In the complex landscape of personal finance, few areas are as opaque and potentially costly as healthcare. For many individuals and families, the terminology found within an insurance policy—deductibles, premiums, coinsurance, and out-of-pocket maximums—can feel like a foreign language. Among these terms, “copay” is perhaps the one people encounter most frequently in their day-to-day lives. Whether you are picking up a prescription or visiting a specialist, the copay is often your first point of financial contact with the medical system.

Understanding what a copay means, how it functions within a broader financial strategy, and how it differs from other cost-sharing mechanisms is essential for maintaining a healthy budget. In this guide, we will break down the mechanics of copayments and provide professional insights into how you can manage these costs effectively within your financial plan.

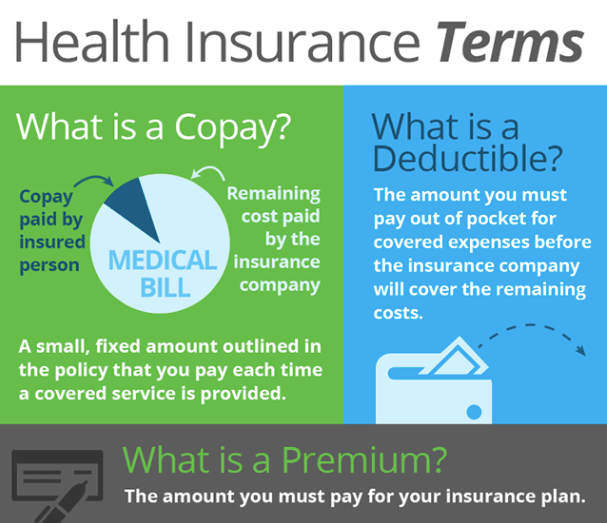

Understanding the Fundamentals: What is a Copayment?

At its most basic level, a copayment (or “copay”) is a fixed out-of-pocket amount that an insured person pays for a covered healthcare service after they have paid their premium. Unlike other forms of medical billing, a copay is a predetermined dollar amount, not a percentage of the total bill.

Defining the Copay in Your Insurance Policy

When you sign up for a health insurance plan, your summary of benefits will list specific dollar amounts for various services. For example, you might see a $20 copay for a primary care visit, a $50 copay for a specialist, and a $15 copay for generic drugs. This amount is usually due at the time of service—meaning you pay it at the front desk of the doctor’s office or the pharmacy counter.

It is important to note that copays do not typically count toward your annual deductible, though they almost always count toward your out-of-pocket maximum. From a personal finance perspective, copays represent a “pay-as-you-go” cost that provides predictability in your monthly cash flow. You know exactly what a routine visit will cost before you even step through the door.

How Copays Differ from Deductibles and Coinsurance

To master your healthcare budget, you must distinguish copays from two other critical terms: deductibles and coinsurance.

- Deductibles: This is the total amount you must pay out-of-pocket for covered services before your insurance company begins to pay. If your deductible is $2,000, you are responsible for the first $2,000 of your medical bills (excluding many preventive services).

- Coinsurance: Once you have met your deductible, you enter the coinsurance phase. Instead of a fixed dollar amount (copay), you pay a percentage of the costs—usually 20%—while the insurer pays the remaining 80%.

The primary advantage of a copay-heavy plan is financial certainty. While coinsurance can lead to high bills for expensive procedures, a copay remains static regardless of whether the doctor spends ten minutes or an hour with you.

The Financial Mechanics of Copays: Why They Exist and How They Are Set

From the perspective of an insurance provider and the broader economy, copays serve a dual purpose: they offset administrative costs and act as a “gatekeeper” to prevent the over-utilization of medical services. If healthcare were entirely free at the point of service, there would be less incentive for consumers to consider the necessity of every minor visit.

Tiered Copay Systems for Prescription Drugs

One of the most common places you will see copays is at the pharmacy. Most insurance companies use a “formulary,” which is a list of covered drugs organized into tiers. Each tier carries a different copay.

- Tier 1: Typically generic drugs with the lowest copay (e.g., $5–$15).

- Tier 2: Preferred brand-name drugs with a moderate copay (e.g., $30–$50).

- Tier 3: Non-preferred or specialty drugs with the highest copay (e.g., $100+).

