The 1929 stock market crash, notoriously known as Black Thursday and Black Tuesday, stands as a chilling testament to the fragility of economic prosperity built on speculative excess. More than just a blip in the financial calendar, it was a cataclysmic event that obliterated immense wealth, shattered public confidence, and served as a brutal harbinger of the Great Depression. Understanding its multifaceted causes is not merely an exercise in historical analysis but a crucial lesson in financial prudence, risk management, and the intricate interplay of market forces, economic policy, and human psychology. While no single factor can be pinpointed as the sole culprit, a confluence of speculative euphoria, structural economic weaknesses, and policy missteps conspired to create the perfect storm that brought the roaring 1920s to a devastating halt.

The Mirage of Prosperity: America in the 1920s

The decade leading up to 1929, often romanticized as the “Roaring Twenties,” was characterized by unprecedented economic growth, technological innovation, and a pervasive sense of optimism. Emerging victorious and relatively unscathed from World War I, the United States embarked on an era of industrial expansion, mass production, and rising consumerism. Automobiles, radios, and household appliances became symbols of a burgeoning middle class, while urban centers thrived, and cultural norms underwent rapid transformation. This seemingly limitless prosperity fueled an insatiable appetite for wealth, transforming the stock market from a tool for capital formation into a national casino.

Unbridled Speculation and the “Get Rich Quick” Mentality

At the heart of the speculative bubble was the widespread belief that stock prices would only ever go up. Fueled by tales of instant millionaires and a relentless bull market, ordinary citizens, alongside seasoned investors, poured their savings into the market. This period saw a dramatic surge in public participation, often without adequate understanding of underlying company fundamentals or market risks. Stocks were increasingly bought not for their dividend potential or intrinsic value, but solely on the expectation that their price would rise, allowing for quick resale at a profit. This “greater fool theory” drove prices to unsustainable levels, creating a disconnect between market valuations and corporate earnings.

Easy Credit and Low Interest Rates

The speculative fervor was significantly amplified by the widespread availability of easy credit. Investors could purchase stocks on “margin,” paying only a small percentage of the stock’s price upfront (as little as 10-20%) and borrowing the rest from brokers. This practice, while amplifying potential gains, also magnified potential losses. As long as stock prices rose, margin calls were rare, and profits seemed effortless. However, a significant market downturn would trigger immediate margin calls, forcing investors to either inject more capital or sell their shares, irrespective of price. Banks, eager to profit from the booming market, lent freely to brokers, who in turn lent to investors, creating a vast, interconnected web of debt. The Federal Reserve, maintaining relatively low interest rates throughout much of the decade, unintentionally encouraged this credit expansion, making borrowing cheap and attractive, further inflating the bubble.

The Illusion of Perpetual Growth

The prevailing economic philosophy and public sentiment contributed to an illusion of perpetual growth. Technological advancements, particularly in manufacturing and transportation, fostered a belief that economic expansion was limitless. Corporate profits soared, unemployment was low, and living standards improved for many. This environment fostered a dangerous complacency, leading investors to ignore warning signs and dismiss cautious voices as overly pessimistic. Analysts and economists often rationalized exorbitant stock valuations by pointing to “new paradigms” of economic growth, suggesting that traditional valuation metrics no longer applied. This psychological phenomenon, known as irrational exuberance, blinded many to the inherent risks accumulating beneath the surface of apparent prosperity.

Deep-Seated Economic Vulnerabilities

Beneath the glittering surface of the Roaring Twenties lay profound structural weaknesses within the American economy. These vulnerabilities, often masked by the booming stock market and industrial output, made the entire system highly susceptible to a shock. While the stock market crash was the immediate trigger for the Great Depression, these underlying issues ensured that the downturn would be prolonged and severe.

Unequal Distribution of Wealth

A significant flaw in the economic structure was the highly unequal distribution of wealth and income. While the industrial magnates and financial elite accumulated vast fortunes, the majority of the population saw only modest gains, or in some sectors, stagnation. This meant that while productive capacity expanded rapidly, the purchasing power of the average consumer lagged behind. Companies were producing goods at an accelerated rate, but there wasn’t a sufficiently broad base of consumers with enough disposable income to buy them. This imbalance eventually led to a critical problem of underconsumption, creating a mismatch between supply and demand.

Agricultural Distress

Even as industry boomed, the agricultural sector experienced a prolonged depression throughout the 1920s. Farmers, who had expanded production during World War I to feed Europe, faced plummeting prices and shrinking demand in the post-war era. Overproduction, coupled with high debt loads from wartime expansion, left many farmers struggling with foreclosures and bankruptcy. This significant segment of the population, unable to participate fully in the broader economic boom, represented a critical weak link in the national economy, further constraining consumer demand and contributing to overall instability.

