In the dynamic and often aggressive world of mergers and acquisitions (M&A), the “bear hug” stands out as a particularly potent and strategically charged maneuver. Far from an embrace of warmth, a bear hug in business is a high-stakes, unsolicited takeover bid designed to exert significant pressure on a target company’s board and shareholders. It’s a financial tactic deployed by an acquiring firm when it seeks to secure control of another company, often one that has previously resisted or shown no inclination towards being acquired. Understanding this strategy is crucial for investors, corporate executives, and financial professionals, as it represents a significant chapter in the complex narrative of corporate finance.

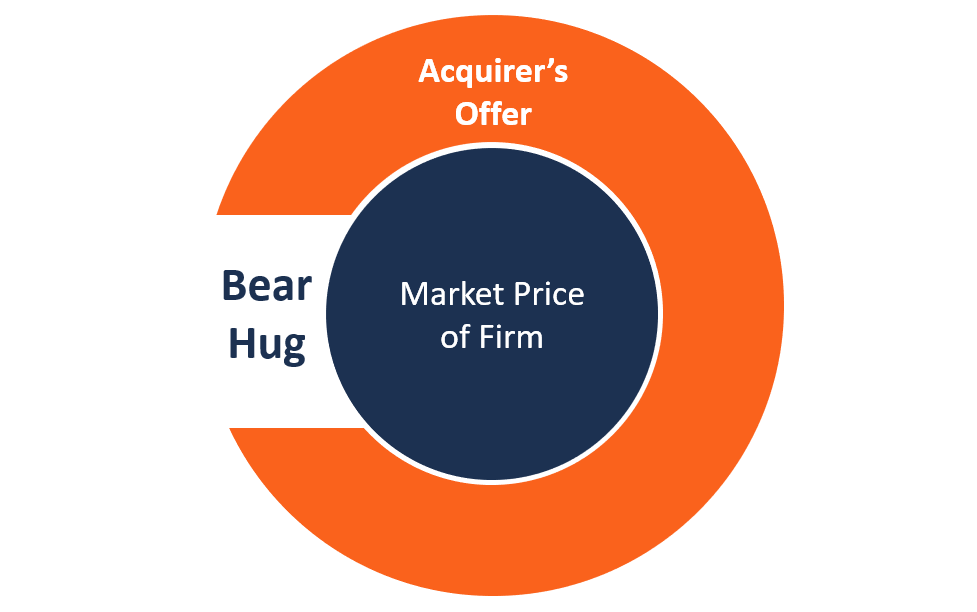

At its core, a bear hug is a definitive, premium offer made directly to the board of directors of a target company, often with the intention of making the offer public if the board resists. The key characteristics that define a bear hug are its unsolicited nature, the attractive premium offered over the target’s current market valuation, and the implicit (or explicit) pressure on the target board to accept lest they face the wrath of their shareholders for rejecting a financially superior deal. This strategy bypasses the usual, often lengthy, negotiation processes, aiming instead for a swift and decisive resolution. For the acquiring company, it’s a bold play to secure a strategic asset, while for the target, it represents a moment of intense financial and strategic reckoning, demanding a careful balance of fiduciary duty and corporate survival.

The Anatomy of a Bear Hug Offer

The effectiveness of a bear hug stems from its carefully constructed financial and tactical components. It’s not merely an offer; it’s a strategic package designed to be difficult to refuse.

Unsolicited and Definitive Terms

Unlike a friendly acquisition where initial overtures might lead to a period of due diligence and negotiation, a bear hug arrives uninvited and fully formed. The acquiring company typically conducts its preliminary due diligence discretely, often based on publicly available information, to craft an offer that is as definitive as possible from the outset. This means the proposal includes specific terms regarding price, payment structure (cash, stock, or a combination), financing commitments, and often a short timeframe for consideration. The lack of prior engagement signals the acquirer’s determination and bypasses the target’s management, who might otherwise stall or reject initial contact. The definitive nature of the terms leaves little room for ambiguity, forcing the target’s board to confront a concrete proposition rather than a speculative interest.

High Premium and Urgency

The most compelling financial aspect of a bear hug is the substantial premium it typically offers over the target company’s current trading price. This premium is crucial; it’s the bait designed to make the deal irresistible to shareholders. A premium of 20%, 30%, or even higher can be offered, making the target’s stock price jump significantly upon announcement. The underlying calculation for the acquirer is that the strategic value, synergies, or market access gained will more than offset the high purchase price. Alongside this attractive valuation, bear hug offers usually come with a strict deadline. This urgency is a pressure tactic, designed to prevent the target’s board from exploring alternative options, implementing defensive strategies, or engaging in protracted negotiations. It forces a quick decision, limiting the board’s time to strategize and potentially find a “white knight” or mount an effective defense.

