Navigating the annual ritual of filing taxes can often feel like deciphering a complex puzzle. With varying income streams, deductions, and credits, the sheer volume of paperwork can be daunting. However, understanding precisely which documents you need is the first and most crucial step towards a smooth, accurate, and stress-free tax season. This comprehensive guide will demystify the process, ensuring you gather all necessary information to meet your obligations and potentially maximize your refunds or minimize your liabilities.

The Foundation: Personal Information and Basic Identifiers

Before delving into income and expenses, every tax return begins with fundamental personal and identification details. These elements form the bedrock of your tax filing.

Your Identity and Contact Details

Your tax return requires accurate personal information for yourself, your spouse (if filing jointly), and any dependents. This includes full legal names, current addresses, dates of birth, and relationship to the taxpayer. Ensuring this information is up-to-date is critical for correct processing and any correspondence from tax authorities. A change of address, for instance, should always be reflected on your tax forms.

Social Security Numbers for All

The Social Security Number (SSN) is paramount. You will need your SSN, your spouse’s SSN, and the SSNs of all dependents you claim. The SSN is the primary identifier for the IRS and other tax authorities, linking all your income, credits, and deductions to your specific record. Accuracy here is non-negotiable; even a single digit error can lead to significant delays or rejections of your return. If any family member lacks an SSN, an Individual Taxpayer Identification Number (ITIN) or Adoption Taxpayer Identification Number (ATIN) may be required.

Bank Account Information for Refunds/Payments

While not a document in the traditional sense, having your bank account’s routing and account numbers readily available is essential if you wish to receive your refund via direct deposit or pay any taxes owed electronically. Direct deposit is often the fastest and most secure way to receive your refund, avoiding potential delays or lost checks. Similarly, electronic payments ensure timely remittance, helping you avoid late payment penalties.

Income Documentation: Tracking Your Earnings

The core of any tax return is reporting your income. The type of income you earn dictates the specific forms you will receive and need to include. Gathering these documents meticulously is crucial for an accurate representation of your taxable earnings.

