At first glance, “1:10” might appear as a simple numerical expression, an elementary fraction or a basic ratio. However, in the intricate world of finance, this seemingly modest combination of digits holds profound significance. Far from being just an arithmetic curiosity, “1:10” embodies a versatile concept that underpins countless financial principles, from personal budgeting and investment strategy to business analytics and risk management. It represents not just a proportion but often a benchmark, a target, or a critical indicator of financial health and potential.

This article delves into the multifaceted meaning of “1:10” within the financial landscape. We will explore its interpretations across various financial domains, dissecting how this ratio, whether expressed as 1 out of 10, 1/10, or simply 10%, serves as a powerful tool for analysis, decision-making, and goal setting. Understanding “what is 1:10” is to grasp a fundamental building block of financial literacy and strategic planning, empowering individuals and organizations to navigate their economic realities with greater clarity and foresight.

The Core Meaning of 1:10 in Finance

The foundational understanding of “1:10” in finance stems from its mathematical essence: a ratio, a fraction, and ultimately, a percentage. This basic interpretation allows for its broad applicability across diverse financial contexts.

Interpreting Ratios and Fractions

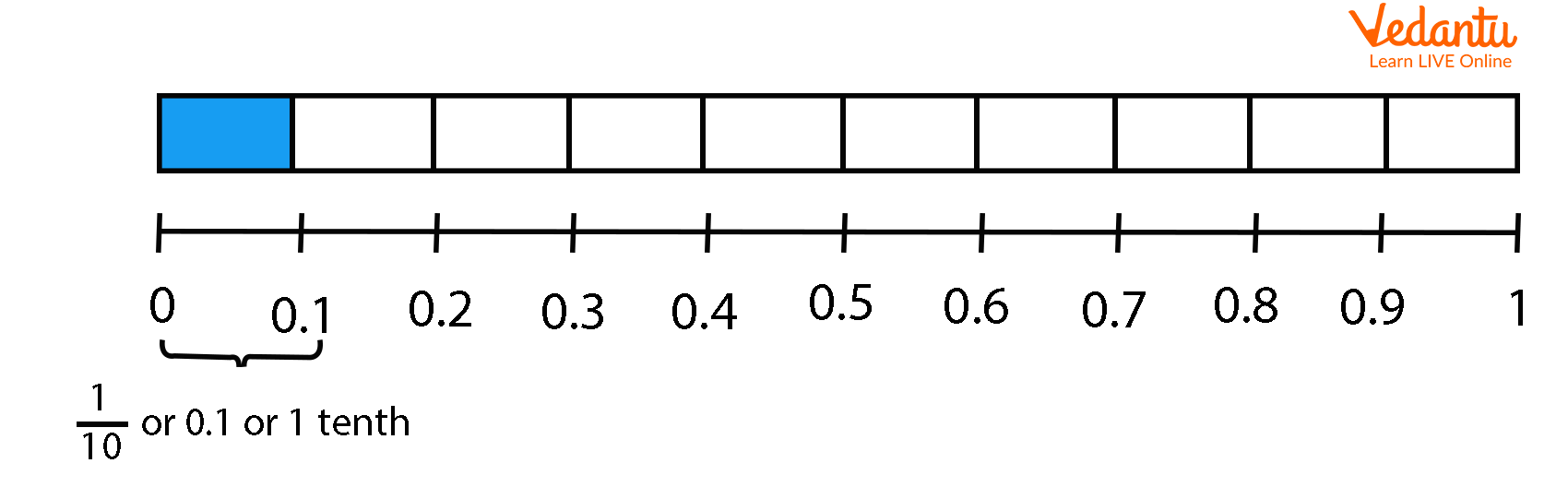

In its purest form, “1:10” signifies a relationship between two quantities where one unit corresponds to ten units of another. As a fraction, 1/10, it denotes one part of a whole divided into ten equal segments. This fundamental understanding is critical because finance is replete with such proportional relationships. Whether we’re talking about a small portion of a larger sum, a specific allocation within a portfolio, or the relative size of one financial metric compared to another, the 1:10 ratio provides a clear, universally understood way to express these relationships. For instance, if you have 10 shares of a company, and you decide to sell 1, you’ve liquidated 1/10th of your holding. This simple arithmetic forms the bedrock of more complex financial calculations.

