Tax season is often viewed with a sense of trepidation, yet it remains one of the most critical annual events in an individual’s financial life. Filing taxes is more than just a legal obligation; it is an opportunity to audit your personal finances, reassess your income streams, and potentially secure a significant refund that can be channeled into savings or investments. To navigate this process successfully, organization is paramount. Missing a single form or failing to account for a specific deduction can result in processing delays, missed financial opportunities, or even an audit from the IRS.

This guide serves as a master checklist for the modern taxpayer. Whether you are a traditional employee, a freelancer in the gig economy, or a seasoned investor, understanding exactly what you need to file taxes will streamline your experience and ensure you are maximizing your financial health.

1. Essential Personal Identification and Demographic Data

Before you can dive into the complexities of income and deductions, you must establish the foundational “who” of your tax return. Accuracy in this section is vital, as even a minor typo in a Social Security number can lead to an immediate rejection of an e-filed return.

Social Security Numbers and ITINs

The primary identifier for federal taxes is your Social Security Number (SSN). You will need this for yourself, your spouse (if filing jointly), and every dependent you intend to claim. If you are a non-resident or resident alien who does not have an SSN, you will need your Individual Taxpayer Identification Number (ITIN). For dependents, ensuring you have their correct birth dates and Social Security cards on hand is crucial, as the IRS cross-references this data to prevent identity fraud and ensure eligibility for various tax credits.

Banking Information for Direct Deposit

From a personal finance perspective, the goal of filing is often to receive a refund as quickly as possible. To facilitate this, you need your bank’s routing number and your specific account number. Opting for direct deposit is significantly faster and more secure than waiting for a paper check in the mail. If you plan to split your refund into multiple accounts—such as a checking account for immediate needs and a high-yield savings account or an IRA for long-term growth—you will need the details for each institution.

Last Year’s Tax Return

While not always strictly required for current calculations, having your previous year’s tax return is highly beneficial. It provides a roadmap of your typical filing status, previously claimed deductions, and carryover losses. Furthermore, if you are using tax software for the first time, you may need your Adjusted Gross Income (AGI) from the prior year to verify your identity for the IRS’s e-filing system.

2. Documentation of All Income Sources

In the modern financial landscape, income rarely comes from a single source. Between the “9-to-5” job, freelance side hustles, and investment portfolios, the IRS expects a comprehensive report of every dollar earned.