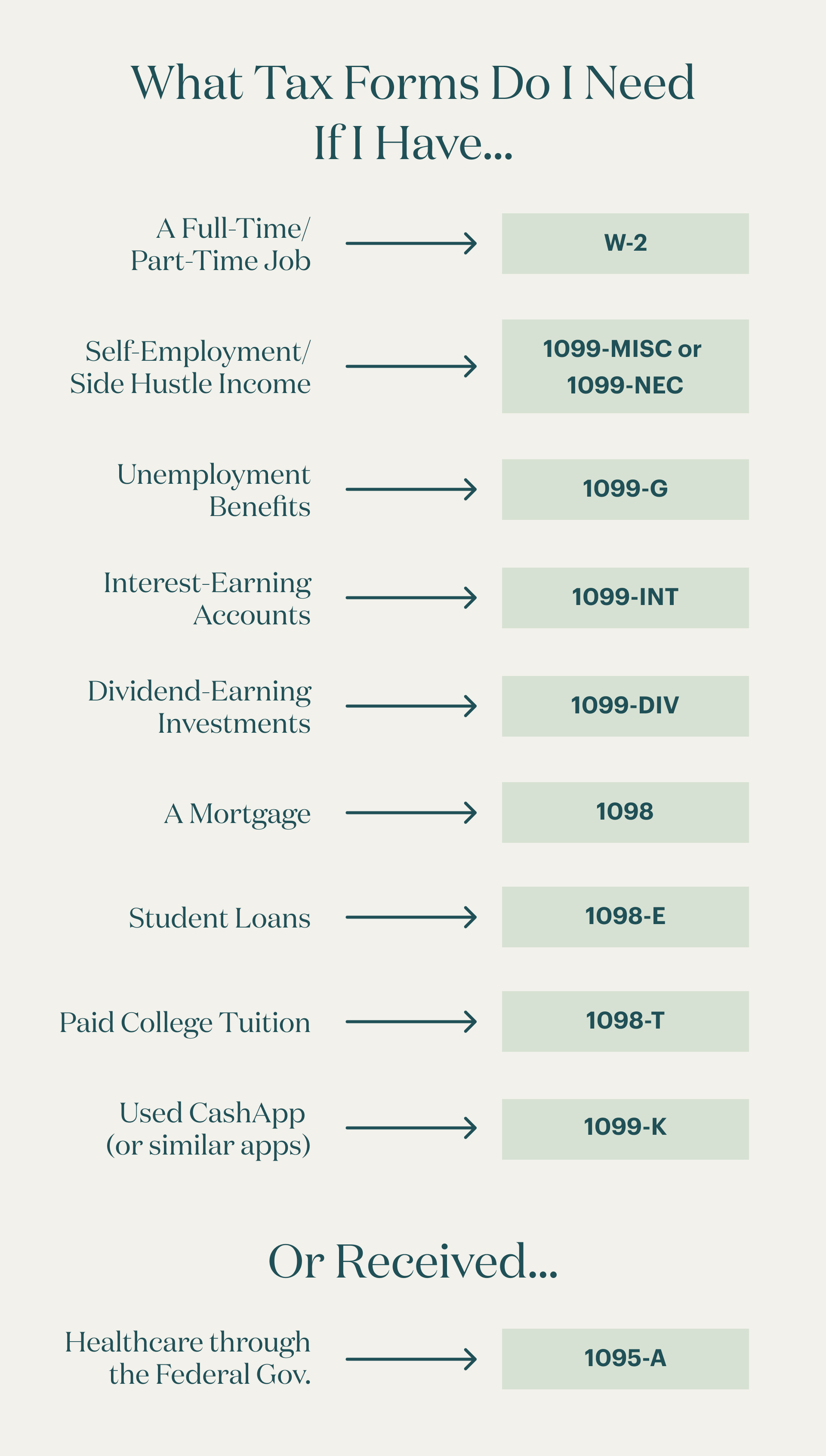

Wage Earners: W-2 Forms

For employees, the Form W-2, Wage and Tax Statement, is perhaps the most familiar document. Your employer is legally required to send this form to you by January 31st each year. It details your gross wages, tips, and other compensation, along with the federal, state, and local income taxes withheld, Social Security taxes, and Medicare taxes. If you worked for multiple employers during the year, you’ll need a W-2 from each one. Don’t forget any W-2s from temporary or seasonal jobs.

Independent Contractors & Gig Workers: 1099 Forms

If you’re self-employed, an independent contractor, or participate in the burgeoning gig economy, you’ll primarily deal with various 1099 forms.

- Form 1099-NEC (Nonemployee Compensation): This replaced Form 1099-MISC for reporting payments of $600 or more for services performed for a trade or business by someone who is not an employee. Freelancers, consultants, and contractors will receive this form.

- Form 1099-MISC (Miscellaneous Information): While no longer used for nonemployee compensation, this form still reports other types of income such as rents, royalties, prizes and awards, or medical and healthcare payments.

- Form 1099-K (Payment Card and Third-Party Network Transactions): If you received payments through third-party payment networks (e.g., PayPal, Venmo, Stripe for business transactions) or credit/debit card transactions, you might receive a 1099-K. This is particularly relevant for online sellers, small business owners, and those in the gig economy.

Investment Income: 1099-B, DIV, INT, R

If you have investments, several 1099 forms report various types of investment income:

- Form 1099-B (Proceeds From Broker and Barter Exchange Transactions): Reports gains or losses from stock sales, mutual funds, and other securities.

- Form 1099-DIV (Dividends and Distributions): Details dividends received from stocks or mutual funds.

- Form 1099-INT (Interest Income): Reports interest earned from bank accounts, savings bonds, or other investments.

- Form 1099-R (Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc.): Essential for retirees or those who took distributions from retirement accounts.

Other Income Sources

Don’t overlook other potential income sources that are taxable:

- Unemployment Compensation (Form 1099-G): Payments received from unemployment insurance are taxable income.

- Social Security Benefits (Form SSA-1099): A portion of your Social Security benefits may be taxable depending on your overall income level.

- Rental Income and Royalties: Records of income and expenses from rental properties or royalty payments.

- Gambling Winnings (Form W-2G): If you won significant amounts from lotteries, horse races, or casinos, you’ll receive this form.

Deduction and Credit Documentation: Reducing Your Taxable Income

Beyond income, many taxpayers can reduce their taxable income or directly lower their tax bill through deductions and credits. These require careful documentation to substantiate your claims.

Itemized Deductions vs. Standard Deduction

Most taxpayers choose between taking the standard deduction (a fixed amount based on filing status) or itemizing their deductions. If your itemized deductions exceed the standard deduction, it’s typically more advantageous to itemize.

- Medical and Dental Expenses: Receipts for unreimbursed medical expenses exceeding a certain percentage of your Adjusted Gross Income (AGI).

