For many individuals, a home is the most significant financial investment they will ever make. Protecting that investment requires more than just a mortgage and standard homeowners insurance; it requires a strategic approach to risk management. One of the most common financial tools used to mitigate the costs of homeownership is the home warranty. While often misunderstood, a home warranty serves as a service contract that covers the repair or replacement of major home systems and appliances that break down due to normal wear and tear.

From a personal finance perspective, a home warranty acts as a hedge against the volatility of repair costs. Instead of facing a sudden $5,000 bill for a failed HVAC system, a homeowner pays a predictable annual premium and a small service fee. This article explores the specifics of what home warranties cover, the financial logic behind them, and how to evaluate their worth within your broader financial plan.

The Financial Framework of a Home Warranty

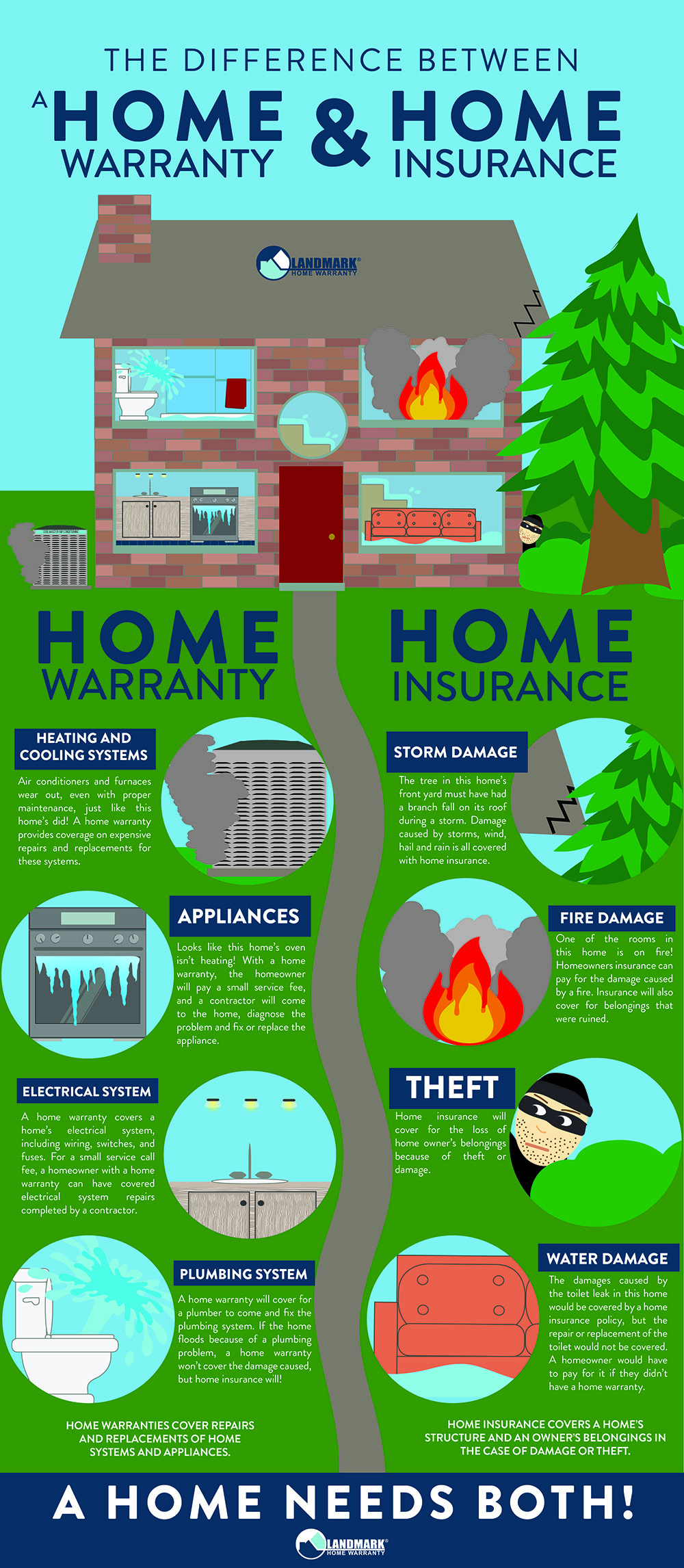

To understand what a home warranty covers, one must first understand its role in a financial portfolio. Unlike homeowners insurance, which protects against “perils” like fire, theft, or catastrophic wind damage, a home warranty is designed for the inevitable: mechanical failure.

Predictable Budgeting vs. Volatile Repair Costs

The primary financial appeal of a home warranty is the conversion of variable, high-impact expenses into fixed, manageable costs. For many households, liquidity is a concern. An unexpected water heater failure or a dishwasher breakdown can disrupt a monthly budget or force a withdrawal from an emergency fund or high-yield savings account. By paying an annual premium—typically ranging from $500 to $900—homeowners transfer the risk of these high-cost repairs to the warranty provider. This allows for more precise long-term financial planning and ensures that “rainy day” funds remain available for true emergencies.

