In the world of high-stakes finance, precision is not merely a preference; it is a requirement. Whether you are calculating the interest on a multi-million dollar commercial loan, evaluating the yield of a treasury bond, or analyzing stock market fluctuations, the ability to transition between fractions and decimals is a fundamental skill. At first glance, the question “What is 4 and 3/4 as a decimal?” appears to be a simple arithmetic exercise. However, in the context of the “Money” niche—encompassing personal finance, institutional investing, and global economics—this figure (4.75) represents a critical threshold for interest rates, dividend yields, and market spreads.

The Mathematical Foundation of Finance: Why 4.75 Matters

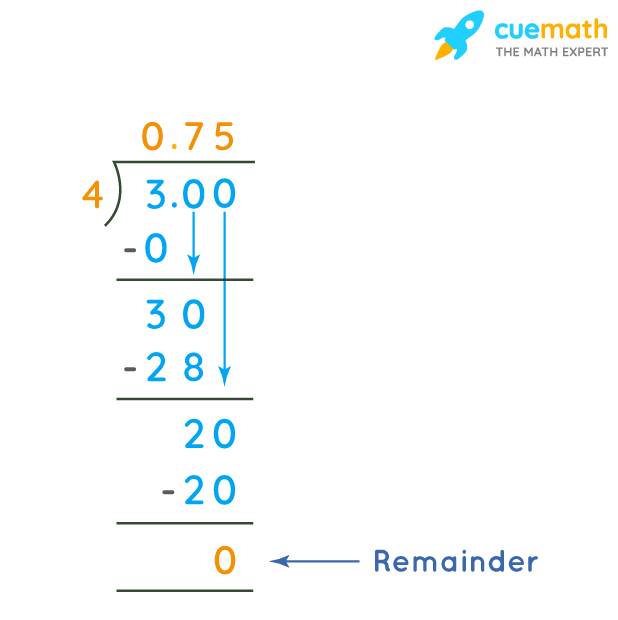

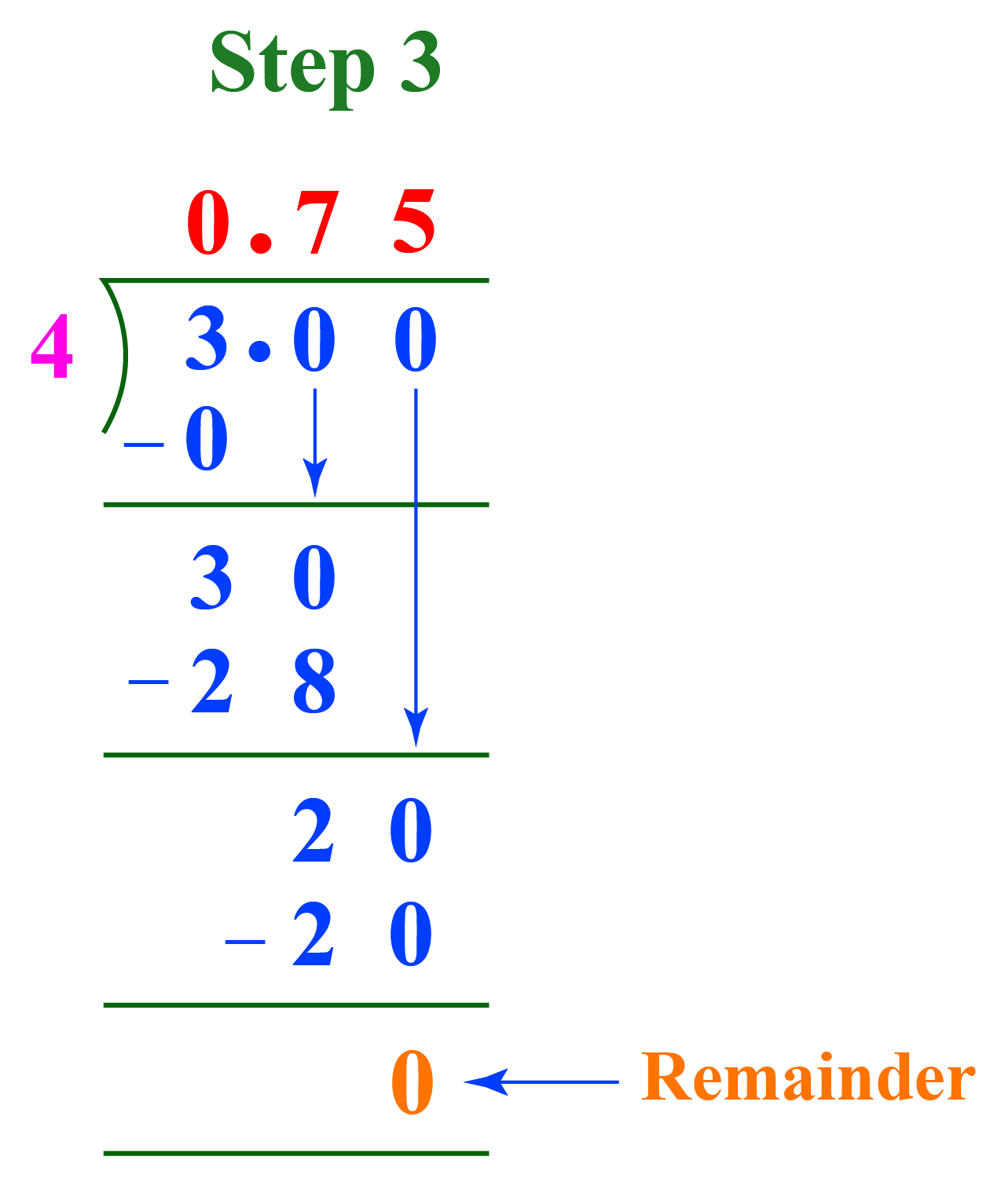

To understand the financial implications of 4 and 3/4, we must first establish the conversion with absolute clarity. In mathematical terms, a mixed fraction consists of a whole number and a proper fraction. To convert 4 and 3/4 into a decimal, one must divide the numerator (3) by the denominator (4), which yields 0.75. When added to the whole number, the result is 4.75.

While the conversion itself is elementary, its application in the financial sector is profound. In the realm of monetary policy, a movement of “three-quarters of a percent” is often the difference between economic expansion and a controlled cooling of the markets.

From Fractions to Decimals: The Conversion Process

The conversion of 4 3/4 to 4.75 is the bridge between traditional verbal financial terminology and modern digital computation. Historically, many financial instruments were quoted in fractions. From the floor of the New York Stock Exchange to the local bank branch, “four and three-quarters” was a standard linguistic shorthand. In a digital-first economy, however, algorithms and spreadsheets require the decimal format (4.75) to execute complex compounding formulas and risk assessments.