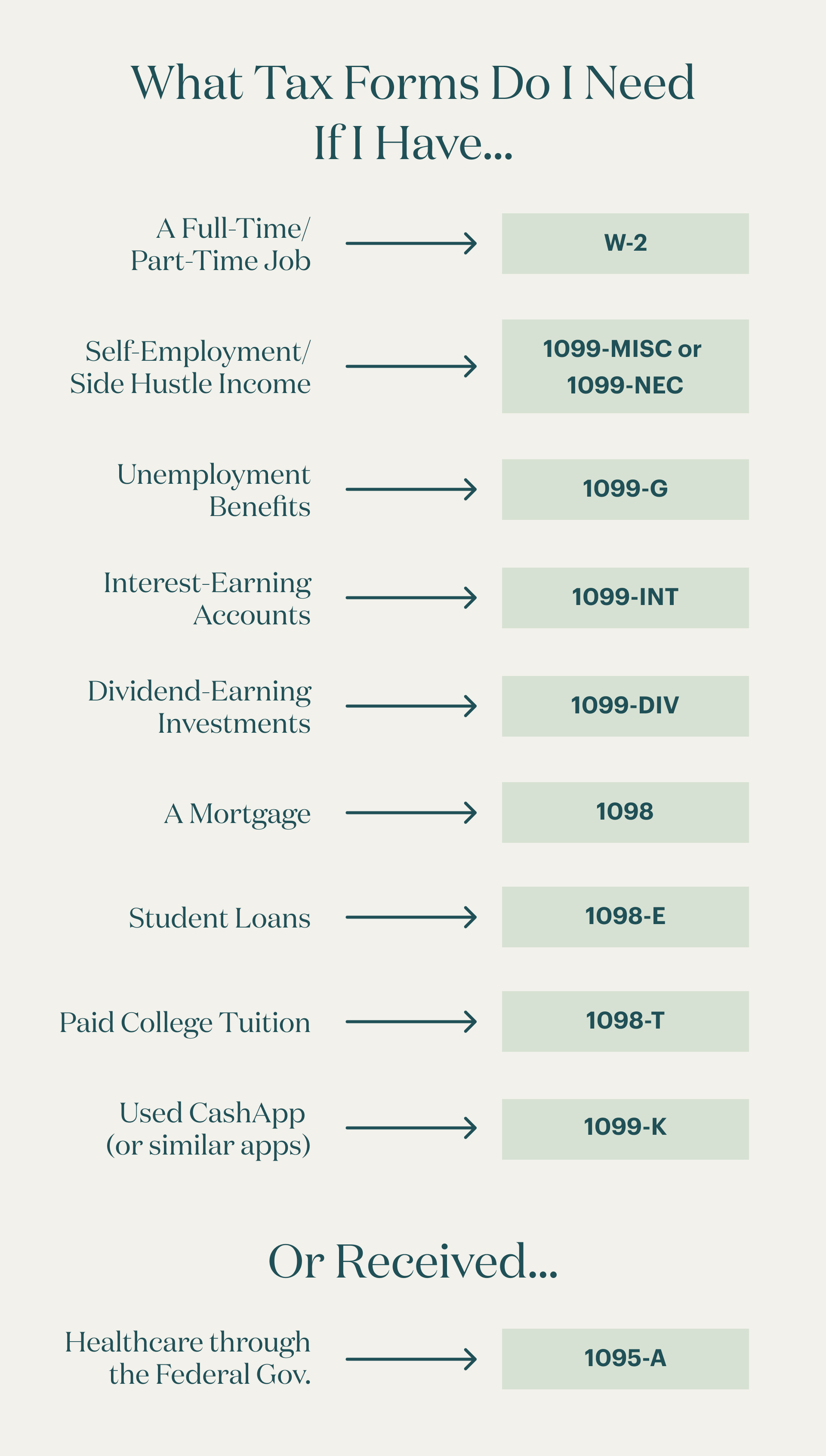

W-2s for Traditional Employment

If you are an employee, your employer is required to provide a Form W-2 by January 31st. This document summarizes your total earnings, as well as the federal, state, and local taxes already withheld. It also details contributions to employer-sponsored retirement plans like 401(k)s and health insurance premiums, which are essential for determining your taxable income.

1099s for Freelancers and the Gig Economy

For those engaged in online income or side hustles, the 1099 series is your primary focus.

- 1099-NEC: This is used for non-employee compensation. If you earned $600 or more from a single client as a contractor, they should issue this form.

- 1099-K: If you receive payments via third-party processors like PayPal, Venmo, or Etsy, you may receive a 1099-K if your transactions meet certain thresholds.

- 1099-MISC: This covers miscellaneous income, such as rent payments or prizes.

As a business finance best practice, you should keep your own ledger of earnings throughout the year to verify that the amounts reported on these forms are accurate.

Investment and Passive Income Documentation

Investing is a pillar of wealth building, but it adds a layer of complexity to tax time. You will need:

- 1099-INT: For interest earned on savings accounts or CDs.

- 1099-DIV: For dividends and distributions from stocks or mutual funds.

- 1099-B: This form reports the proceeds from the sale of stocks, bonds, or cryptocurrencies. Crucially, you must also know your “cost basis”—the original price you paid—to determine your capital gains or losses.

- Schedule K-1: If you are an investor in a partnership, S-corporation, or certain trusts, this form reports your share of the entity’s income.