Public Disclosure Strategy

A key component of many bear hug strategies is the threat, or actual execution, of publicizing the offer. If the target’s board indicates resistance or fails to respond within the given timeframe, the acquiring company may choose to publicly disclose its offer. This move is a direct appeal to the target’s shareholders, bypassing the board entirely. By making the offer public, the acquirer places the target’s board in a precarious position. Shareholders, seeing a significant and immediate financial gain, will naturally pressure their board to accept the offer. Failing to do so could lead to accusations of neglecting fiduciary duties and potentially spark a proxy fight, where the acquirer might attempt to replace the board with directors more amenable to the acquisition. This public pressure can be an extremely effective way to force a reluctant board’s hand.

Why Companies Employ the Bear Hug Strategy

The decision to launch a bear hug is not taken lightly; it’s a move reserved for specific strategic and financial objectives, often when conventional M&A paths appear blocked or too slow.

Overcoming Management Resistance

One of the primary reasons acquirers resort to a bear hug is when they anticipate or have already faced resistance from the target company’s management or board. The target might prefer to remain independent, believe their company is undervalued, or simply have a different strategic vision. In such scenarios, a bear hug offers a way to circumvent this resistance. By presenting an undeniably attractive financial offer directly to the shareholders (via the board, and potentially the public), the acquirer creates a powerful incentive that overrides management’s objections. It’s a direct challenge to the target’s leadership, essentially telling them, “Your shareholders will want this deal.”

Expediting the Acquisition Process

M&A negotiations can be notoriously complex, time-consuming, and expensive. They often involve lengthy due diligence, multiple rounds of proposals and counter-proposals, and intricate legal frameworks. A bear hug strategy aims to condense this process significantly. By presenting a high-premium, definitive offer, the acquirer attempts to force a quick decision. This can be particularly advantageous in fast-moving industries where market conditions can change rapidly, or when securing a specific strategic asset quickly is paramount to maintaining a competitive edge. The urgency built into the offer is designed to limit the time the target has to explore alternatives or mount a robust defense.

Maximizing Shareholder Value (Acquirer’s Perspective)

From the acquirer’s viewpoint, a bear hug is often about seizing a strategic opportunity that promises to enhance its own shareholder value. This could involve acquiring a competitor to consolidate market share, gaining access to new technology, expanding into new geographic markets, or achieving significant cost synergies. By paying a premium upfront, the acquirer is making a calculated bet that the long-term financial benefits derived from the acquisition will far outweigh the initial high cost. The direct approach of a bear hug ensures that the target company, once acquired, can be integrated quickly into the acquirer’s operations, allowing them to realize these anticipated synergies sooner.

Strategic Fit and Market Expansion

Beyond pure financial metrics, bear hugs are often driven by a strong belief in the strategic fit between the two companies. The target company might possess unique intellectual property, a strong customer base, a critical supply chain component, or an established presence in a desired market. When such a strategic asset is not available through conventional means, a bear hug can be the most direct route. It’s about buying a competitive advantage or solving a strategic challenge that simply cannot wait. The financial premium reflects the high value placed on this strategic alignment and the perceived difficulty of achieving it through other means.

The Target Company’s Dilemma: Responding to a Bear Hug

For the target company’s board of directors, receiving a bear hug offer presents a profound challenge, demanding a meticulous balancing act between their fiduciary duties, corporate independence, and shareholder interests.

Evaluating the Offer Financially

The immediate and most critical task for the target’s board is to rigorously evaluate the financial attractiveness of the offer. This involves engaging independent financial advisors to conduct a thorough valuation of the company. Is the premium truly sufficient? Does it reflect the company’s intrinsic value, future growth prospects, and potential synergies that the acquirer might realize? The board must consider not just the current market price, but also what the company could be worth in the absence of an acquisition, or under alternative scenarios. They must assess the payment structure (cash vs. stock), the certainty of financing, and any conditions attached to the offer. Their fiduciary duty dictates that they act in the best financial interest of their shareholders, and rejecting a truly superior offer could expose them to legal challenges and shareholder dissent.

Fiduciary Duty of the Board

Central to the board’s responsibility is its fiduciary duty to its shareholders. This duty typically requires directors to act in good faith and in the best interests of the corporation and its owners. When faced with a bear hug, this often translates to a duty to maximize shareholder value. If an independent financial assessment concludes that the bear hug offer represents a fair or even superior value compared to the company’s standalone prospects, the board is under immense pressure to accept or at least seriously consider it. Rejecting such an offer without a compelling financial or strategic justification can lead to accusations of self-interest (e.g., protecting their own positions) or neglecting their core duties, potentially leading to a shareholder revolt or even litigation.

Defensive Maneuvers and Counter-Strategies

Despite the pressure, a target company is not entirely defenseless. Boards can employ various financial and strategic maneuvers to counter a bear hug:

- Poison Pill (Shareholder Rights Plan): This common defense makes the target company less attractive to the acquirer by diluting their ownership stake if they acquire above a certain threshold without board approval. It forces the acquirer to negotiate with the board.

