Navigating the landscape of business finance requires a keen understanding of various regulatory requirements, tax obligations, and reporting standards. Among the most critical documents for any employer in the United States is IRS Form 941, officially titled the “Employer’s Quarterly Federal Tax Return.” For many business owners, this form is a recurring milestone that dictates the health of their relationship with the Internal Revenue Service and ensures that the financial machinery of the national social safety net continues to function.

Understanding what a 941 is goes beyond simply filling out boxes on a page; it involves a comprehensive grasp of payroll management, tax liability, and the fiduciary responsibility of holding funds in trust for employees. In this guide, we will explore the intricacies of Form 941, the financial implications of non-compliance, and the strategies businesses use to streamline their quarterly reporting.

Understanding the Fundamentals of IRS Form 941

At its core, Form 941 is the mechanism by which employers report the taxes they have withheld from their employees’ paychecks, as well as the employer’s share of Social Security and Medicare taxes. Because the United States operates on a “pay-as-you-go” tax system, the IRS requires these reports quarterly rather than annually to ensure a steady flow of revenue and to monitor business compliance in real-time.

Who is Required to File?

Most businesses that pay wages to an employee must file Form 941 every quarter. This remains true even if the business has no taxes to report for a specific quarter, provided they are still an active business entity. There are very few exceptions to this rule. Seasonal employers only file for quarters in which they paid wages, and small employers with an annual tax liability of $1,000 or less may be permitted to file Form 944 (an annual return) instead of the quarterly 941. Additionally, employers of household employees or agricultural workers generally use different forms.

The Quarterly Filing Cycle

The financial calendar for a business is punctuated by the four deadlines for Form 941. These deadlines fall on the last day of the month following the end of the quarter:

- Quarter 1 (Jan–Mar): Due April 30

- Quarter 2 (Apr–Jun): Due July 31

- Quarter 3 (Jul–Sep): Due October 31

- Quarter 4 (Oct–Dec): Due January 31

If an employer has made timely deposits in full payment of their taxes for the quarter, they may be granted an additional 10 days to file. From a business finance perspective, missing these dates is not just a clerical error; it is a significant financial risk that can lead to compounding interest and penalties.

Breaking Down the Components of the 941 Form

To manage business finance effectively, one must understand exactly what the IRS is looking for within the 941. The form is divided into several parts that reconcile the total wages paid with the amount of tax owed.