From Proportion to Percentage

Crucially, the 1:10 ratio is directly convertible into one of the most common and intuitive financial metrics: percentages. One divided by ten equals 0.10, which, when multiplied by 100, gives us 10%. This conversion is vital because percentages offer an easily digestible way to communicate proportions and rates of change, making financial data accessible and comparable. A 10% discount, a 10% interest rate, a 10% growth target—these figures are ubiquitous in financial discussions. The direct translation of 1:10 to 10% allows for seamless integration into budgeting tools, investment reports, and economic analyses, providing a standardized measure that resonates with financial practitioners and laypersons alike.

The Significance of Scale

While 1:10 or 10% might seem a small proportion in isolation, its significance dramatically escalates when applied to large financial scales. A 10% return on a $1,000 investment is $100, which is good. A 10% return on a $1,000,000 investment is $100,000, a substantial gain. Conversely, a 10% loss on a significant sum can be financially devastating. This highlights that the impact of the 1:10 ratio is always relative to the base amount, emphasizing the importance of context in financial interpretations. Whether it’s a minor adjustment in a personal budget or a strategic shift in a multi-billion dollar portfolio, the 10% factor can dictate the magnitude of outcomes.

Applying 1:10 in Personal Finance and Budgeting

For individuals, the “1:10” principle, often expressed as 10%, serves as a potent guideline for cultivating financial discipline, fostering savings habits, and managing debt effectively. It transforms abstract financial goals into concrete, actionable steps.

The 10% Savings Rule

One of the most enduring pieces of financial advice is the “pay yourself first” mantra, often quantified as saving at least 10% of every paycheck. This 10% savings rule, directly embodying the 1:10 principle, is a cornerstone of personal finance. It advocates for setting aside a portion of income for future goals—retirement, a down payment, or an emergency fund—before any other expenses. The power of this rule lies in its consistency and compounding effect. Even a seemingly modest 10% saved regularly over decades can accumulate into a substantial nest egg, providing financial security and freedom. It’s a manageable goal that, when adhered to, dramatically alters one’s long-term financial trajectory.

Debt Management Strategies

The 10% rule also finds its application in debt management. For instance, some financial experts suggest dedicating an additional 10% of disposable income towards accelerated debt repayment. By consistently paying an extra 10% above the minimum required, individuals can significantly reduce the principal amount faster, save on interest, and become debt-free sooner. Furthermore, lenders often consider debt-to-income (DTI) ratios, where a specific percentage of one’s income dedicated to debt payments is deemed healthy. While varying, keeping a DTI below certain thresholds (e.g., 10% for non-mortgage debt, or total DTI including mortgage below 36%) is generally advisable to maintain financial flexibility and creditworthiness, aligning with the “1:10” concept of managing proportional financial obligations.

Budgeting and Expense Allocation

Within a personal budget, the 1:10 principle can guide allocation across various spending categories. While flexible, a 10% allocation might be a reasonable guideline for discretionary spending (like entertainment or dining out), personal development, or even charitable giving. The popular 50/30/20 budgeting rule, for instance, often advises allocating 20% to savings and debt repayment, meaning that a 10% saving goal fits comfortably within a broader framework. By setting a 10% limit or target for specific expense categories, individuals gain better control over their cash flow, preventing overspending in one area from jeopardizing other financial priorities.

1:10 in Investment and Risk Management

In the realm of investments, the “1:10” ratio is particularly powerful, serving as a critical metric for evaluating potential returns, managing risk, and structuring a diversified portfolio.

The Ideal Risk-Reward Ratio

Perhaps one of the most celebrated applications of the 1:10 principle in trading and investing is the concept of the risk-reward ratio. An ideal risk-reward ratio might be 1:2 or 1:3, but a 1:10 risk-reward ratio is often considered the holy grail by astute traders and investors. This ratio implies that for every $1 of capital risked on a trade or investment, the potential profit is $10. Such a favorable ratio suggests a high probability of generating substantial returns even with a relatively low success rate, as a few winning trades can offset multiple small losses. Understanding and actively seeking investments with attractive risk-reward profiles is fundamental to long-term investment success, and 1:10 represents an exceptionally strong proposition in this regard.

Portfolio Allocation and Diversification

The 1:10 ratio, or its 10% equivalent, plays a pivotal role in strategic portfolio allocation. Investors often use 10% as a threshold for individual asset exposure to ensure diversification and manage concentration risk. For instance, limiting any single stock, sector, or alternative investment to no more than 10% of the total portfolio prevents overexposure. If one asset performs poorly, its impact on the overall portfolio is contained, protecting against significant drawdowns. This principle aligns with the wisdom of not putting all your eggs in one basket, advocating for a balanced distribution that minimizes the impact of volatility from any single component.

