Navigating the complexities of the tax code is a fundamental skill for any serious investor or business owner. Among the various documents required by the Internal Revenue Service (IRS), Form 8949, “Sales and Other Dispositions of Capital Assets,” stands as one of the most critical for those managing a portfolio. Whether you are trading individual stocks, holding long-term real estate, or venturing into the volatile world of cryptocurrency, Form 8949 is the primary vehicle for detailing your investment activity.

This article provides an in-depth exploration of Form 8949, its role in your personal finance strategy, and how to accurately report your financial transactions to ensure compliance while optimizing your tax liability.

What is Form 8949 and Why Does It Matter for Your Taxes?

In the realm of personal finance and investing, every transaction has a tax consequence. Form 8949 is the IRS document used to report the details of every sale or exchange of a capital asset. While many taxpayers are familiar with Schedule D, which summarizes capital gains and losses, Form 8949 is the granular workhorse where the “heavy lifting” of data entry occurs.

The Purpose of Form 8949

The primary purpose of Form 8949 is to provide the IRS with a transparent record of your capital asset transactions. A capital asset generally includes almost everything you own and use for personal or investment purposes. When you sell these assets, the difference between what you paid (the cost basis) and what you received (the proceeds) results in either a capital gain or a capital loss. Form 8949 allows the IRS to verify these figures against the information reported by your broker on Form 1099-B.

Who Needs to File This Form?

If you sold stocks, bonds, or mutual funds during the tax year, you will likely need to file Form 8949. However, the scope of this form extends far beyond traditional equities. Individuals, partnerships, corporations, and trusts must use this form to report:

- The sale or exchange of capital assets not reported on another form.

- Gains from involuntary conversions (other than from casualty or theft).

- The non-business bad debts.

- The worthlessness of a security.

- The election to defer capital gains by investing in a Qualified Opportunity Fund (QOF).

Understanding who needs to file is the first step in avoiding costly penalties and ensuring that your financial reporting aligns with your investment strategy.

Navigating the Mechanics: How to Fill Out Form 8949

Completing Form 8949 requires meticulous record-keeping and a clear understanding of your investment timeline. The form is divided into two main parts: Part I for short-term transactions and Part II for long-term transactions. This distinction is vital because short-term gains are taxed at ordinary income rates, while long-term gains often benefit from preferential tax rates.