Reporting Employee Wages and Tips

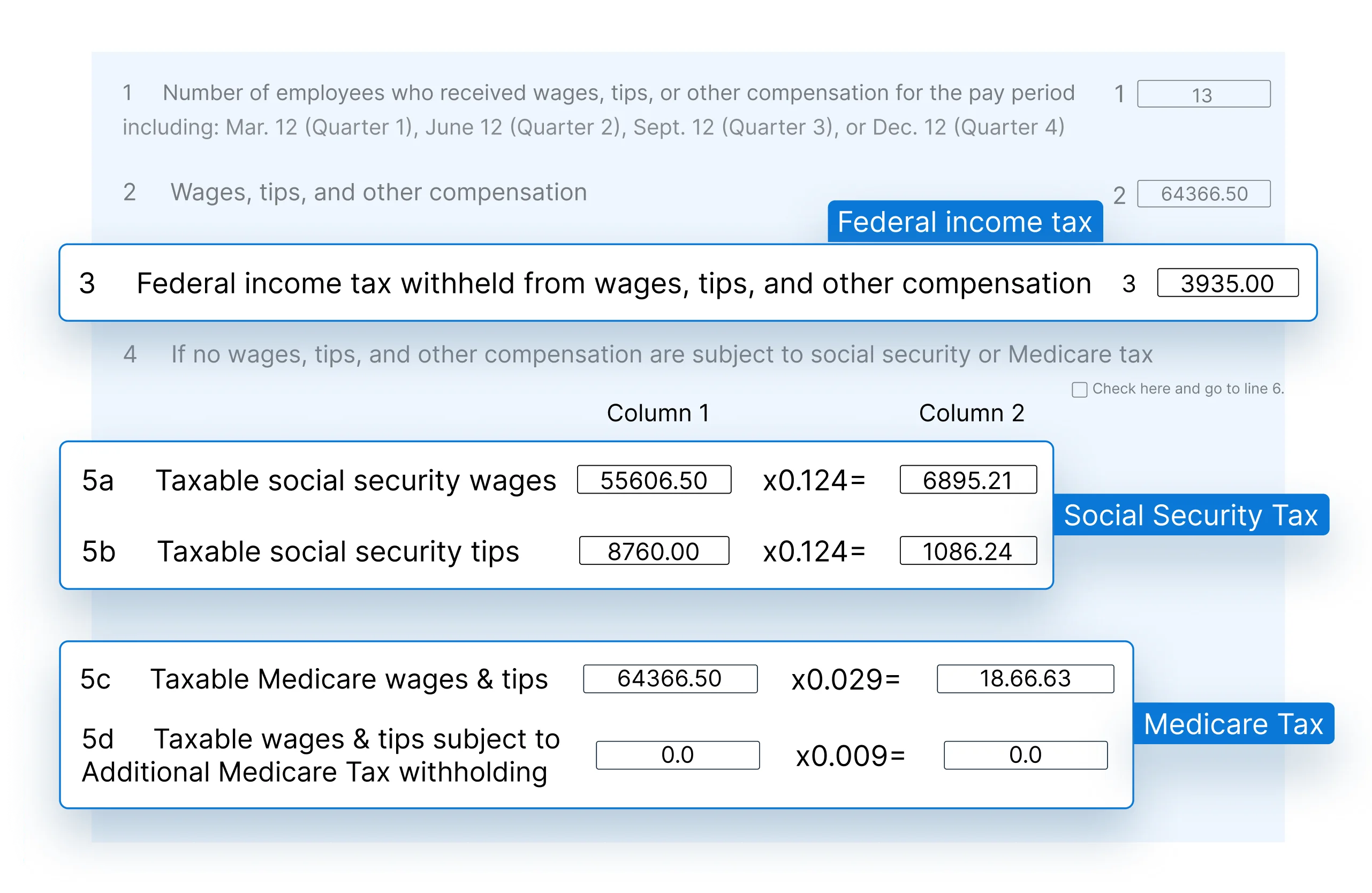

The first section of the form requires the employer to disclose the total number of employees paid during the period and the total compensation distributed. This includes wages, tips, sick pay, and taxable fringe benefits. This figure serves as the baseline for all subsequent tax calculations. Accuracy here is paramount, as this data is cross-referenced with the W-2 forms issued at the end of the year.

Calculating Federal Income Tax and FICA Taxes

Form 941 is the primary tool for calculating Federal Insurance Contributions Act (FICA) taxes, which consist of Social Security and Medicare.

- Social Security Tax: Both the employer and the employee pay 6.2% of the employee’s gross wages (up to the annual wage base limit).

- Medicare Tax: Both parties pay 1.45% of all wages, with no wage limit.

- Additional Medicare Tax: Employers are also responsible for withholding an additional 0.9% for employees earning over a certain threshold ($200,000 for individuals), though the employer does not match this specific portion.

The form allows the IRS to see the “total taxes” before adjustments, creating a clear financial snapshot of the company’s payroll liability for that three-month window.

Adjustments and Credits

Business finance is rarely a straight line, and Form 941 accounts for this through adjustments. Employers can adjust for fractions of cents (rounding), sick pay, or group-term life insurance. More importantly, this section is where businesses claim credits. In recent years, this has included significant provisions like the Employee Retention Credit (ERC) or credits for qualified sick and family leave wages. These credits can significantly offset the total tax liability, making the 941 a tool for capital preservation when managed correctly.

The Financial Impact of Compliance and Deadlines

In the world of business finance, cash flow is king. Form 941 represents a significant “trust fund” liability—money that the employer holds but does not own. Failure to manage these funds correctly can lead to severe consequences for the business’s bottom line and the personal liability of its owners.