Distinguishing Between Home Insurance and Home Warranties

From a money management standpoint, it is crucial to distinguish these two products to avoid over-insuring or under-protecting your assets. Homeowners insurance is usually required by mortgage lenders and covers the structure and the contents in the event of external damage. A home warranty is optional and covers the internal mechanics. For example, if a lightning strike fries your refrigerator, insurance handles it. If the refrigerator’s compressor simply wears out after eight years, the home warranty is the financial instrument that covers the replacement.

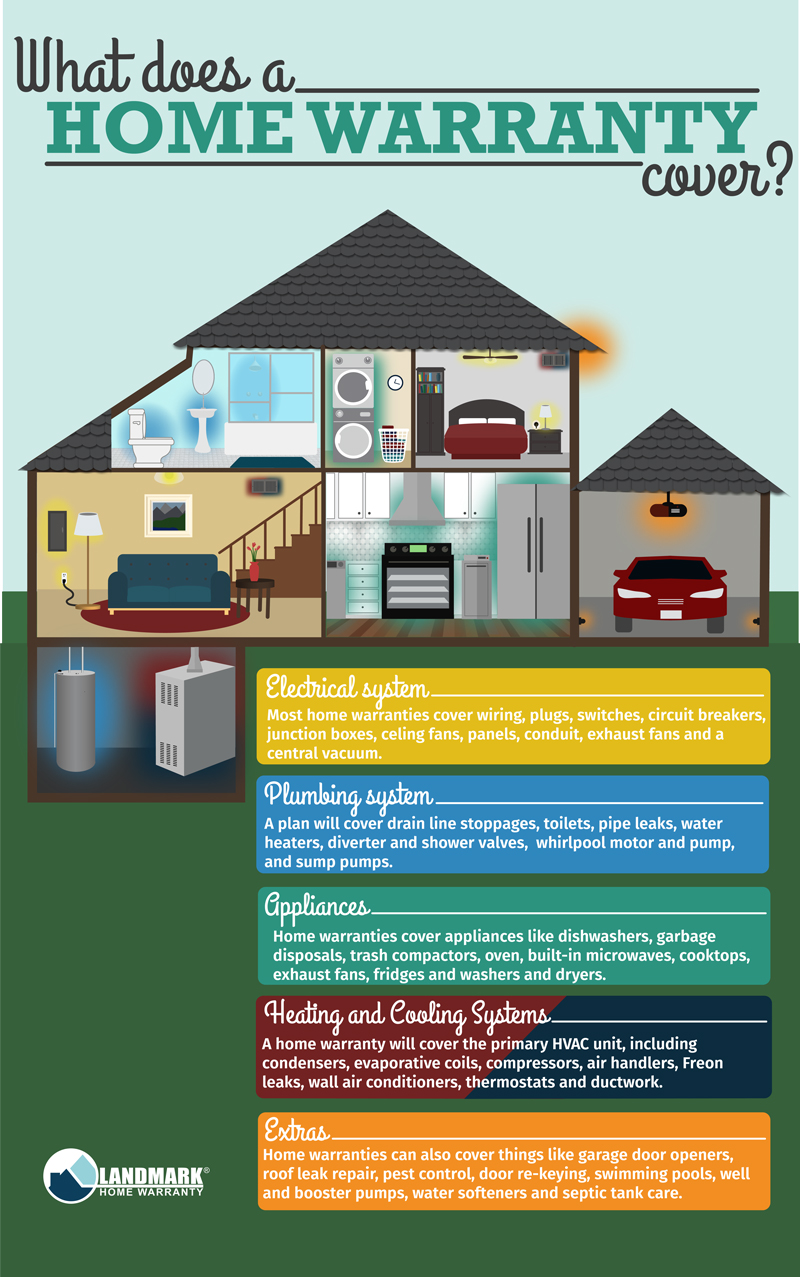

Standard Coverage: Safeguarding Your Major Systems and Appliances

Home warranty contracts are generally divided into three tiers: systems plans, appliance plans, and combination plans. Understanding these categories is essential for choosing a plan that aligns with the specific risks of your property.

Essential Home Systems

The “Systems” portion of a warranty usually covers the most expensive components of a house. These are the “bones” of the property’s utility, and their failure can lead to significant financial strain.

- HVAC (Heating, Ventilation, and Air Conditioning): This is often the most valuable part of a warranty. Repairing a furnace or an AC condenser can cost thousands.

- Electrical Systems: Coverage typically includes wiring, main breaker panels, and built-in exhaust fans.

- Plumbing Systems: This includes leaks in water lines, valves, and sometimes even the clearing of drain clogs.

- Water Heaters: Both traditional tank and tankless units are standard inclusions in system-based plans.

