Understanding your withholding allowance is a crucial step in mastering your personal finances and ensuring you’re not over or underpaying taxes throughout the year. While it might sound like a technical tax term, its impact is very real, directly affecting the amount of money that hits your paycheck each pay period. In essence, your withholding allowance, often referred to as a withholding exemption, is a number that dictates how much federal, state, and local income tax your employer should deduct from your wages. The higher your withholding allowance, the less tax will be withheld; conversely, a lower allowance means more tax will be taken out. This seemingly simple adjustment can significantly impact your cash flow, your tax refund, or even the tax bill you face when filing your annual return.

The complexity arises from the fact that your withholding allowance isn’t a static figure. It’s a personalized calculation based on a variety of factors unique to your financial situation, including your marital status, the number of dependents you claim, and other income sources you might have. Incorrectly estimating your allowance can lead to unwelcome surprises – either a large refund that signifies you’ve lent money to the government interest-free for a year, or a hefty tax bill that strains your budget. This article will delve into the intricacies of withholding allowances, demystify the process of determining the correct amount for your situation, and provide actionable insights to help you optimize your tax withholding for financial well-being.

The Foundation: Understanding the W-4 Form and Its Role

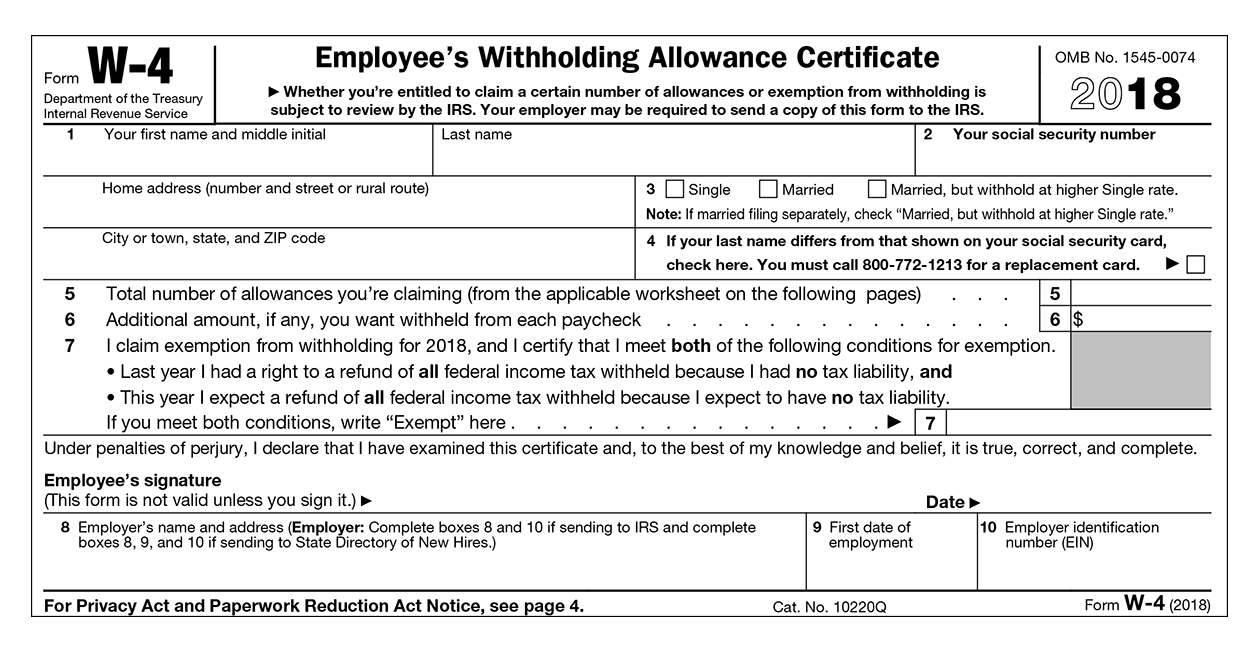

The primary mechanism through which withholding allowances are communicated to your employer is the IRS Form W-4, Employee’s Withholding Certificate. This document is the cornerstone of accurate tax withholding, and accurately completing it is paramount. It serves as the direct link between your personal tax situation and your employer’s payroll system, instructing them on the appropriate tax amounts to remit to the government on your behalf.