Penalties for Late Filing or Payment

The IRS is particularly aggressive regarding payroll taxes because a portion of the money (the employee’s withholding) belongs to the employees and the government. The “Failure to File” penalty is generally 5% of the tax due for each month or part of a month that the return is late, capping at 25%.

The “Failure to Pay” penalty is 0.5% of the unpaid tax for each month it remains unpaid. When you combine these with market-based interest rates, a late filing can quickly snowball into a financial crisis. For a growing business, these avoidable costs can drain the capital needed for expansion or operations.

The Trust Fund Recovery Penalty (TFRP)

One of the most daunting aspects of payroll tax finance is the Trust Fund Recovery Penalty. If a business fails to pay the withheld income and FICA taxes, the IRS can hold “responsible persons” personally liable. This means that business owners, officers, or even employees with check-signing authority can be forced to pay the tax out of their personal assets. Understanding the 941 is, therefore, a matter of personal financial security for those at the helm of a company.

Modernizing the Filing Process with Financial Tools

As businesses scale, the manual calculation of Form 941 becomes risky and inefficient. Modern financial tools and software integrations have transformed how companies approach this quarterly obligation, turning a complex chore into a streamlined workflow.

E-filing vs. Paper Filing

While the IRS still accepts paper forms, the vast majority of modern businesses utilize e-filing. Electronic filing provides an immediate receipt of confirmation, reducing the “lost in the mail” anxiety that often accompanies tax season. From a financial management perspective, e-filing also allows for more precise scheduling of payments through the Electronic Federal Tax Payment System (EFTPS), ensuring that funds leave the company’s bank account exactly when intended, neither too early (impacting liquidity) nor too late (incurring penalties).

Integrating Payroll Software for Accuracy

The most effective way to handle 941 obligations is through integrated payroll software. These financial tools automatically track employee hours, calculate withholdings based on the latest tax tables, and aggregate the data required for the quarterly return. By automating the data entry process, businesses eliminate human error, which is the leading cause of 941 discrepancies. This integration ensures that the “Tax” line item in the company’s general ledger always matches the amount reported to the IRS, simplifying audits and year-end reconciliations.

Best Practices for Managing Your Quarterly Tax Liabilities

To maintain a healthy financial standing, businesses should view Form 941 management as a continuous process rather than a quarterly “sprint.” Implementing a few structural best practices can ensure that the filing process is a non-event.

Reconciling Payroll Records Regularly

A common mistake in business finance is waiting until the end of the quarter to look at payroll totals. Successful firms perform monthly reconciliations, comparing their payroll reports to their bank statements and tax deposit records. This practice allows for the early detection of errors, such as misclassified employees or incorrect withholding rates, before they are formalized on a 941 filing.

Establishing a Tax Escrow Account

One of the most effective strategies for managing the cash flow impact of payroll taxes is the use of a separate tax escrow account. By transferring the employer and employee portions of payroll taxes into a separate account every time payroll is run, a business ensures that it never “accidently” spends tax money on operating expenses. This discipline protects the business from liquidity crises when the 941 due date arrives, as the funds are already set aside and accounted for.

Preparing for Year-End with 941 Data

The data reported on the four quarterly 941 forms must eventually reconcile with the annual Form W-3 (Transmittal of Wage and Tax Statements). If the sum of the four 941s does not match the W-3, the IRS will likely trigger an inquiry. By maintaining rigorous 941 records throughout the year, a business prepares itself for a seamless year-end closing, reducing the administrative burden on the finance team and ensuring the company’s tax record remains spotless.

In conclusion, Form 941 is a cornerstone of American business finance. It is the bridge between a company’s payroll operations and its federal tax obligations. By understanding the components of the form, respecting the deadlines, and utilizing modern financial tools, business owners can ensure compliance, protect their cash flow, and focus their energy on growing their enterprise. Whether you are a small startup or an established corporation, mastering the 941 is an essential step in professional financial management.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.