High-Value Kitchen and Laundry Appliances

For many, the “Appliance” plan is the gateway into home warranties. Modern appliances are increasingly reliant on complex electronics and specialized parts, making repairs more expensive than they were a decade ago.

- Kitchen Suite: This covers refrigerators (including ice makers), ovens, ranges, cooktops, and built-in microwaves.

- Dishwashers: Given the high frequency of use, dishwashers are one of the most commonly claimed items.

- Laundry Units: Clothes washers and dryers are standard inclusions. Because these involve both water and high-voltage electricity, they are prone to mechanical failures that a warranty helps mitigate.

Optional Add-ons and Specialized Protection

Many homeowners have unique assets that fall outside the “standard” box. To address this, warranty companies offer “riders” or add-ons. From a financial perspective, these should be selected only if the cost of the rider is lower than the projected depreciation and repair cost of the specific item. Common add-ons include:

- Pool and Spa equipment (pumps and filtration systems).

- Septic tank pumping and systems.

- Well pumps.

- Sump pumps.

- Roof leak repairs (limited to patches rather than full replacement).

Understanding the Financial Constraints: Exclusions and Limitations

A home warranty is not a “blank check” for home maintenance. To manage the financial risks effectively, a homeowner must be aware of the limitations that could lead to a denied claim or out-of-pocket expenses.

The Impact of Pre-existing Conditions and Improper Maintenance

Most warranty contracts exclude “pre-existing conditions”—mechanical issues that existed before the contract went into effect. Furthermore, companies often require proof of “normal wear and tear.” If a homeowner fails to change the filters in an HVAC system for three years, the provider may argue that the failure was due to negligence rather than standard use, leading to a claim denial. This emphasizes the need for homeowners to view the warranty as a supplement to, not a replacement for, proactive asset maintenance.

Coverage Caps and Aggregate Limits

Every savvy investor looks at the “ceiling” of their protection. Home warranties have specific dollar limits per item or per year. For example, a contract might have a $2,000 cap on HVAC repairs. If the repair costs $3,500, the homeowner is responsible for the $1,500 surplus. Understanding these caps is vital for determining your “net exposure” to financial loss. Before signing a contract, it is imperative to read the “Limits of Liability” section to ensure the coverage matches the replacement value of your high-end appliances.

Service Call Fees: The “Deductible”

Every time a technician is dispatched to your home, you pay a service call fee (usually between $75 and $125). This is the warranty equivalent of an insurance deductible. When calculating the financial benefit of a warranty, one must account for these fees. If you have three minor repairs in a year, the service fees alone could total $300, which, when added to your premium, raises the total cost of the protection plan.

Analyzing the ROI: When Does a Home Warranty Make Financial Sense?

Deciding whether to purchase a home warranty is a matter of Return on Investment (ROI) and risk tolerance. It is a mathematical equation based on the age of your home’s components and your ability to absorb sudden costs.

Assessing the Age and Condition of Your Assets

If you are moving into a brand-new home, most of your systems and appliances are likely covered by a manufacturer’s warranty for the first 12 to 24 months. In this scenario, a third-party home warranty might be redundant. However, if your home is 10 to 15 years old—the “danger zone” where many major systems begin to fail—the warranty becomes a highly valuable financial tool. The probability of a claim increases as the asset ages, making the premium a wise expenditure.

Calculating the Break-even Point

To perform a basic financial audit, list the age of your major appliances and their average replacement costs.

- HVAC: $5,000 – $8,000

- Refrigerator: $1,500 – $3,000

- Water Heater: $1,200 – $2,500

If the combined probability of one of these items failing in the next 12 months is high, the $600 premium is a bargain. If everything is new and high-quality, you might be better off taking that $600 and placing it into a dedicated “Home Maintenance” brokerage account or high-yield savings account, where it can earn interest while waiting to be used.

Real Estate Strategy and Resale Value

From a business finance perspective, including a home warranty in a real estate transaction can be a strategic move. Sellers often purchase a one-year warranty for the buyer as an incentive. This provides the buyer with financial peace of mind, potentially leading to a faster sale or a higher closing price. It acts as a form of “transactional insurance,” protecting the seller from post-closing disputes regarding the condition of the home’s systems.

Conclusion

A home warranty is a specialized financial instrument designed to provide stability in the often-volatile world of homeownership. While it does not cover every possible scenario—excluding structural issues and cosmetic damage—its focus on major systems and appliances provides a safety net for your primary residence.

By understanding the nuances of what is covered, acknowledging the limitations of coverage caps, and performing a rigorous cost-benefit analysis, homeowners can make informed decisions that protect their liquidity and long-term net worth. In the broader context of personal finance, a home warranty isn’t just about fixing a broken stove; it’s about maintaining a disciplined budget and ensuring that a mechanical failure doesn’t become a financial catastrophe.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.