Decoding the Purpose of Form W-4

Form W-4 is more than just a piece of paper; it’s a crucial tax document that allows you to tell your employer how much federal income tax you want them to withhold from each of your paychecks. The IRS uses the information you provide on the W-4 to estimate your total tax liability for the year. Based on this estimate, your employer then calculates and withholds the appropriate amount of tax. Without this form, or if it’s filled out incorrectly, your employer would be forced to withhold taxes based on default settings, which are often higher than necessary, leading to over-withholding and a larger refund. Conversely, if you significantly underestimate your tax liability, you might face penalties for underpayment. The W-4 is designed to align your tax payments with your actual tax obligation as closely as possible throughout the year.

Key Sections and Their Significance

The W-4 form has undergone significant revisions in recent years to simplify the process and make it more accurate. While the specific layout might change, the core information required remains consistent. Understanding the purpose of each section is vital for making informed decisions.

Personal Allowances Worksheet

This is arguably the most critical section for determining your withholding allowance. The Personal Allowances Worksheet guides you through a series of questions designed to calculate the number of withholding allowances you can claim. These questions typically revolve around:

- Marital Status: Whether you are single, married filing jointly, married filing separately, or head of household. Your marital status directly impacts the tax brackets and standard deduction amounts you qualify for.

- Dependents: The number of qualifying children and other dependents you have. Each dependent generally allows you to claim an additional withholding allowance, reducing the amount of tax withheld.

- Other Income: If you have income from sources other than your primary job (e.g., a spouse’s income, freelance work, interest, or dividends), this needs to be accounted for. Failing to do so can lead to under-withholding.

- Deductions: If you plan to claim deductions beyond the standard deduction (e.g., mortgage interest, state and local taxes exceeding the limit, charitable contributions), you can adjust your withholding to reflect these potential deductions.

- Extra Withholding: This section allows you to request that your employer withhold an additional amount of tax each pay period, useful for those who anticipate a larger tax bill or prefer to err on the side of over-withholding.

Step 1: Personal Information

This section requires you to provide your basic personal details, including your name, Social Security number, and your filing status. Your filing status is a fundamental determinant of your tax liability and directly influences how many allowances you can claim.

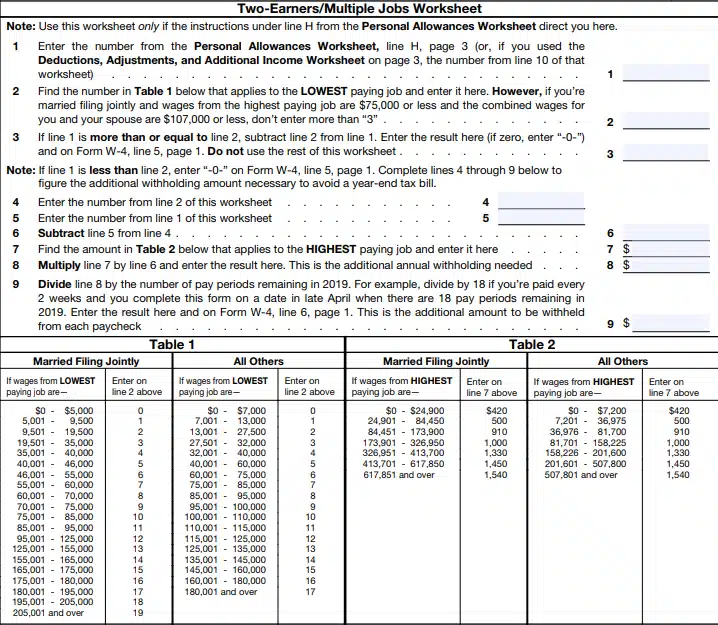

Step 2: Multiple Jobs or Spouse Works

This step is crucial if you or your spouse hold more than one job, or if your spouse also works. The withholding system is designed around a single income source. When there are multiple income streams, the tax brackets can be compressed, leading to higher taxes being withheld if not properly adjusted. This section provides methods to accurately account for combined income, either by using the IRS Tax Withholding Estimator or by using the worksheet provided on the W-4 to account for the higher-earning job.

Step 3: Claim Dependents

This section is where you claim the withholding allowances associated with your dependents. You’ll need to know the total amount of credits you expect to claim for your dependents. The IRS provides specific dollar amounts for these credits, which translate into withholding allowances.

Step 4: Other Adjustments

This section allows for further fine-tuning of your withholding.

- Other Income: Here, you can account for income from sources other than your main job.

- Deductions: If you anticipate itemizing deductions or claiming certain tax credits beyond dependents, you can use this section to reduce your withholding.

- Extra Withholding: As mentioned earlier, this is where you can request an additional dollar amount to be withheld from each paycheck.