- State and Local Taxes (SALT): Records of property taxes paid, state income taxes, or sales taxes. Note the current $10,000 limitation for state and local taxes.

- Mortgage Interest (Form 1098): Your mortgage lender will send you Form 1098, reporting the interest paid on your home loan.

- Charitable Contributions: Receipts or acknowledgment letters from qualified charities for cash or non-cash donations. For contributions over $250, written acknowledgment from the charity is mandatory.

Common Credits

Tax credits directly reduce your tax liability dollar-for-dollar and are generally more beneficial than deductions.

- Child Tax Credit and Credit for Other Dependents: Requires SSNs for qualifying children and other dependents.

- Child and Dependent Care Credit (Form 2441): Records of expenses paid for childcare while you worked or looked for work, along with the care provider’s name, address, and SSN/EIN.

- Education Credits (Forms 1098-T): Tuition statements from educational institutions for yourself or your dependents.

- Residential Energy Credits: Receipts for qualifying energy-efficient home improvements.

- Earned Income Tax Credit (EITC): No specific form, but relies on your income and number of qualifying children.

Retirement Contributions

Documents related to contributions to retirement accounts can also impact your taxes:

- IRA Contributions: Records of contributions made to a traditional or Roth IRA.

- 401(k) Contributions: These are typically reflected on your W-2.

Health Savings Accounts (HSAs)

If you have a High-Deductible Health Plan (HDHP) and contribute to an HSA, you’ll need:

- Form 1099-SA: Reports distributions from an HSA, Archer MSA, or Medicare Advantage MSA.

- Form 5498-SA: Reports contributions to an HSA, Archer MSA, or Medicare Advantage MSA.

Special Circumstances and Business-Related Documents

Beyond the common scenarios, certain life events or business ventures require additional documentation.

Self-Employment Expenses

For self-employed individuals, meticulous record-keeping of business expenses is vital to accurately calculate net earnings and potential deductions. This includes:

- Business mileage logs: For vehicle expenses.

- Receipts for office supplies, software, utilities, and other operating costs.

- Home office expenses: Records for a dedicated home office.

- Business travel and meal receipts.

- Professional development and training costs.

Homeownership

If you own a home, several documents become relevant:

- Real Estate Tax Statements: Proof of property taxes paid.

- Mortgage Interest Statement (Form 1098): As mentioned earlier, for mortgage interest.

- Records of any home energy improvements that might qualify for credits.

Foreign Income and Assets

If you have income from foreign sources or hold foreign bank accounts, you might need additional forms:

- Form 2555 (Foreign Earned Income): To claim the foreign earned income exclusion.

- FinCEN Form 114 (FBAR): Report of Foreign Bank and Financial Accounts, for aggregate foreign account balances exceeding $10,000.

Previous Year’s Tax Return

While not always strictly necessary for current-year filing, having a copy of your previous year’s tax return is often highly beneficial. It provides:

- Your prior year’s Adjusted Gross Income (AGI), which might be needed for identity verification when e-filing.

- Information on any carryovers (e.g., capital loss carryovers, net operating losses).

- A useful reference for recurring deductions or income sources.

Organizing and Preparing for a Smooth Filing Process

Gathering the documents is only half the battle; proper organization and preparation are key to a stress-free experience.

Digital vs. Physical Organization

Decide on a system for organizing your documents. Whether you prefer a physical filing cabinet with clearly labeled folders or a digital system using scans and cloud storage, consistency is paramount. For digital records, consider encrypting sensitive files and backing them up securely. Many online tax software providers allow you to upload documents directly, streamlining the process.

The Importance of Record Keeping

The IRS generally recommends keeping tax records for at least three years from the date you filed your original return or two years from the date you paid the tax, whichever is later. For certain items, such as records relating to property or business assets, you may need to keep them for much longer. Good record-keeping throughout the year significantly simplifies tax preparation and provides crucial evidence if you ever face an audit.

Seeking Professional Help

If your financial situation is complex, or you feel overwhelmed by the process, consider consulting a tax professional. An enrolled agent, CPA, or tax attorney can help ensure accuracy, identify all applicable deductions and credits, and navigate intricate tax laws. Even if you use a professional, having all your documents organized beforehand will save time and money.

In conclusion, understanding and gathering the necessary documents is the cornerstone of successful tax filing. By systematically collecting your personal information, income statements, and records for deductions and credits, you can approach tax season with confidence, ensuring compliance and optimizing your financial outcome. Start early, stay organized, and remember that thorough preparation is your best defense against errors and missed opportunities.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.