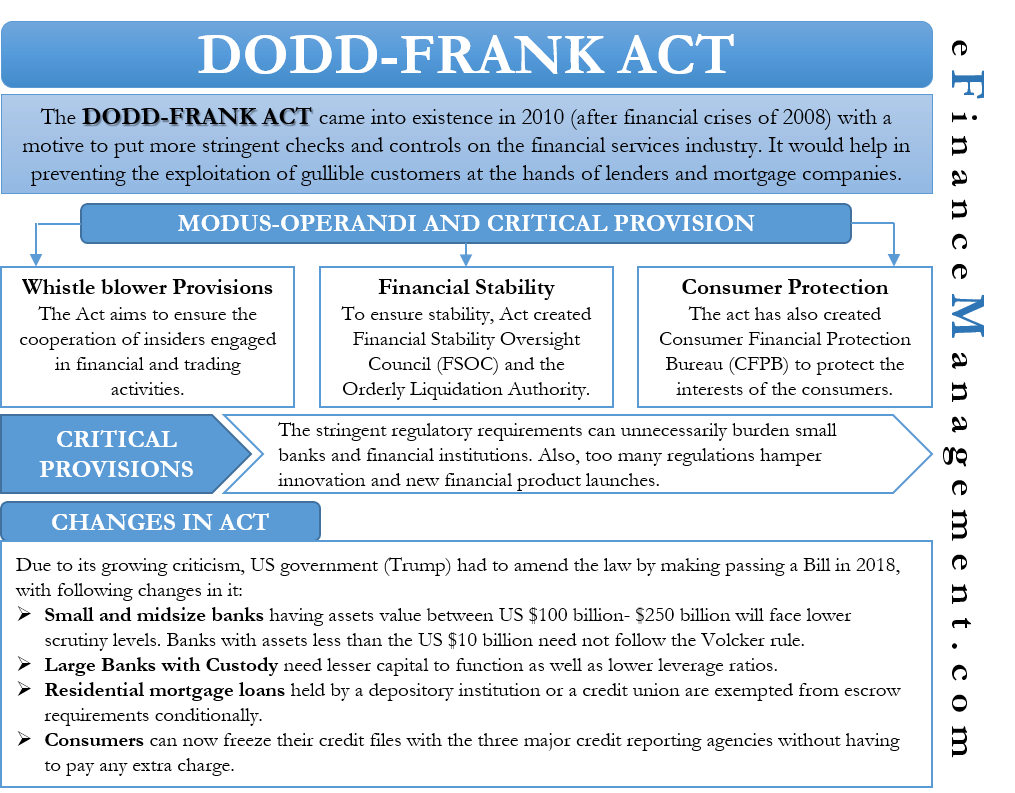

The Dodd-Frank Wall Street Reform and Consumer Protection Act, commonly known as Dodd-Frank, was enacted in 2010 in the wake of the 2008 global financial crisis. Its primary objective was to overhaul the U.S. financial regulatory system, aiming to prevent a recurrence of the systemic risks that had brought the economy to its knees. This sweeping legislation touched upon nearly every aspect of the financial industry, from the largest banks to individual consumers, fundamentally altering the landscape of financial services and oversight. While its ultimate impact and effectiveness remain subjects of ongoing debate, understanding its core provisions is crucial for grasping the evolution of financial regulation in the United States.

The Genesis of Dodd-Frank: Responding to Crisis

The financial crisis of 2008 was a catastrophic event that exposed deep-seated flaws in the U.S. financial system. The collapse of major financial institutions, the near-meltdown of the global economy, and the subsequent government bailouts fueled public outrage and a strong demand for accountability and reform. Dodd-Frank emerged as the legislative response, born out of a desire to create a more stable and transparent financial system.

The Subprime Mortgage Meltdown and Its Ripple Effects

At the heart of the crisis was the subprime mortgage market. Predatory lending practices, coupled with the securitization and widespread distribution of risky mortgage-backed securities, created a housing bubble that eventually burst. As home prices plummeted, defaults soared, triggering massive losses for financial institutions that held these complex and opaque assets. The interconnectedness of the financial system meant that the failure of one institution could have cascading effects, leading to a credit crunch that paralyzed the economy.

The Need for Enhanced Regulatory Oversight

The crisis highlighted a critical gap in regulatory oversight. Many financial institutions, particularly large and complex ones, operated with insufficient capital, engaged in excessive risk-taking, and lacked adequate transparency. The “too big to fail” phenomenon, where the potential collapse of a major institution was deemed too damaging to the economy, led to implicit government guarantees, incentivizing risky behavior. Furthermore, consumer protection in the financial marketplace was found to be woefully inadequate, with many individuals falling victim to deceptive practices.

Key Pillars of Dodd-Frank: Restructuring the Financial System

Dodd-Frank was a multifaceted piece of legislation, creating new agencies, expanding the powers of existing ones, and implementing a wide array of rules and regulations. Its provisions can be broadly categorized into several key areas, each designed to address specific vulnerabilities exposed by the crisis.

Strengthening Prudential Regulation and Systemic Risk Management

One of the most significant aspects of Dodd-Frank was its focus on strengthening the oversight of large, systemically important financial institutions (SIFIs). The act aimed to prevent another situation where the failure of a single entity could threaten the entire financial system.

The Financial Stability Oversight Council (FSOC)

Dodd-Frank established the FSOC, a council comprised of heads of various financial regulatory agencies. The FSOC’s primary mandate is to identify and monitor risks to the U.S. financial system. It has the authority to designate non-bank financial companies as SIFIs, subjecting them to enhanced prudential standards and supervision by the Federal Reserve. This designation process aimed to extend regulatory scrutiny beyond traditional banks to other entities that could pose systemic risks.