Industrial Overproduction and Inventory Buildup

Stemming from the unequal distribution of wealth and lagging consumer demand, many industries found themselves grappling with overproduction. Factories, driven by the optimism of the boom and the availability of easy credit, continued to churn out goods at a rapid pace. However, the market for these goods began to saturate, leading to accumulating inventories in warehouses. When businesses could no longer sell their products, they were forced to cut production, reduce working hours, and lay off employees, initiating a vicious cycle of decreased income, reduced consumer spending, and further economic contraction.

Weak Banking Structure

The American banking system in the 1920s was fragmented and largely unregulated. Thousands of small, independent banks operated without adequate federal oversight or deposit insurance. Many were heavily invested in the stock market or lent extensively to speculative ventures. When the market began to turn, and loan defaults mounted, these banks faced severe liquidity crises. The absence of a strong central banking system capable of acting as a lender of last resort, coupled with the lack of federal deposit insurance, meant that bank failures often triggered cascading effects, leading to widespread panic and bank runs, further destabilizing the financial system.

International Economic Instability

The global economic landscape also played a role. Post-World War I, European nations were burdened with war debts to the U.S. and punitive reparations obligations (Germany). This created a fragile international financial system where the flow of capital was distorted. American loans to Europe, designed to facilitate reconstruction and allow repayment of war debts, created a dependency. When the U.S. economy faltered, these loans dried up, exacerbating economic woes in Europe and contributing to a global financial downturn. Protectionist trade policies, such as the Smoot-Hawley Tariff Act passed in 1930 (but debated pre-crash), signaled a move towards economic nationalism that would further cripple international trade and global economic recovery.

The Implosion: Black Thursday and Black Tuesday

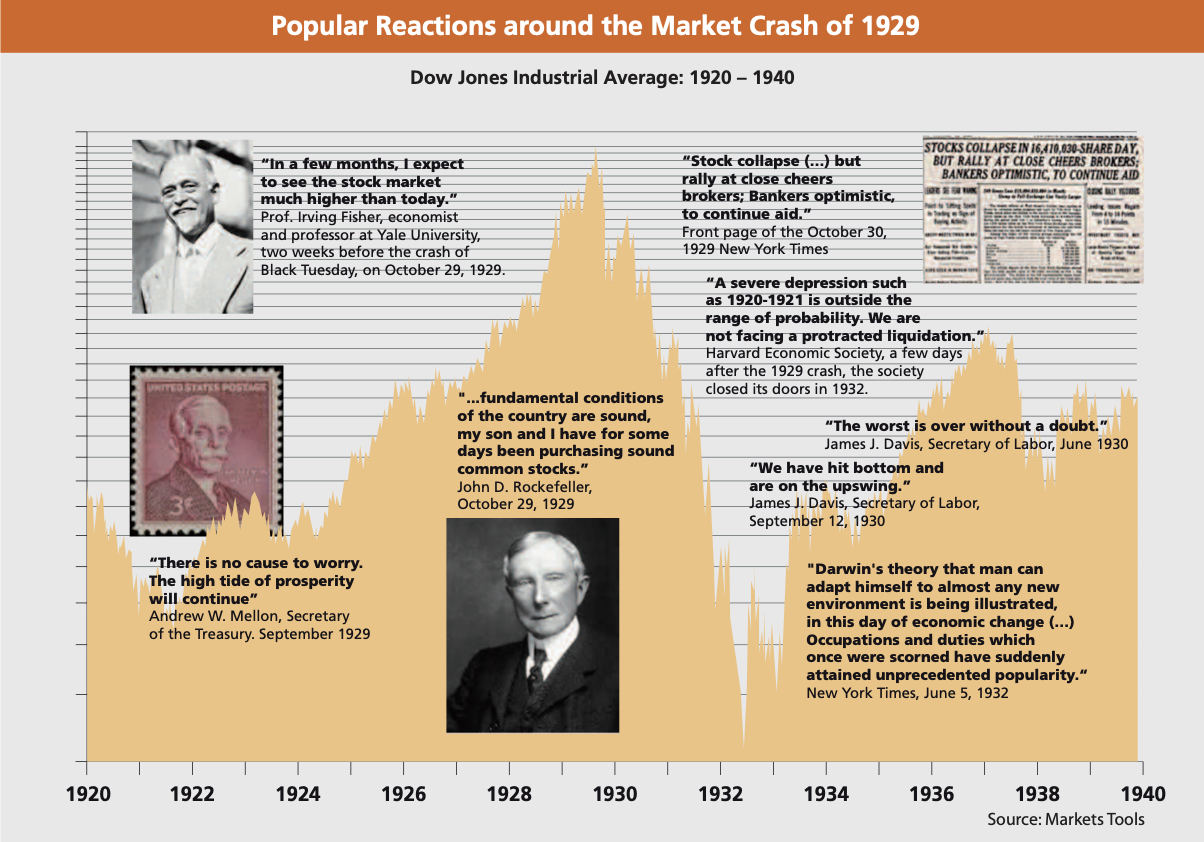

The culmination of these factors manifested dramatically in October 1929. The weeks leading up to the crash had seen increasing volatility, with market analysts expressing growing concern.