For those managing chronic conditions, understanding these tiers is vital for long-term financial planning. Switching from a Tier 2 brand-name medication to a Tier 1 generic can save a household hundreds of dollars annually in copayments alone.

Specialist vs. Primary Care: The Variation in Costs

Insurance companies structure copays to encourage cost-efficient behavior. This is why a visit to a primary care physician (PCP) almost always has a lower copay than a visit to a specialist. By making the PCP visit more affordable, insurers nudge patients to seek care from generalists first, who can then determine if expensive specialist intervention is actually required.

Furthermore, emergency room (ER) copays are designed to be significantly higher—often $250 or more—to discourage people from using the ER for non-life-threatening issues that could be handled at an urgent care center (which typically carries a much lower copay).

Strategic Financial Planning: Managing Your Healthcare Budget

Knowing what a copay is is only the first step; the second is integrating that knowledge into your wealth management strategy. Healthcare costs are one of the leading causes of financial stress, but they can be mitigated with proactive planning.

The Impact of Copays on Annual Out-of-Pocket Maximums

In the United States, the Affordable Care Act (ACA) mandates an “out-of-pocket maximum.” This is the most you will have to pay for covered services in a plan year. Once you reach this limit, your insurance pays 100% of your healthcare costs.

When calculating your “worst-case scenario” for the year, you must factor in your copays. If you have a high-utilization year—perhaps involving physical therapy or frequent specialist visits—those $40 and $50 copays add up quickly. A professional financial plan should include an emergency fund that covers at least your annual out-of-pocket maximum to ensure a medical crisis doesn’t become a financial one.

Utilizing HSAs and FSAs to Cover Copay Expenses

One of the smartest ways to handle copays is by using tax-advantaged accounts like Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs).

- HSAs: Available to those with high-deductible health plans (HDHPs). The money you contribute is tax-deductible, grows tax-free, and stays with you forever. Using an HSA to pay for copays effectively gives you a 20–30% discount on your medical costs (depending on your tax bracket) because you are using pre-tax dollars.

- FSAs: Usually offered through employers. These are “use it or lose it” accounts within a calendar year, but they offer similar tax benefits for paying copays.

By automating contributions to these accounts, you ensure that the cash for your next copay is already set aside, reducing the friction of paying at the doctor’s office.

The Role of Copays in Employer-Sponsored Benefit Strategies

If you are a business owner or an HR professional, the way you structure copays within your company’s health plan is a critical component of your corporate financial strategy. Benefits are a major overhead cost, but they are also a primary tool for talent acquisition and retention.

Balancing Premiums and Copays for Business Efficiency

There is an inverse relationship between premiums (the monthly cost of the insurance) and copays. Plans with “low copays” generally have “high premiums.” For a business, offering a “Platinum” plan with $10 copays can be an excellent perk for employees, but it significantly increases the company’s fixed monthly costs.

Conversely, many modern businesses are moving toward High Deductible Health Plans (HDHPs) where copays are often non-existent until the deductible is met. While this lowers the company’s premium burden, it can lead to financial strain for employees if not paired with employer contributions to an HSA. Finding the “sweet spot” requires analyzing the demographics and health needs of the workforce.

How Copay Structures Influence Employee Retention

In a competitive job market, “total compensation” includes the quality of healthcare. An employee might choose a job with a slightly lower salary if the health plan features low copays and a broad network of doctors. For employees with families, a $20 difference in a pediatric copay can mean a difference of hundreds of dollars a year. Therefore, a well-designed copay structure is not just a line item in a budget; it is a strategic investment in the stability and satisfaction of the workforce.

Conclusion: Copays as a Tool for Financial Literacy

In the realm of personal and business finance, “what does copay mean” is a question that leads to a much deeper conversation about risk management and resource allocation. A copay is more than just a fee paid at a counter; it is a mechanism that provides predictability in an unpredictable world.

By understanding how copays interact with deductibles, leveraging tax-advantaged accounts like HSAs, and choosing insurance plans that align with your health usage patterns, you can take control of your financial destiny. Whether you are an individual looking to optimize your monthly budget or a business leader looking to provide value to your team, mastering the nuances of copayments is an essential step toward long-term fiscal health. In the end, the goal of understanding these terms is simple: to ensure that healthcare remains a path to wellness, rather than a hurdle to financial security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.