3. Maximizing Deductions and Tax Credits

The “Money” niche of tax filing focuses heavily on tax efficiency—the art of legally minimizing your tax liability. Deductions reduce the amount of income you are taxed on, while credits provide a dollar-for-dollar reduction in the tax you owe.

Standard vs. Itemized Deductions

The most significant decision you will make is whether to take the standard deduction or to itemize. For the majority of taxpayers, the standard deduction (which the IRS adjusts annually for inflation) provides the largest benefit with the least amount of paperwork. However, if your total deductible expenses—such as mortgage interest, state and local taxes (SALT), and medical expenses—exceed the standard deduction threshold, itemizing is the smarter financial move.

Educational Expenses and Student Loans

Education is an investment in human capital, and the tax code offers incentives for it. You should look for Form 1098-T from your educational institution to claim the American Opportunity Tax Credit (AOTC) or the Lifetime Learning Credit (LLC). Additionally, if you are paying off debt, Form 1098-E reports the student loan interest you’ve paid, which may be deductible even if you don’t itemize.

Healthcare and Charitable Contributions

If you had a High Deductible Health Plan (HDHP) and contributed to a Health Savings Account (HSA), you will need Form 5498-SA and 1099-SA. Contributions to an HSA are triple-tax advantaged and represent a powerful financial tool. Furthermore, if you itemize, you must gather receipts for all charitable contributions. For donations over $250, the IRS requires a written acknowledgment from the charity to substantiate the claim.

4. Business Expenses and Self-Employed Financial Records

For those running a small business or working as a “solopreneur,” the line between personal and business finance can sometimes blur. To file correctly, you need rigorous documentation of your business expenditures to offset your gross income.

The Home Office and Operating Costs

If you use a portion of your home exclusively for business, you may be eligible for the home office deduction. You will need records of your home’s square footage, as well as utility bills, mortgage interest, or rent paid. Beyond the home office, you should compile receipts for advertising, professional software subscriptions, office supplies, and travel expenses directly related to your business operations.

Vehicle Usage and Mileage Logs

If you use your car for business—whether it’s visiting clients or making deliveries—you can deduct these costs. You generally have two choices: the standard mileage rate or the actual expense method. If you choose the mileage rate, you must provide a detailed log showing the date, purpose, and distance of every business trip. If choosing actual expenses, you’ll need receipts for gas, repairs, insurance, and registration.

Retirement Contributions for the Self-Employed

One of the best ways to reduce your taxable income while building future wealth is through self-employed retirement accounts. If you contributed to a SEP-IRA, SIMPLE IRA, or a Solo 401(k), ensure you have the records of these contributions. These are often deductible and represent a critical strategy in long-term financial planning.

5. Utilizing Financial Tools and Maintaining Records

The final step in preparing to file taxes involves selecting the right tools and establishing a system for the future. In the realm of business finance, efficiency is just as important as accuracy.

Choosing Between Software and Professional CPAs

In the modern era, high-quality tax software can handle most standard returns with ease, guiding users through a series of questions to ensure no credits are missed. However, if your financial situation involves complex business structures, multiple rental properties, or significant international assets, hiring a Certified Public Accountant (CPA) is a wise investment. A professional can provide strategic advice that software cannot, potentially saving you thousands in the long run.

The Importance of Record-Keeping and Audit Protection

The filing process doesn’t end once you hit “submit.” The IRS generally has three years to audit a return, though this can be longer in certain circumstances. From a financial security standpoint, you should maintain digital or physical copies of all documents used to prepare your return for at least seven years. Using digital tools like receipt-scanning apps and cloud-based accounting software can make this organization effortless, ensuring that if you are ever asked to substantiate a claim, you have the evidence ready.

In conclusion, filing taxes is a foundational aspect of personal finance management. By gathering your identification, documenting every stream of income, and meticulously tracking your deductions and business expenses, you move from a state of reactive stress to one of proactive financial control. Preparation is the key to ensuring that you pay exactly what you owe and not a penny more, allowing you to keep more of your hard-earned money working for you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.