- White Knight: The target board might seek out a “white knight” – another company willing to make a friendly, often higher, counter-offer. This provides an alternative for shareholders and can save the company from a hostile takeover.

- “Just Say No” Defense: In rare circumstances, if the board believes the offer fundamentally undervalues the company or poses severe strategic risks, they may choose to simply reject it, arguing that the company’s long-term value creation potential far exceeds the bear hug offer. This is often accompanied by a detailed strategic plan outlining how they intend to achieve superior value independently.

- Recapitalization/Share Buyback: The company might undertake a significant share buyback or issue a large dividend, often financed by debt, to increase shareholder value and make the company less financially attractive for an acquisition.

Shareholder Pressure and Activist Investors

One of the most powerful forces unleashed by a bear hug is direct shareholder pressure. Once the offer is made public, shareholders, especially institutional investors and hedge funds, will scrutinize the offer intensely. If the premium is substantial and the market believes the offer is fair, these shareholders will not hesitate to voice their opinions, often publicly, demanding that the board engage with the acquirer or accept the offer. Activist investors, who specialize in pushing for corporate change to unlock value, may even acquire a stake in the target company specifically to agitate for the acceptance of the bear hug, further complicating the board’s position. This dynamic means the board must not only convince itself of its chosen path but also effectively communicate its rationale to a potentially skeptical and financially motivated shareholder base.

Financial and Strategic Implications

The ripple effects of a bear hug extend far beyond the immediate transaction, impacting financial markets, corporate strategies, and the long-term health of both the acquiring and target entities.

Impact on Share Price and Valuation

The announcement of a bear hug typically causes the target company’s share price to surge, often close to the offer price, reflecting the market’s expectation that the deal will go through. For the acquiring company, the immediate impact can be more mixed. If the market perceives the acquisition as strategically sound and financially beneficial, the acquirer’s stock price might rise. However, if the premium is considered excessive, or the financing risky, the acquirer’s share price could fall, reflecting investor concerns about dilution or overpayment. Beyond the immediate effect, the acquisition can permanently alter the market valuation metrics for both companies, depending on how successful the integration proves to be.

Cost of Acquisition and Financing

A bear hug, by its very nature, often involves a significant premium, making the acquisition expensive. The acquirer must carefully consider the financial implications of this cost. How will the deal be financed? Will it involve issuing new equity, taking on substantial debt, or a combination? The choice of financing can have a profound impact on the acquirer’s capital structure, earnings per share, and credit rating. High levels of debt, for instance, can increase financial risk and limit future flexibility. Financial analysts meticulously scrutinize the pro-forma financials of the combined entity to assess the sustainability of the acquisition and its impact on key financial ratios.

Potential Synergies and Integration Challenges

The justification for paying a high premium in a bear hug often rests on the promise of substantial synergies – cost savings, revenue enhancements, or operational efficiencies that the combined entity can achieve. These synergies are the financial lifeblood of many M&A deals. However, realizing these synergies is notoriously difficult. Post-acquisition integration is a complex and challenging process, fraught with cultural clashes, operational disruptions, and unforeseen costs. Failure to effectively integrate the target company can erode the financial benefits of the acquisition, turning an initially attractive deal into a value-destroying venture. The acquirer must have a robust integration plan and a clear strategy for unlocking the promised financial value.

Regulatory Scrutiny and Market Perception

Large-scale acquisitions, especially those initiated via a bear hug, frequently attract the attention of regulatory bodies. Antitrust authorities, for instance, will scrutinize the deal to ensure it does not create a monopoly or unfairly reduce competition within a market. Regulatory delays or requirements for divestitures can add significant costs and uncertainty to the transaction. Beyond regulation, the market’s perception of the deal is crucial. A poorly executed bear hug, or one perceived as exploitative, can damage the acquirer’s reputation, affecting its stock price, its ability to attract talent, and its future M&A prospects. Conversely, a successful and well-received bear hug can enhance an acquirer’s standing as a savvy and aggressive market player.

In conclusion, a bear hug in business is a powerful, high-stakes financial strategy in the world of M&A. It’s an aggressive, unsolicited, and often public offer designed to compel a target company’s board and shareholders to accept a takeover, typically by offering a substantial financial premium. For the acquiring firm, it’s a strategic weapon to overcome resistance and expedite access to valuable assets or markets, while for the target, it represents an existential moment demanding rigorous financial evaluation, adherence to fiduciary duties, and swift strategic decision-making. The financial implications are profound, affecting valuations, capital structures, integration challenges, and market dynamics for all parties involved. Understanding the nuances of a bear hug is essential for anyone navigating the intricate landscape of corporate finance and investment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.