Enhanced Capital and Liquidity Requirements

Under Dodd-Frank, large banks and SIFIs were subjected to more stringent capital and liquidity requirements. These measures were designed to ensure that these institutions had sufficient financial cushions to absorb losses and continue operating during periods of stress. The goal was to reduce the likelihood of insolvency and the need for government bailouts. This included requirements for stress testing, which simulates adverse economic conditions to assess an institution’s resilience.

The Volcker Rule

Named after former Federal Reserve Chairman Paul Volcker, this provision aimed to restrict proprietary trading by banks, which is trading for their own account with their own money, rather than on behalf of clients. The rationale was that proprietary trading was excessively risky and could lead to conflicts of interest, especially when combined with traditional banking activities. By limiting such activities, the Volcker Rule sought to reduce the risk-taking of commercial banks and encourage them to focus on their core lending and deposit-taking functions.

Consumer Protection and Financial Education

The crisis exposed how vulnerable consumers could be to predatory lending and deceptive financial products. Dodd-Frank introduced significant reforms to enhance consumer protection in the financial marketplace.

The Consumer Financial Protection Bureau (CFPB)

Perhaps the most widely known creation of Dodd-Frank is the Consumer Financial Protection Bureau (CFPB). This independent agency was established to protect consumers in the financial sector by creating and enforcing rules related to mortgages, credit cards, student loans, and other financial products and services. The CFPB’s mandate includes investigating complaints, issuing regulations, and taking enforcement actions against companies that violate consumer protection laws. Its creation was a direct response to the widespread abuses identified during the subprime mortgage crisis.

Regulation of Abusive and Deceptive Practices

Dodd-Frank empowered regulatory agencies to take stronger action against abusive and deceptive practices in the financial industry. This included new rules governing mortgage origination, such as the ability-to-repay standard, which requires lenders to verify that borrowers can afford their mortgage payments. The act also enhanced disclosure requirements for financial products, aiming to provide consumers with clearer and more comprehensive information.

Increased Transparency and Accountability in Derivatives Markets

The opaque nature of the over-the-counter (OTC) derivatives market was identified as a significant contributor to the crisis. These complex financial instruments, including credit default swaps (CDS), were largely unregulated, making it difficult to assess the risks involved.

Mandating Central Clearing and Exchange Trading for Derivatives

Dodd-Frank sought to bring greater transparency and stability to the derivatives market by requiring that many OTC derivatives be cleared through central counterparties and traded on exchanges or swap execution facilities. Central clearinghouses act as intermediaries, reducing counterparty risk by guaranteeing trades even if one party defaults. Exchange trading promotes price discovery and standardization. These reforms aimed to make the derivatives market less prone to sudden shocks.

Regulation of Swap Dealers

The act also implemented regulations for swap dealers, entities that engage in the business of trading swaps. These dealers are now subject to capital requirements, margin rules, and reporting obligations, increasing their accountability and reducing the risk they pose to the broader financial system.

Ending “Too Big to Fail” and Resolving Financial Institutions

A core objective of Dodd-Frank was to address the problem of “too big to fail,” where the government felt compelled to bail out large financial institutions to prevent systemic collapse. The act introduced mechanisms to resolve failing SIFIs in an orderly manner, without resorting to taxpayer-funded bailouts.

Orderly Liquidation Authority

Dodd-Frank granted the FDIC (Federal Deposit Insurance Corporation) the authority to resolve failing SIFIs through an “orderly liquidation” process. This process is designed to wind down a failing institution in a controlled manner, protecting depositors and minimizing disruption to the financial system, while holding creditors and shareholders accountable for losses. This mechanism aimed to provide a credible alternative to bailouts.

Living Wills and Resolution Plans

Systemically important financial institutions are required to submit “living wills” or resolution plans to regulators. These plans detail how the institution could be dismantled in an orderly fashion during a crisis. This proactive planning process is intended to make the orderly liquidation authority more effective and to encourage firms to structure themselves in a way that facilitates resolution.

The Legacy and Ongoing Debate

Dodd-Frank remains one of the most significant pieces of financial legislation in modern U.S. history. Its implementation has been complex, and its effects continue to be debated by policymakers, economists, and industry participants.

Arguments for Dodd-Frank’s Successes

Proponents of Dodd-Frank argue that it has made the financial system more resilient, reducing the likelihood of another crisis of similar magnitude. They point to the increased capital buffers of banks, the enhanced consumer protections provided by the CFPB, and the greater transparency in derivatives markets as tangible successes. The absence of another major financial crisis since its enactment is often cited as evidence of its effectiveness, though the complex interplay of economic factors makes direct causation difficult to prove.

Criticisms and Calls for Reform

Critics, however, argue that Dodd-Frank has imposed excessive regulatory burdens on financial institutions, stifling economic growth and innovation. Some contend that the compliance costs are disproportionately borne by smaller institutions, making it harder for them to compete. There have also been concerns that the act has not fully resolved the “too big to fail” problem, with some arguing that the largest institutions remain implicitly government-backed. In subsequent years, some provisions of Dodd-Frank have been modified or rolled back, reflecting the ongoing political and economic debates surrounding its impact.

The Evolving Financial Landscape

The financial industry is dynamic, constantly adapting to new technologies, market conditions, and regulatory frameworks. Dodd-Frank has undeniably shaped this evolution, forcing a reevaluation of risk management, consumer engagement, and corporate governance within financial firms. The act’s influence extends beyond the immediate regulatory changes, fostering a broader cultural shift towards greater accountability and a recognition of the interconnectedness of the global financial system. As the financial world continues to change, so too will the assessment of Dodd-Frank’s enduring legacy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.