Identifying Your Assets: Part I and Part II

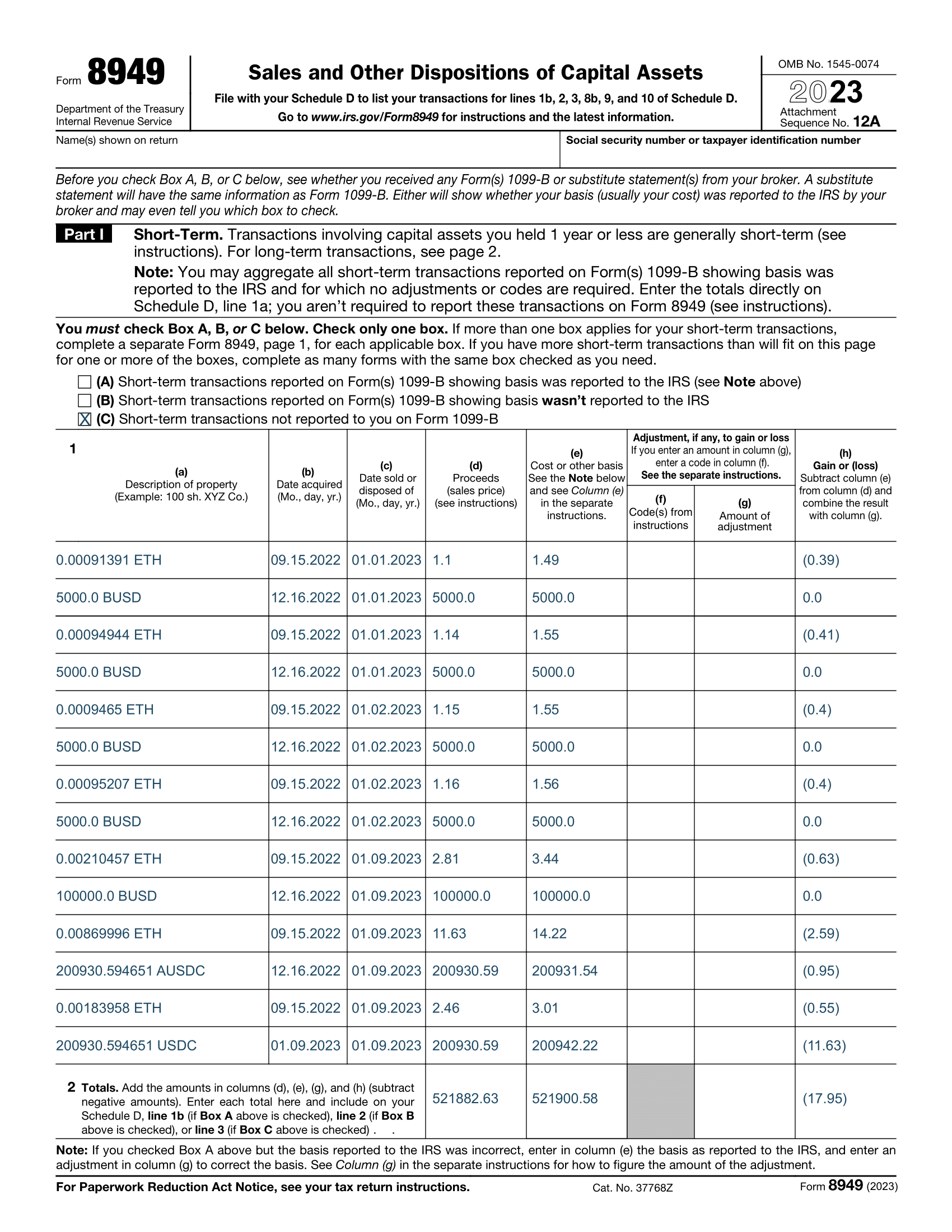

A short-term capital gain or loss occurs on assets held for one year or less. These are reported in Part I. Conversely, long-term gains or losses occur on assets held for more than one year and are reported in Part II. Within each part, you must further categorize transactions based on whether the cost basis was reported to the IRS by your broker. You will check one of three boxes (A, B, or C for short-term; D, E, or F for long-term) depending on whether you received a 1099-B and whether that form showed the cost basis.

Decoding the Columns: From Description to Cost Basis

The form consists of several columns (a through h) that must be filled out for every transaction:

- Column (a): Description of the property (e.g., “100 shares of XYZ Corp”).

- Column (b): Date acquired.

- Column (c): Date sold or disposed of.

- Column (d): Proceeds (the total amount you received from the sale).

- Column (e): Cost or other basis (what you originally paid plus adjustments).

- Column (h): Gain or loss (Column d minus Column e, plus or minus adjustments in Column g).

Accuracy in Column (e) is particularly important. Many investors overlook “adjustments” to their cost basis, such as commissions, fees, or stock splits, which can inadvertently lead to overpaying taxes.

Understanding Adjustment Codes

Column (f) and (g) are reserved for “Codes” and “Amount of Adjustment.” These are used when the math isn’t straightforward. For example, if you are claiming a wash sale loss disallowance, you would enter code “W.” If you are reporting a gain from a QOF, or if the basis reported on your 1099-B is incorrect, these columns allow you to reconcile the discrepancy. Mastering these codes is a hallmark of sophisticated financial management, as it ensures your reported taxable income is as accurate as possible.

