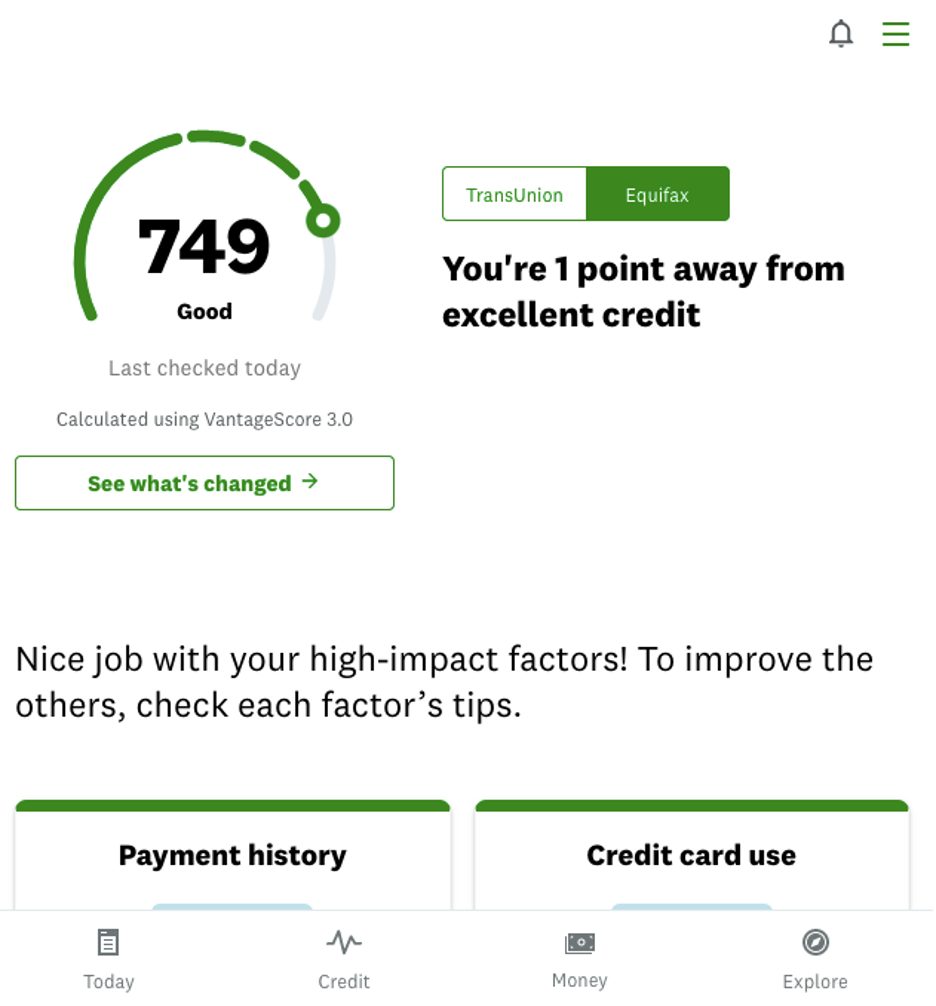

Navigating Credit Karma’s Score Representation

Credit Karma offers a user-friendly interface to monitor your credit health. It’s crucial to understand how they present credit scores and what their categories signify.

Understanding VantageScore

As mentioned, Credit Karma primarily utilizes VantageScore. It’s essential to know that VantageScore and FICO are distinct scoring models, though they share many underlying principles. VantageScore ranges from 300 to 850, similar to FICO. Credit Karma often categorizes scores into general ranges to provide a quick understanding of your credit standing.

Credit Karma’s Score Tiers and What They Mean

While Credit Karma doesn’t explicitly define “good” with a single number, they often present scores in descriptive tiers. These tiers are generally interpreted as follows:

- Poor (300-579): At this level, you are likely to face significant challenges obtaining credit. Lenders may see you as a high risk, and you’ll likely encounter higher interest rates or outright denials for loans and credit cards. You may also need to provide larger security deposits for services.

- Fair (580-669): This range indicates that you have some credit challenges. While you might be approved for some credit products, you’ll likely face higher interest rates and less favorable terms. Building a stronger credit history is a priority in this tier.

- Good (670-739): This is a solid credit range. You are likely to be approved for most credit products and can expect reasonably competitive interest rates. This is a target many individuals strive for.

- Very Good (740-799): With a “Very Good” score, you’re in a strong position. You’ll qualify for a wide array of credit products with favorable terms and competitive interest rates. Lenders see you as a reliable borrower.

- Excellent (800-850): This is the top tier. An “Excellent” credit score signifies exceptional creditworthiness. You’ll likely have access to the best loan offers, the lowest interest rates, and may even receive special perks and rewards from lenders.

