For the vast majority of aspiring homeowners, the “30-year mortgage rate” is more than just a financial statistic; it is the most critical variable in the equation of affordability. As the standard benchmark for home financing in the United States, the 30-year fixed-rate mortgage offers a unique blend of stability and accessibility. However, despite its ubiquity, the mechanics behind how these rates are set, why they fluctuate, and how they impact long-term wealth accumulation remain complex.

Understanding the 30-year mortgage rate requires a deep dive into the intersection of personal finance, macroeconomics, and the global bond market. Whether you are a first-time buyer or a seasoned real estate investor, mastering this topic is essential for making informed financial decisions.

What is a 30-Year Mortgage Rate and How Does It Work?

At its core, a 30-year mortgage rate is the interest rate charged on a home loan that is scheduled to be repaid over a period of 360 months. The “fixed-rate” nature of this product means that the interest rate established at the time of closing remains constant for the entire life of the loan. This provides the borrower with a predictable monthly payment, shielding them from the volatility of the financial markets.

The Definition of a Fixed-Rate Mortgage

The 30-year fixed-rate mortgage is a debt instrument where the interest rate does not change. Unlike adjustable-rate mortgages (ARMs), which can fluctuate based on market indices, the fixed-rate option ensures that if you lock in a rate of 6%, it will remain 6% in year one, year fifteen, and year thirty. For the borrower, this translates to “inflation-proof” housing costs. While the price of consumer goods, taxes, and insurance may rise over three decades, the principal and interest portion of the mortgage payment remains a static line item in the household budget.

How Amortization Shapes Your Monthly Payments

To understand the 30-year rate, one must understand amortization. In the early years of a 30-year mortgage, a significant majority of the monthly payment is directed toward interest, with only a small fraction reducing the principal balance. As the loan matures, this ratio shifts. By the final decade of the loan, the bulk of the payment is applied to the principal. This structure is why the 30-year rate is so sensitive to changes: even a 1% increase in the rate can result in tens of thousands of dollars in extra interest paid over the life of the loan due to the extended repayment timeline.

Why the 30-Year Term is the Gold Standard

The 30-year term is the most popular choice in the United States because it spreads the debt over a long horizon, resulting in lower monthly payments compared to 10-year or 15-year loans. This “affordability cushion” allows buyers to qualify for larger loan amounts, effectively increasing their purchasing power in competitive real estate markets. From a personal finance perspective, it also provides flexibility; a borrower can choose to pay extra toward the principal to retire the debt early, but they are not contractually obligated to the higher payments required by shorter-term loans.