The Initial Jitters and Warning Signs

Throughout September and early October 1929, the stock market experienced several sharp dips followed by partial recoveries. These “minor” corrections served as early warning signs, causing some cautious investors to sell, but many remained confident, conditioned by years of continuous growth. Economists like Roger Babson had issued warnings about an impending crash, but they were largely dismissed by the prevailing optimism.

Margin Calls and Panic Selling

The real unraveling began on October 24, 1929, known as “Black Thursday.” A wave of frantic selling hit the New York Stock Exchange, causing prices to plummet at an alarming rate. As prices fell, brokers issued margin calls to investors who had bought stocks on credit. Unable to meet these calls, many were forced to sell their shares, often at fire-sale prices, initiating a vicious cycle. Each wave of selling drove prices lower, triggering more margin calls, and fueling further panic. The volume of shares traded reached unprecedented levels, overwhelming the market’s infrastructure.

Failed Attempts at Intervention

In an attempt to stem the tide, a consortium of leading bankers, including figures like Charles E. Mitchell of National City Bank and Thomas W. Lamont of J.P. Morgan & Co., intervened. They pooled resources and began buying large blocks of blue-chip stocks at above-market prices, hoping to restore confidence. For a brief period, their efforts appeared to stabilize the market on Black Thursday afternoon and Friday. However, this intervention proved to be a temporary reprieve.

The Final Descent

The respite was short-lived. Over the weekend, public confidence continued to erode. When the market reopened on Monday, October 28 (“Black Monday”), selling intensified, and prices plunged again. The following day, “Black Tuesday” (October 29, 1929), witnessed the most catastrophic single day in stock market history. Over 16 million shares were traded, and the Dow Jones Industrial Average fell by 12%, wiping out billions of dollars in market value. The speculative bubble had burst unequivocally, leaving a trail of financial devastation.

The Aftermath and Enduring Financial Lessons

The 1929 stock market crash was not just an isolated financial event; it was a profound turning point in American and global history, marking the end of an era of unbridled optimism and the beginning of a period of immense hardship.

Economic Contraction and the Great Depression

The immediate consequence of the crash was a severe contraction of the economy. The destruction of wealth and confidence led to a dramatic reduction in consumer spending and business investment. Banks, reeling from loan defaults and widespread withdrawals, tightened credit, making it harder for businesses to operate and expand. Unemployment soared, factories closed, and a downward spiral took hold, deepening into the Great Depression—a decade-long economic crisis that reshaped government, society, and the global financial order.

Regulatory Reforms: Safeguarding the Market

The trauma of the crash and the Depression prompted significant reforms aimed at preventing a recurrence. The U.S. government, under President Franklin D. Roosevelt, enacted landmark legislation during the New Deal era. Key among these was the establishment of the Securities and Exchange Commission (SEC) in 1934, tasked with regulating the stock market and ensuring transparency. The Glass-Steagall Act (1933) separated commercial banking from investment banking, aiming to curb speculative abuses. The creation of the Federal Deposit Insurance Corporation (FDIC) provided government insurance for bank deposits, restoring public trust in the banking system and preventing future bank runs. These regulations fundamentally transformed the financial landscape, introducing safeguards designed to protect investors and maintain market stability.

The Perils of Speculative Bubbles

The 1929 crash remains a stark reminder of the dangers of speculative bubbles. It underscores how market prices can diverge wildly from underlying economic realities when driven by herd mentality, easy credit, and the promise of quick riches. History has shown that similar patterns of irrational exuberance, though perhaps not always with the same catastrophic outcome, have repeated in various forms, from the dot-com bubble of the late 1990s to the housing market crash of 2008. Understanding market psychology and resisting the temptation to follow the crowd blindly are crucial for investors.

The Importance of Diversification and Prudent Investing

For modern investors, the lessons of 1929 are timeless. It highlights the importance of diversification, ensuring that one’s investments are spread across various asset classes and sectors to mitigate risk. It also emphasizes the need for prudent investing, focusing on fundamental analysis, long-term growth, and a clear understanding of one’s risk tolerance, rather than chasing speculative gains. The crash underscored that investing is not a guaranteed path to wealth and that thorough research, patience, and a healthy dose of skepticism are essential attributes for navigating the complexities of financial markets. The 1929 crash reshaped the regulatory framework of financial markets and instilled a cautious wisdom that continues to inform economic policy and investment strategies to this day.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.