The Nuance: Credit Karma’s Personalized Recommendations

Beyond just displaying your score, Credit Karma’s value lies in its personalized recommendations. The platform analyzes your credit profile and suggests specific credit cards, loans, or other financial products that you might be approved for. The “goodness” of a number for Credit Karma is not just about hitting a general benchmark; it’s about how that number unlocks specific opportunities presented by the platform. For instance, a score that might be considered “Good” could qualify you for certain credit cards, while a “Very Good” score might open doors to even better rewards or lower APRs.

What Constitutes a “Good” Number for Credit Karma?

Defining a “good number” for Credit Karma is multifaceted. It’s not just about hitting a specific threshold; it’s about achieving a score that aligns with your financial goals and maximizes your opportunities.

The “Good Enough” Score for General Purposes

For most everyday financial needs, such as qualifying for a decent credit card with a reasonable rewards program or getting approved for an auto loan at a competitive rate, aiming for a score in the “Good” range (670-739) is often sufficient. This range demonstrates responsible credit management and provides a solid foundation for most financial transactions. If your goal is simply to avoid the pitfalls of a poor credit score and access mainstream financial products, then reaching this tier is a significant achievement.

The Sweet Spot for Optimal Financial Benefits

To truly leverage your credit score for maximum financial advantage, you should aim for the “Very Good” (740-799) to “Excellent” (800-850) ranges. In these tiers, you’re not just getting approved; you’re getting the best terms. This means:

- Lowest Interest Rates: This is where the most significant savings occur. On a mortgage, for example, a slight improvement in your score can save you tens of thousands of dollars over 30 years.

- Higher Credit Limits: With excellent credit, lenders are more comfortable extending larger lines of credit, which can improve your credit utilization ratio and provide more financial flexibility.

- Access to Premium Rewards Cards: The most coveted travel and cashback rewards credit cards often require excellent credit.

- Better Negotiation Power: A strong credit score gives you more leverage when negotiating terms for loans and other financial products.

The “Good” Number is Relative to Your Goals

It’s crucial to remember that the “goodness” of a credit number is relative to your personal financial aspirations.

- For a first-time credit user: Simply establishing a positive credit history and reaching the “Fair” or “Good” range is a huge win.

- For someone looking to buy a home: A score in the “Very Good” to “Excellent” range will be paramount to securing favorable mortgage terms and avoiding exorbitant interest payments.

- For someone seeking to improve their credit card rewards: Aiming for “Excellent” credit will unlock the most lucrative travel and cashback opportunities.

Credit Karma’s personalized recommendations can guide you on what score is “good enough” to qualify for specific offers they present. If you see a credit card with an offer you like, Credit Karma will often indicate the score range typically required for approval.

Strategies to Improve Your Credit Score on Credit Karma

Improving your credit score is an ongoing process, but Credit Karma can be a valuable tool in this journey. By understanding your current standing and identifying areas for improvement, you can take actionable steps.

Utilizing Credit Karma’s Tools for Improvement

Credit Karma provides several features that can help you boost your score:

- Credit Report Monitoring: Regularly review your credit reports for errors. Inaccurate information can significantly harm your score. Credit Karma allows you to access these reports and identify any discrepancies.

- Score Factors: Credit Karma breaks down the factors that are influencing your score, both positively and negatively. This helps you pinpoint specific areas to focus on. For example, if your credit utilization is high, the platform will flag this, prompting you to take action.

- Personalized Recommendations: As discussed, Credit Karma suggests products that align with your credit profile. While this is a business model, it can also be a stepping stone. If you’re in the “Fair” range, they might recommend a secured credit card that can help you build positive credit history.

- Credit Score Simulators: Some platforms, and Credit Karma may offer similar features, allow you to simulate how certain actions (like paying down a credit card balance) might impact your score.

Actionable Steps for Score Enhancement

Based on the insights gained from Credit Karma, here are concrete steps you can take:

- Pay Bills on Time, Every Time: This is non-negotiable. Set up automatic payments or reminders to ensure you never miss a due date.

- Lower Your Credit Utilization Ratio: If your balances are high, focus on paying them down. Aim to keep your utilization below 30%, ideally below 10% for the best impact.

- Avoid Opening Too Many New Accounts: Be strategic when applying for new credit. Only apply for credit you genuinely need.

- Keep Old Accounts Open: Unless there’s a compelling reason (like a high annual fee on an unused card), keep older, unused credit accounts open. This helps your average age of credit.

- Dispute Errors on Your Credit Report: If you find any inaccuracies, take the time to dispute them with the credit bureaus.

- Consider a Mix of Credit (When Appropriate): As your credit history grows, demonstrating responsible management of different credit types can be beneficial, but don’t open accounts solely for this purpose.

- Become an Authorized User (with Caution): If a trusted friend or family member with excellent credit adds you as an authorized user to their card, their positive payment history can sometimes benefit your score. However, ensure they are responsible with their credit.

By diligently using the resources Credit Karma provides and implementing these strategies, you can systematically improve your credit score, moving closer to the “good number” that unlocks your financial potential.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.