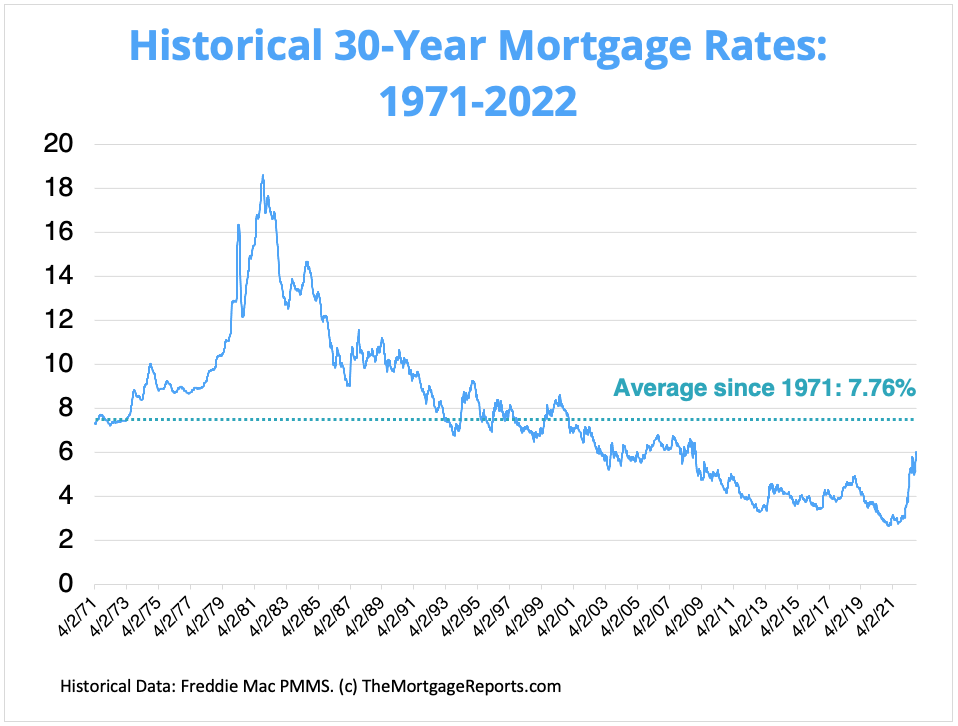

The Economic Drivers Behind Mortgage Rate Fluctuations

Many consumers mistakenly believe that the Federal Reserve directly sets mortgage rates. In reality, mortgage rates are determined by the secondary market, where mortgages are bundled into Mortgage-Backed Securities (MBS) and sold to investors. Because investors demand a certain “yield” or return for the risk of lending money, mortgage rates move in response to broader economic signals.

The Influence of the Federal Reserve and Monetary Policy

While the Federal Reserve does not set mortgage rates, its influence is profound. The Fed manages the federal funds rate—the interest rate banks charge each other for overnight loans. When the Fed raises rates to combat inflation, it increases the cost of borrowing across the entire economy. This ripple effect typically pushes mortgage rates higher. Conversely, when the Fed lowers rates to stimulate economic growth, mortgage rates often trend downward, making it cheaper for consumers to finance a home.

The Correlation Between the 10-Year Treasury Yield and Mortgage Rates

The most accurate “weather vane” for the 30-year mortgage rate is the 10-year U.S. Treasury yield. Historically, there is a strong correlation between the two. Investors often view mortgages as a slightly riskier alternative to government bonds. Therefore, mortgage rates typically stay about 1.5 to 3 percentage points higher than the 10-year Treasury yield—a gap known as the “spread.” When Treasury yields rise due to strong economic data or shifting investor sentiment, mortgage rates almost always follow suit.

Inflationary Pressures and Investor Appetite

Inflation is the natural enemy of fixed-income investors. Because a 30-year mortgage pays a fixed amount of interest over a long period, high inflation erodes the purchasing power of those future payments. If inflation is expected to rise, investors will demand higher interest rates today to compensate for the decreasing value of the dollar tomorrow. This is why mortgage rates often spike even before the Federal Reserve takes official action; the market is simply “pricing in” the expectation of future inflation.

Comparing the 30-Year Fixed-Rate Mortgage to Other Financing Options

Choosing a 30-year mortgage is a strategic decision that should be weighed against other available financial products. Depending on an individual’s financial goals—whether it is maximizing monthly cash flow or minimizing total interest paid—the 30-year option may or may not be the optimal choice.

15-Year vs. 30-Year Mortgages: Speed vs. Affordability

The primary alternative to the 30-year mortgage is the 15-year fixed-rate mortgage. The 15-year option typically carries a lower interest rate because the lender is exposed to risk for a shorter duration. The financial benefit is massive: a borrower can save hundreds of thousands of dollars in interest and build equity twice as fast. However, the trade-off is a significantly higher monthly payment. For many, the 30-year mortgage acts as a safety net, providing a lower required payment while allowing for voluntary overpayments.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

Adjustable-Rate Mortgages (ARMs) usually offer a lower “teaser” rate for an initial period (such as 5, 7, or 10 years) before the rate begins to adjust based on market conditions. In a high-rate environment, an ARM can be an attractive way to lower initial costs. However, the 30-year fixed-rate mortgage remains the preferred choice for those planning to stay in their homes long-term, as it eliminates the “reset risk” associated with ARMs, where payments could potentially skyrocket if market rates rise in the future.