The Significance of the “Quarter Point” in Global Markets

In central banking, particularly regarding the Federal Reserve’s federal funds rate, changes are often measured in “basis points.” One basis point is equal to 1/100th of 1 percent, or 0.01%. Therefore, 4 and 3/4 percent is equivalent to 475 basis points. When an economy faces inflation, a hike to 4.75% represents a significant tightening of credit. For investors, recognizing that 4 3/4 is 4.75 is the first step in calculating how much more expensive it will be for corporations to debt-finance their operations.

Applications in Real Estate and Mortgages

Perhaps nowhere is the fraction 4 3/4 more prevalent than in the real estate sector. For decades, mortgage lenders have quoted interest rates in eighths or quarters of a percent. If a prospective homeowner is offered a rate of 4 and 3/4%, they are looking at a decimal rate of 4.75%. While the difference between 4.5% and 4.75% might seem negligible to the untrained eye, the long-term financial implications are staggering.

Understanding Basis Points and Interest Rates

When a lender discusses a “25 basis point” increase, they are moving the rate from 4.50% to 4.75%. In the “Money” niche, understanding this decimal conversion is vital for debt management. A 4.75% interest rate on a 30-year fixed mortgage of $500,000 results in significantly higher lifetime interest payments compared to a 4.00% rate. The decimal 4.75 allows borrowers to use online amortization calculators to visualize their equity growth over time.

How a 0.75 Difference Impacts Long-Term Amortization

The “3/4” or “.75” component of 4.75% is the engine of the amortization schedule. On a standard $300,000 loan, the difference between a 4% rate and a 4.75% rate can amount to tens of thousands of dollars over thirty years. By converting the fraction to a decimal, financial planners can accurately project the total cost of capital, allowing for more informed decisions regarding whether to pay “points” upfront to buy down the rate.

