For many, a dog is a beloved member of the family. However, from a financial and legal perspective, a dog is also a significant liability risk. When a dog bite occurrence moves from a theoretical “what if” to a reality, the owner is suddenly thrust into a complex world of insurance claims, legal defense costs, and potential personal financial ruin. Understanding the fiscal implications of a dog bite is essential for any pet owner who wishes to protect their assets and maintain their long-term financial stability.

This article examines the multifaceted economic consequences of a dog bite incident, focusing on liability, the intricacies of insurance coverage, the long-term impact on personal wealth, and proactive strategies for financial risk mitigation.

Understanding Liability and Immediate Financial Obligations

The moment a dog bite occurs, a clock begins to tick on a series of financial obligations. Depending on the jurisdiction, the dog owner may be held liable under “strict liability” statutes or the “one-bite rule.” Regardless of the legal framework, the immediate costs can be staggering and often require immediate liquidity.

Medical Expenses and Out-of-Pocket Costs

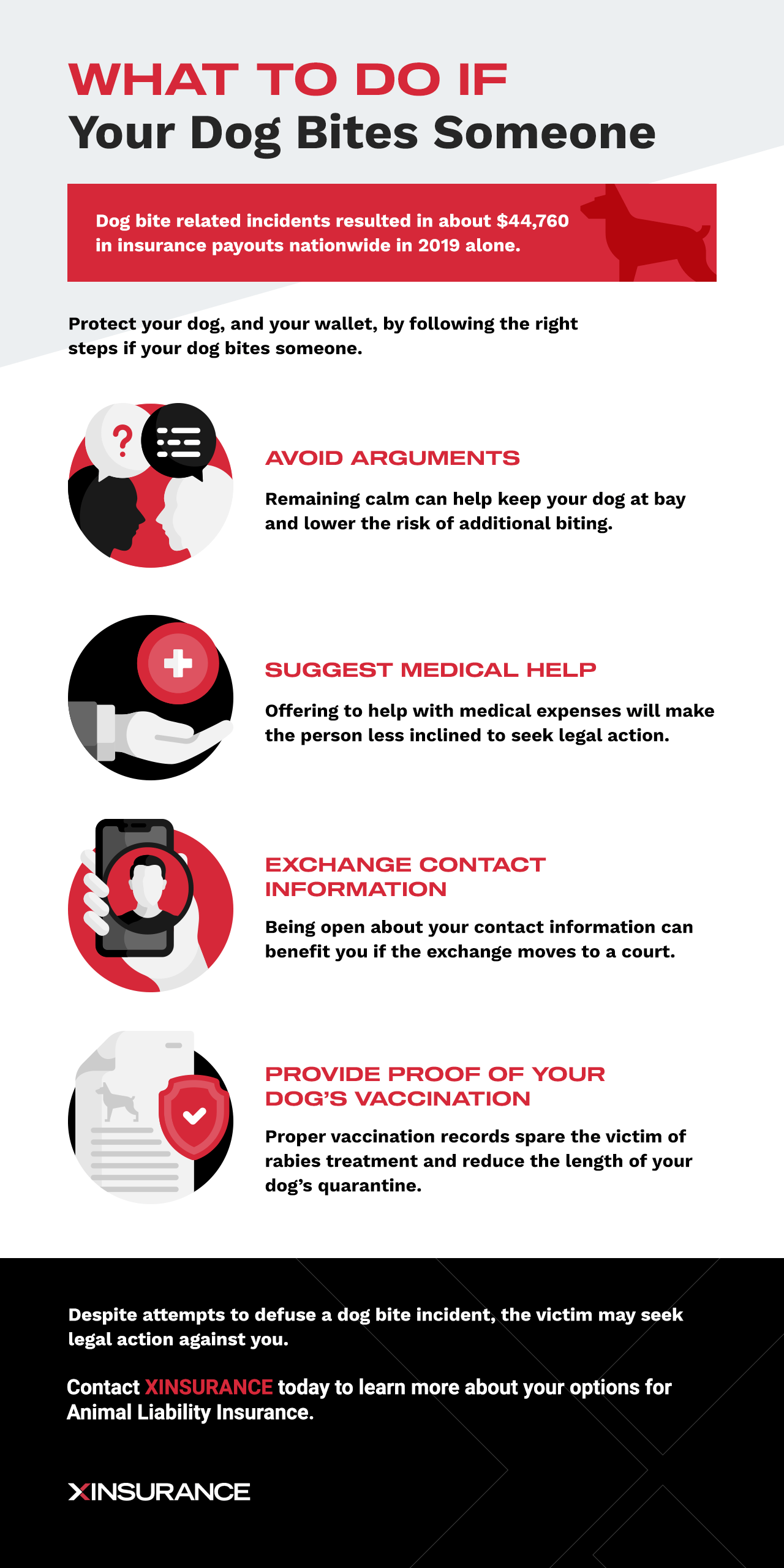

The first and most immediate financial drain is the victim’s medical bills. As the owner, you may be expected to cover emergency room visits, stitches, antibiotics, and follow-up care. In more severe cases, costs escalate into the tens of thousands of dollars if surgery, physical therapy, or psychological counseling for trauma is required. If the victim does not have health insurance, or if their provider seeks subrogation (reimbursement), the financial burden falls squarely on the dog owner. Failing to address these costs early can lead to the victim seeking more aggressive legal recourse, which only increases the total financial outlay.