When to Choose a Longer Repayment Period

The 30-year mortgage is often the best choice for individuals who prioritize liquidity. By keeping the mandatory mortgage payment low, homeowners can redirect their extra cash flow into high-yield investments, such as the stock market or retirement accounts. If the mortgage rate is lower than the expected return on an investment portfolio, it may actually be mathematically advantageous to carry the 30-year debt rather than rushing to pay it off.

Factors That Determine Your Personal 30-Year Mortgage Rate

While the “national average” 30-year rate is a helpful benchmark, the specific rate an individual receives is highly personalized. Lenders use a process called “risk-based pricing” to determine the interest rate offered to a specific borrower.

Credit Scores and Their Impact on Interest Costs

Your credit score is perhaps the single most influential factor in determining your 30-year mortgage rate. Lenders view higher scores as an indicator of lower default risk. A borrower with a “Very Good” to “Exceptional” score (740+) will typically qualify for the lowest available rates. Conversely, a borrower with a score in the 600s may face a rate that is 1% to 2% higher, which can translate into hundreds of dollars in additional monthly costs. Improving your credit score before applying for a mortgage is one of the most effective ways to build long-term wealth.

The Role of Down Payments and Loan-to-Value (LTV) Ratios

The amount of equity you put into the home upfront also affects your rate. A larger down payment reduces the lender’s Loan-to-Value (LTV) ratio. If you put down 20% or more, you are perceived as a lower-risk borrower, often resulting in a better rate and the elimination of Private Mortgage Insurance (PMI). Small down payments (3% to 5%) are accessible but usually come with “pricing adjustments” that slightly increase the interest rate.

Debt-to-Income (DTI) Ratios and Lender Risk

Lenders also examine your Debt-to-Income (DTI) ratio—the percentage of your gross monthly income that goes toward paying debts. While DTI primarily affects how much you can borrow, an exceptionally high DTI can sometimes lead to higher interest rates or the requirement of “discount points” to offset the lender’s risk. Maintaining a DTI below 36% is generally considered ideal for securing the most competitive terms.

Strategies for Navigating High-Rate Environments

In cycles where the 30-year mortgage rate is elevated, buyers must be more strategic to ensure their home purchase remains a sound investment. There are several financial maneuvers that can help mitigate the impact of high interest rates.

Rate Locks and When to Use Them

Mortgage rates can change daily, and sometimes hourly. Once you find a rate you are comfortable with, a “rate lock” allows you to freeze that rate for a specific period (usually 30 to 60 days) while your loan is processed. This protects you from rate hikes while you are in escrow. Some lenders even offer “lock and shop” programs, allowing you to lock in a rate before you have even found a specific property.

Buying Down the Rate with Discount Points

Borrowers have the option to pay “points” upfront at closing to permanently lower their interest rate. One point typically costs 1% of the total loan amount and reduces the interest rate by approximately 0.25%. This is a “prepayment” of interest. It makes sense if you plan to stay in the home long enough to reach the “break-even point,” where the monthly savings exceed the initial cost of the points.

The Importance of Comparison Shopping Across Lenders

Finally, the 30-year mortgage rate is not a monolithic number. Different lenders—such as big banks, credit unions, and online mortgage brokers—have different overhead costs and “appetites” for risk. Research shows that borrowers who get at least three quotes can save thousands of dollars over the life of their loan. In the world of personal finance, shopping for a mortgage rate is perhaps the highest-ROI activity a consumer can perform.

The 30-year mortgage rate remains the most powerful tool in the American financial arsenal. By understanding the forces that drive it and the personal factors that influence it, you can navigate the housing market with confidence, ensuring that your home serves as both a sanctuary and a cornerstone of your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.