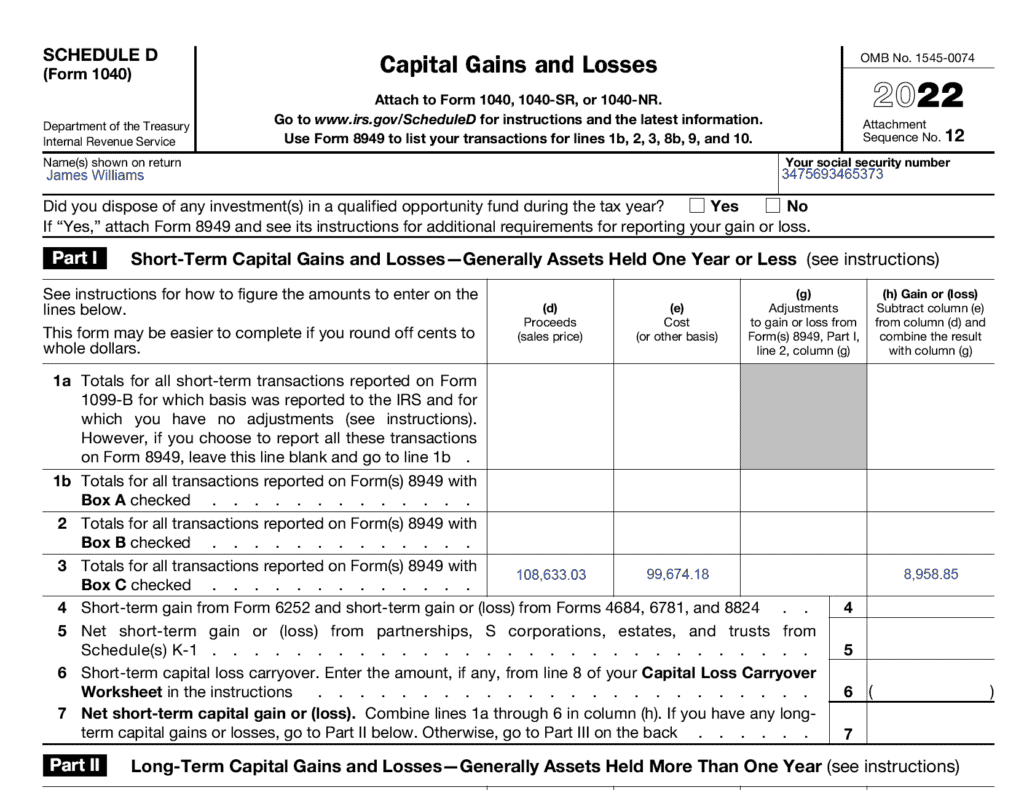

The Vital Link Between Form 8949 and Schedule D

It is common for taxpayers to confuse Form 8949 with Schedule D, but in the world of professional finance, they serve distinct, complementary roles. Think of Form 8949 as the “ledger of details” and Schedule D as the “executive summary.”

How Data Flows to Schedule D

Once you have listed every individual transaction on Form 8949 and calculated the totals for each category, those totals are transferred to the corresponding lines on Schedule D. For example, the total short-term gain or loss from Form 8949, Part I, is moved to the short-term section of Schedule D. This flow of information allows the IRS to see the big picture of your net capital position without having to scan through hundreds of individual trades on the summary page.

Why You Can’t Have One Without the Other

For the vast majority of investors, Schedule D cannot be completed without first finishing Form 8949. While there are a few exceptions—such as when a taxpayer has no adjustments and the broker reported all basis information to the IRS—most active investors will find that Form 8949 is mandatory. Failing to include Form 8949 when required can lead to “mismatch” notices from the IRS, where their automated systems flag the discrepancy between your 1099-B and your tax return, often resulting in a higher tax bill and interest charges.

Common Challenges and Strategy: Maximizing Tax Efficiency

Reporting your transactions is more than a compliance exercise; it is an opportunity to analyze your investment performance and implement tax-saving strategies like tax-loss harvesting. However, several modern complexities can make Form 8949 particularly challenging.

Handling Wash Sales and Complex Transactions

One of the most frequent hurdles in personal finance is the “Wash Sale Rule.” This occurs when you sell a security at a loss and buy a “substantially identical” security within 30 days before or after the sale. The IRS prevents you from claiming that loss immediately; instead, the loss is deferred and added to the basis of the new security. On Form 8949, this must be meticulously tracked using adjustment codes to ensure you aren’t claiming disallowed losses, which could trigger an audit.

The Impact of Cryptocurrency and Digital Assets

In recent years, the IRS has significantly increased its focus on digital assets. Every time you sell cryptocurrency, trade one coin for another, or use crypto to purchase a good or service, it is considered a “disposition of a capital asset.” These transactions must be reported on Form 8949. Because many crypto exchanges do not provide the same level of 1099-B reporting as traditional brokerages, the burden of tracking cost basis and holding periods falls entirely on the investor. Utilizing specialized financial tools to track these transactions is essential for maintaining accurate records.

Best Practices for Record Keeping and Accuracy

The key to mastering Form 8949 is proactive record-keeping. Investors should:

- Maintain a Transaction Log: Don’t wait until April to gather your trade data. Keep a running tally of buy/sell dates and prices.

- Review 1099-Bs Early: Check your brokerage statements for errors in cost basis reporting. If the broker is wrong, you must correct it on Form 8949 using the appropriate adjustment code.

- Leverage Technology: For those with hundreds or thousands of trades, manual entry is nearly impossible. Use tax software or financial management tools that allow for the direct import of brokerage data into Form 8949.

- Consider Tax-Loss Harvesting: At the end of the year, review your Form 8949 data. If you have significant gains, you might choose to sell underperforming assets at a loss to offset those gains, thereby reducing your overall tax liability.

In conclusion, Form 8949 is a cornerstone of investment taxation. By understanding its structure, its relationship with Schedule D, and the nuances of reporting various asset classes, you can navigate tax season with confidence. More importantly, a deep understanding of these forms allows you to make more informed financial decisions, ensuring that you keep more of your hard-earned investment returns. High-level wealth management is as much about what you keep as what you earn, and Form 8949 is the primary tool for managing the “what you keep” side of the equation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.