Calculating Your Withholding Allowance: Practical Steps and Tools

Determining the correct withholding allowance is not a one-size-fits-all endeavor. It requires a personalized approach that considers your unique financial circumstances. Fortunately, the IRS and various financial tools offer guidance and assistance to make this process as accurate as possible.

The Manual Calculation Method (Using Worksheets)

While the W-4 form itself provides worksheets, using them effectively requires careful attention to detail. The Personal Allowances Worksheet guides you through a step-by-step process. For example, you might start with a base number of allowances and then add or subtract based on specific situations.

- Base Allowance: You generally start with one allowance for yourself. If married, your spouse might also claim one.

- Dependent Allowances: For each qualifying dependent (child or other), you’ll add a specific number of allowances, as defined by IRS guidelines.

- Adjustments for Other Income: If your spouse works, or you have significant other income, you might need to reduce your allowances to ensure sufficient tax is withheld. The worksheet provides formulas for this.

- Adjustments for Deductions and Credits: If you plan to itemize deductions or claim tax credits beyond dependents, you can add allowances to reduce withholding. The worksheet will guide you on how to translate these into allowance adjustments.

It’s crucial to remember that the worksheets are designed as estimates. The IRS strongly encourages taxpayers to use their online tools for a more precise calculation.

Leveraging the IRS Tax Withholding Estimator

The IRS Tax Withholding Estimator is a powerful, free online tool that provides a more dynamic and accurate way to determine your withholding allowance. This tool allows you to input detailed information about your income, tax credits, deductions, and other financial factors.

- Inputting Your Information: You’ll need access to your most recent pay stubs, your spouse’s pay stubs (if applicable), and a copy of your most recent tax return. The estimator will ask about your filing status, the number of jobs you and your spouse have, the number of dependents, income from other sources, expected deductions, and tax credits.

- Real-Time Adjustments: As you input information, the estimator provides real-time feedback on your projected tax liability and the amount of tax being withheld. It can then suggest specific adjustments to your W-4, such as the number of allowances, additional withholding amounts, or adjustments to deductions.

- Simulating Scenarios: The estimator is also useful for simulating different scenarios. For instance, you can see how a change in your marital status, an increase in income, or the addition of a dependent might affect your withholding.

Using the IRS Tax Withholding Estimator is highly recommended for most taxpayers, especially those with multiple income sources, significant life changes, or complex tax situations. It offers a more robust and personalized approach than relying solely on the paper worksheets.

The Importance of Regular Review and Adjustments

Your tax situation is not static. Life events, changes in income, or shifts in your financial planning can all impact your withholding needs. Therefore, it’s essential to review and adjust your withholding allowance regularly.

- Life Events: Major life changes such as marriage, divorce, the birth or adoption of a child, or a change in employment status (e.g., taking on a second job, becoming self-employed, or experiencing a layoff) necessitate a review of your W-4.

- Changes in Income: If your income increases or decreases significantly, or if your spouse’s income changes, your withholding will need to be adjusted to reflect these shifts and avoid under- or over-withholding.

- Tax Law Changes: While less frequent, changes in tax laws can also impact your tax liability and may require an adjustment to your withholding.

- Annual Review: Even without significant life events, it’s a good practice to review your W-4 at least once a year, ideally in conjunction with tax preparation. This ensures your withholding remains aligned with your current financial circumstances.

Failing to update your W-4 after a life event or significant income change can lead to unexpected tax bills or a diminished tax refund. By proactively managing your withholding, you can maintain better control over your finances and avoid unpleasant tax surprises.

The Consequences of Incorrect Withholding: Refund vs. Tax Bill

The number you choose for your withholding allowance has a direct and significant impact on your financial outcome at tax time. It dictates whether you’ll receive a substantial tax refund, face an unexpected tax bill, or be close to breaking even. Understanding these potential outcomes can help you make more informed decisions when completing your W-4.

The Over-Withholding Scenario: A Larger Tax Refund

When you claim too many withholding allowances, or if your actual tax liability for the year is less than what has been withheld, you will likely receive a tax refund. This means that throughout the year, your employer has been deducting more income tax from your paychecks than you actually owe.

- The “Interest-Free Loan” Effect: While a large refund might feel like a bonus, it essentially means you’ve been lending money to the government interest-free for an entire year. This money could have been used for other financial goals, such as paying down debt, investing, or building an emergency fund.

- Psychological Impact: Some individuals prefer a larger refund as a form of forced savings. However, financially speaking, it’s generally more advantageous to have that money available to you throughout the year for immediate use.

- Potential for Underpayment Penalties: While over-withholding leads to a refund, under-withholding can lead to penalties. If you consistently owe a significant amount when you file your taxes, the IRS may charge you penalties and interest for not paying enough tax throughout the year.