Legal Fees and Defense Retainers

Even if you believe the bite was provoked or that you are not at fault, you will likely need to hire legal counsel. Defense attorneys specializing in personal injury or animal law often require significant retainers. These professional fees can range from $200 to over $500 per hour. If the case proceeds to discovery or trial, the cost of expert witnesses—such as animal behaviorists or medical experts—can add thousands more to the bill. For an uninsured or underinsured individual, these legal defense costs alone can deplete an emergency fund or require the liquidation of short-term investments.

The Role of Insurance in Asset Protection

For most pet owners, homeowners or renters insurance is the primary line of defense against the costs of a dog bite. However, relying on insurance requires a deep understanding of policy language, as many owners find themselves exposed due to fine-print exclusions.

Understanding Coverage Limits and Exclusions

A standard homeowners insurance policy typically provides between $100,000 and $300,000 in liability coverage. While this sounds substantial, it can be quickly exhausted by a significant injury claim. Furthermore, many insurance carriers have moved toward “breed exclusions.” If your dog is a breed deemed high-risk—such as a Pit Bull, Rottweiler, or German Shepherd—your policy may explicitly exclude coverage for any incidents involving that animal.

If you have failed to disclose the dog to your insurer, or if the dog has a prior history of aggression that was not reported, the company may deny the claim entirely. This leaves the owner personally responsible for the entire judgment, putting their home, savings, and future earnings at risk.

The Impact on Future Premiums and Uninsurability

Even if the insurance company pays the claim, the financial repercussions continue. Following a dog bite claim, an insurance company will almost certainly increase your annual premiums significantly. In many instances, the carrier may choose to non-renew your policy or issue a “canine exclusion” for the future.

Once you have a claim on your record (recorded in databases like the Comprehensive Loss Underwriting Exchange, or CLUE), finding a new insurer becomes difficult and expensive. You may be forced into the “surplus lines” market, where premiums are substantially higher and coverage is more restrictive, creating a long-term drain on your household budget.

Hidden Costs: Settlements, Judgments, and Long-Term Wealth Impact

The true cost of a dog bite is rarely just the medical bill. The legal system allows for “non-economic damages,” which can turn a minor incident into a six-figure financial disaster.

Negotiating Settlements vs. Going to Trial

Most dog bite cases are settled out of court to avoid the unpredictability of a jury. However, settlement amounts are influenced by factors like the victim’s lost wages, scarring (which has a high “dollar value” in personal injury law), and emotional distress. According to the Insurance Information Institute, the average cost per dog bite claim has risen significantly over the last decade, often exceeding $50,000.

If a settlement cannot be reached and the case goes to trial, the financial risk grows exponentially. Juries may award punitive damages if they find the owner was grossly negligent, such as allowing a known aggressive dog to roam off-leash. Punitive damages are rarely covered by insurance, meaning they must be paid directly from the owner’s personal assets.

Impact on Personal Credit and Net Worth

A significant judgment that exceeds insurance limits functions like any other massive debt. If you are unable to pay the judgment, the victim’s legal team may seek to garnish your wages or place a lien on your property. This can destroy your credit score, making it impossible to secure favorable interest rates on mortgages, car loans, or business credit. For those in the middle of their careers, the loss of liquid assets to a lawsuit can set retirement goals back by a decade or more, fundamentally altering their financial trajectory.

Mitigating Financial Risk: Proactive Wealth Protection Strategies

Given the potential for a dog bite to cause a total financial crisis, pet owners must view risk management as a component of their broader financial planning.

Umbrella Insurance Policies

One of the most cost-effective ways to protect your wealth is the purchase of an umbrella insurance policy. An umbrella policy provides excess liability coverage above and beyond the limits of your standard homeowners or auto insurance. For a relatively low annual premium (often $200–$500), you can secure an additional $1 million to $5 million in protection. For a dog owner, this is an essential financial tool; it ensures that even a catastrophic injury or a high-value lawsuit does not result in the loss of your primary residence or retirement accounts.

Investing in Behavioral Training as a Financial Safeguard

From a purely economic perspective, spending money on professional dog training and socialization is an investment with a high Return on Investment (ROI). If you spend $1,500 on a high-quality behavioral modification program, you are effectively spending a small amount to prevent a $50,000+ liability event.

Furthermore, some insurance companies may offer discounts or maintain coverage for “restricted” breeds if the dog has passed the American Kennel Club’s (AKC) Canine Good Citizen (CGC) test. Documenting your efforts to be a responsible owner creates a “paper trail” of due diligence. While this does not absolve you of strict liability, it can be a powerful tool for your defense attorney when negotiating a settlement or arguing against punitive damages, potentially saving you tens of thousands of dollars in the process.

Strategic Asset Titling

For individuals with high net worth, how assets are titled can provide a layer of protection against judgments. Utilizing tools such as Domestic Asset Protection Trusts (DAPTs) or holding certain assets in Tenancy by the Entirety (in states where available) can make it more difficult for a judgment creditor to seize property following a lawsuit. While this does not stop the lawsuit, it protects your core wealth from being completely liquidated to satisfy a dog bite claim.

Conclusion

A dog bite is a traumatic event for all parties involved, but its status as a financial catastrophe is often overlooked until it is too late. From the immediate costs of medical care and legal counsel to the long-term impact on insurance eligibility and net worth, the economic stakes are incredibly high.

By treating pet ownership as a quantifiable financial risk, owners can take the necessary steps—such as securing umbrella insurance, understanding their policy exclusions, and investing in preventative training—to ensure that a single unfortunate moment doesn’t lead to a lifetime of financial hardship. Proper financial planning isn’t just about growing your wealth; it’s about defending it from the unpredictable liabilities of daily life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.