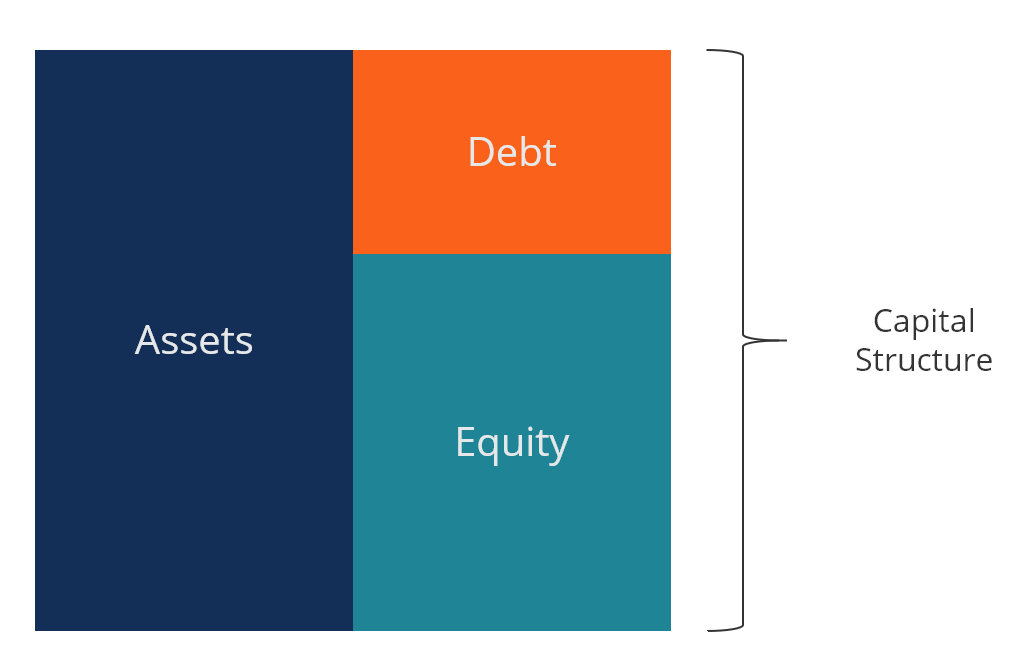

In the world of business finance, few concepts are as foundational—yet as complex—as capital structure. Whether you are a solo entrepreneur launching a side hustle, a CFO of a mid-sized enterprise, or an investor looking to evaluate a company’s health, understanding the mix of funds used to finance operations is critical. At its simplest level, capital structure refers to the specific mixture of debt and equity used by a company to finance its overall operations and growth. It is the financial architecture that supports every decision a business makes.

Determining the “right” capital structure is not a one-size-fits-all endeavor. It involves a delicate balancing act between risk and reward, cost and flexibility, and control and obligation. This article explores the nuances of capital structure, the theories that govern it, and how businesses can optimize their financial mix to ensure long-term sustainability.

The Core Components of Capital Structure

To understand capital structure, one must first break down the two primary pillars of corporate finance: debt and equity. While most businesses use a combination of both, the proportion of each can tell a deep story about the company’s risk profile and strategic priorities.

Equity Financing: Ownership and Long-Term Commitment

Equity represents ownership in the company. When a business raises money through equity, it sells a piece of itself to investors. This can come in the form of common stock, preferred stock, or retained earnings (profits kept within the business rather than paid out as dividends).

The primary advantage of equity is that it does not require repayment. Unlike a loan, there are no monthly interest payments that could strain cash flow during lean times. However, equity is often considered the “most expensive” form of capital in the long run. Investors demand a higher rate of return to compensate for the risk of being last in line for payment if the company fails. Furthermore, issuing equity leads to dilution, meaning the original owners have a smaller claim on future profits and potentially less control over decision-making.

Debt Financing: Leverage and Obligation

Debt financing involves borrowing money from outside sources, such as banks, bondholders, or private lenders. The company agrees to pay back the principal amount plus interest over a predetermined period.

The allure of debt lies in its relative “cheapness” compared to equity. Because lenders have a legal claim to be paid before shareholders, their risk is lower, and thus the interest rate they charge is typically lower than the expected return on equity. Additionally, in many jurisdictions, interest payments are tax-deductible, creating an “interest tax shield” that further reduces the effective cost of borrowing. The downside, of course, is the obligation. If a company cannot meet its debt service requirements, it faces the risk of bankruptcy or insolvency.

Hybrid Securities: The Middle Ground

Between pure debt and pure equity lie hybrid instruments, such as convertible bonds or mezzanine financing. These tools offer the fixed-income characteristics of debt but can be converted into equity under certain conditions. They provide companies with flexible options to raise capital when traditional bank loans are too restrictive or when the stock market is too volatile for a secondary offering.

Finding the Optimal Capital Structure

Financial managers spend significant time trying to identify the “Optimal Capital Structure”—the specific mix of debt and equity that minimizes the company’s Weighted Average Cost of Capital (WACC) while maximizing its market value.