The Under-Withholding Scenario: An Unexpected Tax Bill

Conversely, if you claim too few withholding allowances, or if your actual tax liability for the year is greater than what has been withheld, you will owe money when you file your tax return. This situation can be financially stressful, especially if the tax bill is substantial.

- Budgetary Strain: An unexpected tax bill can disrupt your budget, potentially forcing you to dip into savings, take on debt, or cut back on essential expenses.

- IRS Penalties and Interest: The IRS imposes penalties for underpayment of taxes. These penalties are typically calculated as a percentage of the underpaid amount and can significantly increase the total amount you owe. Interest is also charged on the underpaid amount until it’s fully paid.

- Factors Leading to Under-Withholding: Common reasons for under-withholding include not accounting for multiple jobs, underestimating income from side hustles or investments, failing to adjust withholding after a life event, or not claiming all eligible dependents and tax credits.

Striving for Tax Neutrality: The Ideal Outcome

The goal for many taxpayers is to achieve tax neutrality, meaning the amount of tax withheld throughout the year closely matches their actual tax liability. This results in owing very little or receiving a small refund when filing their annual tax return.

- Maximizing Cash Flow: By withholding the correct amount, you ensure you have access to your full income throughout the year, allowing for better financial planning and management.

- Avoiding Penalties and Missed Opportunities: Tax neutrality prevents underpayment penalties and avoids the opportunity cost of lending money to the government interest-free.

- Achieving Through Accurate W-4 Completion: Accurate completion of Form W-4, particularly with the assistance of the IRS Tax Withholding Estimator, is the most effective way to achieve tax neutrality. Regularly reviewing and updating your W-4 after significant life events is also crucial.

Beyond the W-4: Other Financial Considerations Related to Withholding

While the W-4 form is the primary tool for managing income tax withholding, understanding its implications can lead to broader financial planning considerations. Effectively managing your withholding allowance is a key component of sound personal finance management.

The Role of Withholding in Your Overall Financial Plan

Your withholding allowance is intrinsically linked to your overall financial strategy. How much tax is withheld directly impacts your disposable income, which in turn affects your ability to save, invest, and manage debt.

- Budgeting and Cash Flow: The amount of net pay you receive each payday is a direct result of your withholding. Adjusting your W-4 can free up more cash flow for daily expenses, debt repayment, or unexpected emergencies. Conversely, higher withholding can create a more predictable savings outcome if you prefer a larger refund.

- Emergency Fund: Having a robust emergency fund is critical. If you consistently over-withhold and receive a large refund, you might be foregoing the opportunity to build this fund more rapidly. If you under-withhold and face a tax bill, a lack of an emergency fund can exacerbate the financial strain.

- Debt Management: The extra money you have access to from optimized withholding can be strategically used to pay down high-interest debt, saving you money on interest payments over time.

- Investment Goals: Similarly, increased disposable income can be directed towards investments, helping you grow your wealth over the long term.

Self-Employment and Estimated Taxes

For individuals who are self-employed, the concept of withholding allowance takes on a different form. Instead of an employer withholding taxes, self-employed individuals are responsible for calculating and paying their own taxes through a system of estimated tax payments.

- No Employer Withholding: Unlike employees, self-employed individuals do not have an employer to automatically withhold income tax and FICA taxes (Social Security and Medicare) from their earnings.

- Quarterly Payments: Self-employed individuals are generally required to make estimated tax payments to the IRS quarterly. These payments are an estimate of the taxes you expect to owe for the year, including income tax and self-employment tax.

- Calculating Estimated Taxes: The calculation for estimated taxes involves projecting your annual income and expenses, determining your expected tax liability, and then dividing that liability into four equal quarterly payments. Tools and worksheets provided by the IRS can assist with this calculation.

- Penalties for Underpayment: Similar to employees who under-withhold, self-employed individuals can face penalties if they underpay their estimated taxes throughout the year.

Understanding the differences between employee withholding and self-employment estimated taxes is crucial for individuals in both categories to avoid tax surprises and penalties.

The Broader Impact on Financial Health

Mastering your withholding allowance is more than just a tax compliance issue; it’s a fundamental aspect of responsible financial management. By taking the time to understand and accurately set your withholding, you gain greater control over your finances, enabling you to achieve your financial goals more effectively. It empowers you to make informed decisions about your money, reduce financial stress, and build a more secure financial future. Regularly reviewing and adjusting your withholding is a simple yet powerful habit that pays significant dividends throughout your financial journey.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.