Understanding Investment Returns

A 10% annual return on investment (ROI) is often considered a respectable benchmark in many investment circles, especially when accounting for inflation. While market conditions vary, consistently achieving a 10% return, particularly through compounding, can lead to significant wealth accumulation over time. The “Rule of 72,” a financial guideline, states that dividing 72 by the annual rate of return gives an approximate number of years it will take for an investment to double. With a 10% return, an investment would double in roughly 7.2 years, illustrating the potent long-term growth potential implied by this ratio.

Business Finance and Operational Insights

Beyond personal wealth, “1:10” or 10% offers invaluable insights in business finance, guiding strategic decisions related to profitability, efficiency, and growth.

Profit Margins and Revenue Targets

For businesses, a 10% profit margin can be a critical benchmark, particularly in competitive industries. It signifies that for every dollar of revenue, 10 cents are converted into profit after all expenses. Achieving or exceeding this margin often indicates strong operational efficiency and pricing power. Similarly, growth targets are frequently framed around a 10% increase year-over-year in revenue, customer base, or market share. These 10% targets serve as motivational goals and performance indicators, driving strategic initiatives and resource allocation within the organization.

Operational Efficiency and Cost Reduction

Businesses constantly seek ways to improve operational efficiency and reduce costs. Identifying opportunities for a 10% reduction in specific operational expenses—such as supply chain costs, energy consumption, or administrative overhead—can have a substantial positive impact on the bottom line. Conversely, a 10% increase in productivity or sales conversion rates can similarly boost profitability. The “1:10” perspective encourages companies to scrutinize their operations, pinpointing areas where marginal improvements can collectively lead to significant financial gains.

Market Share and Customer Acquisition

The pursuit of market dominance often involves setting ambitious yet achievable targets. A company might aim to capture an additional 10% of its target market, or increase its customer acquisition rate by 10%. These metrics, rooted in the 1:10 principle, guide marketing strategies, product development, and sales efforts. Analyzing the 1:10 ratio in terms of customer churn (e.g., losing 1 customer for every 10 acquired) also provides critical insights into customer retention strategies and the overall health of the customer base.

Beyond the Numbers: The Psychology of 1:10

The impact of the “1:10” ratio extends beyond mere mathematical computation; it also taps into the psychology of goal setting, motivation, and perception in financial matters.

Setting Achievable Goals

Framing financial objectives as a 1:10 proportion or a 10% target often makes them seem more manageable and less daunting. Saving 10% of your income, for example, feels more attainable than aiming to save “a lot.” This psychological framing helps overcome inertia and fosters a sense of progress, as hitting small, consistent targets builds momentum towards larger financial ambitions. It breaks down complex, long-term goals into bite-sized, actionable steps.

The Power of Small Increments

The “1:10” principle powerfully illustrates that consistent, incremental efforts yield significant results over time. A 10% annual savings rate, a 10% increase in investment contributions, or a 10% reduction in unnecessary spending—these seemingly small adjustments, compounded year after year, can lead to exponential growth in wealth and financial stability. This emphasizes the importance of patience and perseverance in financial planning, reinforcing that small steps can lead to giant leaps.

Benchmarking and Comparison

Finally, 10% frequently serves as a common benchmark against which performance is measured. How does your investment portfolio’s return compare to the market’s 10% average? Is your company’s profit margin above or below the industry’s 10% standard? This comparative utility helps individuals and businesses assess their financial standing, identify areas for improvement, and celebrate successes. It provides a relatable standard for evaluating financial health and progress against broader expectations.

Conclusion

The seemingly simple expression “what is 1:10?” unveils a surprisingly rich and versatile concept at the heart of finance. From guiding personal savings habits and managing debt to strategizing investment portfolios and driving business profitability, the 1:10 ratio—or its synonymous 10%—serves as a fundamental tool for analysis, planning, and evaluation. It embodies the principles of proportionality, incremental growth, risk management, and achievable goal setting across the entire financial spectrum.

By understanding the core meaning of 1:10, its diverse applications in personal finance, investment, and business, and even its psychological implications, individuals and organizations gain a powerful lens through which to view and master their financial realities. Embracing the wisdom embedded in this fundamental ratio empowers smarter decisions, fosters financial discipline, and ultimately paves the way for greater financial security and success. It is not just a number; it is a blueprint for financial acumen.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.