Stock Market Evolution: From Fractional Pricing to Decimalization

The transition from 4 3/4 to 4.75 mirrors the historical evolution of the stock market itself. Younger investors may be surprised to learn that until the early 2000s, stock prices on the New York Stock Exchange (NYSE) were quoted in fractions. A stock might have been trading at 4 3/4 per share rather than $4.75.

A Brief History of Trading in Eighths

This system originated from the Spanish “pieces of eight,” where doubloons were physically cut into halves, quarters, and eighths. For centuries, the “teenies” (1/16ths) and “eighths” (1/8ths) governed Wall Street. A stock moving from 4 1/2 to 4 3/4 represented a significant gain. However, this system was inefficient and widened the “spread”—the difference between the bid and ask price—which essentially functioned as a hidden cost for retail investors.

Modern Precision and the Liquidity of Decimals

In 2001, the “decimalization” of the U.S. markets changed everything. By moving from 4 3/4 to 4.75, the markets allowed for “sub-pennying,” where stocks could be traded in increments of $0.01 or even $0.0001. This increased liquidity and narrowed spreads, saving investors billions of dollars annually. Today, seeing 4.75 on a trading terminal is the standard, but it represents the same value that once required a working knowledge of fractions to navigate the exchange floor.

Personal Finance and Yield Calculations

For the individual investor, the number 4.75 often appears in the context of “yield.” Whether it is a High-Yield Savings Account (HYSA), a Certificate of Deposit (CD), or a corporate bond, 4 and 3/4 percent is a common benchmark for “safe” returns during periods of moderate interest rates.

Calculating Annual Percentage Yield (APY)

When a bank advertises a rate of 4 and 3/4, the savvy consumer must look at the APY (Annual Percentage Yield). If the interest is compounded monthly, the effective rate will be slightly higher than the nominal decimal rate of 4.75. By using the decimal 4.75 in the compound interest formula—$A = P(1 + r/n)^{nt}$—investors can determine exactly how much their money will grow over a five or ten-year period.

The Psychology of “Four and Three-Quarters” vs. “4.75%”

In marketing financial products, there is a distinct psychology behind how numbers are presented. Some institutions use the fractional “4 3/4” to evoke a sense of traditional stability and “old-school” banking reliability. Others use “4.75%” to appeal to tech-savvy, data-driven investors who prioritize transparency and digital integration. Regardless of the branding, the underlying value remains identical, and the ability to convert between the two ensures the consumer is never misled by presentation.

Strategic Tools for Financial Conversion

To maintain an edge in business finance and investing, one must utilize tools that handle these conversions with 100% accuracy. Relying on mental math for a 4 3/4 conversion is acceptable for a quick estimate, but formal financial reporting requires more robust methods.

Financial Calculators and Spreadsheet Mastery

In platforms like Microsoft Excel or Google Sheets, entering “4 3/4” can sometimes result in formatting errors where the software treats the entry as a date. Financial professionals instead input “=4+(3/4)” or simply “4.75” and format the cell as a percentage. This ensures that subsequent formulas—such as those calculating Net Present Value (NPV) or Internal Rate of Return (IRR)—pull the correct numerical value.

Avoiding Rounding Errors in High-Stakes Accounting

In corporate finance, rounding 4.75% to 4.8% or 5% is an unacceptable practice. On a corporate bond issue of $100 million, a rounding error of just 0.05% (5 basis points) results in a $50,000 discrepancy per year. By strictly adhering to the decimal 4.75, accountants and treasurers ensure that the books balance and that fiduciary responsibilities are met.

Conclusion: The Power of 4.75 in Your Financial Toolkit

While the question “What is 4 and 3/4 as a decimal?” begins as a simple math problem, its answer—4.75—is a cornerstone of modern financial literacy. From the way we price our homes to the way the world’s largest corporations trade debt, this decimal represents a specific, measurable value that dictates the flow of capital.

By mastering the conversion from 4 3/4 to 4.75, you are doing more than solving a fraction; you are equipping yourself with the language of the markets. Whether you are an entrepreneur looking at a 4.75% business loan or a retiree seeking a 4 3/4% dividend yield, understanding this number allows you to calculate risk, project growth, and navigate the complex world of money with confidence and precision. In finance, every decimal point counts, and 4.75 is a number that carries significant weight in the pursuit of wealth and economic stability.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.