The Weighted Average Cost of Capital (WACC)

WACC is a calculation of a business’s cost of capital in which each category of capital is proportionately weighted. All sources of capital, including common stock, preferred stock, bonds, and any other long-term debt, are included in a WACC calculation. By lowering the WACC, a company increases its valuation because future cash flows are discounted at a lower rate. Generally, as a firm adds debt to its structure, the WACC decreases due to the tax-deductibility of interest. However, this only works up to a certain point.

The Trade-Off Theory

The Trade-Off Theory suggests that companies balance the benefits of debt (the tax shield) against the costs of potential financial distress. As a company takes on more debt, the probability of default increases. This risk causes lenders to demand higher interest rates and makes equity investors nervous, eventually driving the WACC back up. The “optimal” point is the peak of the curve where the marginal benefit of another dollar of debt equals the marginal cost of the increased risk of bankruptcy.

The Pecking Order Theory

In contrast to the Trade-Off Theory, the Pecking Order Theory suggests that companies follow a specific hierarchy when seeking finance. They prefer internal financing (retained earnings) first, followed by debt, and finally issuing new equity as a last resort. This theory is rooted in “asymmetric information”—the idea that managers know more about the company’s true value than outside investors. Issuing new equity can be seen as a signal that the stock is overvalued, whereas taking on debt signals confidence in the ability to repay.

Internal and External Factors Influencing the Financial Mix

No company exists in a vacuum. The decision to lean toward debt or equity is often dictated by the environment in which the business operates and the internal characteristics of the firm itself.

Industry Norms and Asset Tangibility

Different industries have vastly different capital structures. For instance, utility companies or real estate investment trusts (REITs) often carry high levels of debt. They have stable, predictable cash flows and significant tangible assets (like power plants or buildings) that can serve as collateral.

On the other hand, a software-as-a-service (SaaS) company might rely almost entirely on equity. Their primary assets are intangible—intellectual property and human capital—which banks are hesitant to lend against. Furthermore, the volatility of high-growth tech means that the rigid obligations of debt could be fatal during a market downturn.

Tax Policy and Interest Rates

Macroeconomic factors play a massive role in capital structure. In a low-interest-rate environment, the cost of debt is historically cheap, encouraging businesses to leverage up to fund acquisitions or share buybacks. Similarly, corporate tax rates influence the “tax shield” benefit. If the corporate tax rate is high, the incentive to use debt is stronger. If the tax rate is low, the relative benefit of debt decreases.

Financial Flexibility and Growth Stage

A startup in its “burn phase” rarely qualifies for traditional debt because it lacks the cash flow to service interest. These companies rely on venture capital (equity). As a company matures and moves toward profitability, it gains access to the credit markets. Mature companies often use debt strategically to optimize their balance sheets, while keeping some “dry powder” (unused borrowing capacity) for future opportunities or unexpected crises.

The Impact on Investors and Business Valuation

For an investor, the capital structure is a vital indicator of a company’s risk profile. It dictates how profits are shared and how the company will weather economic storms.

Financial Leverage and Earnings Per Share (EPS)

Financial leverage is the use of borrowed money to increase the potential return on an investment. When a company uses debt to finance a project that earns a return higher than the interest rate on the debt, the “excess” profit goes to the shareholders. This can significantly boost Earnings Per Share (EPS) and Return on Equity (ROE). However, leverage is a double-edged sword. If the project underperforms, the fixed interest costs must still be paid, which can wipe out shareholder earnings much faster than if the project had been funded by equity alone.

Market Perception and Credit Ratings

Rating agencies like Moody’s and S&P evaluate a company’s capital structure to assign credit ratings. A high debt-to-equity ratio might lead to a credit downgrade, which increases the cost of future borrowing. Investors also look at “solvency ratios,” such as the interest coverage ratio, to determine how easily a company can pay its debts from its operating income. A company that is “over-leveraged” is often viewed as a risky bet, leading to a lower stock price multiple.

Strategic Management of Capital Structure

Managing capital structure is not a “set it and forget it” task. It requires constant monitoring and strategic adjustments based on the company’s performance and the external market.

Recapitalization Strategies

Sometimes a company decides its current mix is no longer optimal. It may undergo a “leveraged recapitalization,” where it takes on a large amount of debt to buy back shares, effectively shifting the structure toward debt to boost ROE. Conversely, an over-leveraged company might engage in an equity offering to pay down debt, “de-leveraging” the balance sheet to reduce the risk of bankruptcy.

Managing Dilution vs. Default

The ultimate challenge for a financial manager is choosing between the risk of dilution and the risk of default. Issuing equity protects the company from the threat of bankruptcy but dilutes the ownership of current shareholders and may signal weakness to the market. Taking on debt protects ownership and provides tax benefits but introduces the threat of financial ruin if cash flows falter.

Conclusion: The Dynamic Nature of Capital

Capital structure is the heartbeat of business finance. It is a reflection of a company’s past successes, its current stability, and its future ambitions. By carefully balancing debt and equity, businesses can create a robust foundation that allows them to innovate, expand, and survive economic volatility. For the savvy business owner or investor, “what capital structure” is not just a technical question—it is a strategic inquiry into the very soul of a company’s financial health. Understanding these principles ensures that capital remains a tool for growth rather than a burden of obligation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.