Understanding mortgage rates is paramount for anyone looking to buy a home, refinance an existing loan, or simply track the pulse of the real estate market. These rates, which represent the cost of borrowing money to purchase a property, are dynamic and influenced by a complex web of economic indicators, monetary policy, and market sentiment. For the average consumer, fluctuating rates can mean the difference between an affordable monthly payment and a stretched budget, significantly impacting purchasing power and long-term financial health. In today’s economic climate, where inflation, central bank actions, and geopolitical events cast long shadows, keeping a finger on the pulse of mortgage rates is more critical than ever. This article delves into the intricacies of mortgage rates, exploring the factors that drive them, the various types available, and strategies for securing the most favorable terms in a constantly evolving market.

Understanding the Fundamentals of Mortgage Rates

To effectively navigate the housing market, it’s essential to grasp the core concepts behind mortgage rates and the foundational elements that shape their movement.

What is a Mortgage Rate?

At its simplest, a mortgage rate is the interest rate charged by a lender on a mortgage loan. It’s expressed as a percentage of the principal loan amount and determines how much you’ll pay back over the life of the loan in addition to the principal. The higher the rate, the more expensive the loan. There are primarily two types of rates:

- Fixed-Rate: The interest rate remains constant for the entire duration of the loan. This offers predictability in monthly payments, making budgeting easier.

- Adjustable-Rate (ARM): The interest rate is fixed for an initial period (e.g., 3, 5, 7, or 10 years) and then adjusts periodically based on a predetermined index, plus a margin. ARMs can offer lower initial payments but introduce uncertainty regarding future payment amounts.

Key Factors Influencing Mortgage Rates

Mortgage rates are not set in a vacuum; they are a response to broader economic forces. Understanding these can help predict future movements.

- Federal Reserve Policy: While the Fed doesn’t directly set mortgage rates, its actions, particularly regarding the federal funds rate, heavily influence the overall cost of borrowing across the economy. When the Fed raises its benchmark rate, it typically leads to higher borrowing costs for banks, which then pass those costs on to consumers in the form of higher mortgage rates.

- Inflation: High inflation erodes the purchasing power of money over time. Lenders demand higher interest rates to compensate for the diminished value of future repayments. The market’s expectation of future inflation is a significant driver of long-term interest rates, including mortgage rates.

- Economic Growth: A strong economy often signals higher demand for loans and greater investment opportunities, potentially pushing rates up. Conversely, a weaker economy might lead to lower rates as the Fed tries to stimulate activity.

- Bond Market Performance: Mortgage rates are closely tied to the yields on U.S. Treasury bonds, particularly the 10-year Treasury note. As Treasury yields rise, mortgage rates generally follow suit, and vice versa. This is because mortgage-backed securities (MBS), which are bundles of mortgages, compete with government bonds for investor attention.

- Housing Market Supply and Demand: While less direct, an imbalance in the housing market can also exert some pressure. High demand coupled with low supply can create a competitive environment that might indirectly contribute to rate stability or upward pressure if overall economic conditions support it.

How Lenders Determine Your Specific Rate

Even with general market rates, your individual circumstances play a crucial role in the rate you’re offered.

- Credit Score: A higher credit score (typically above 740-760) indicates lower risk to lenders, often qualifying you for the best rates. Lower scores will result in higher rates.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI (ideally below 43%) demonstrates your ability to manage debt and makes you a more attractive borrower.

- Loan-to-Value (LTV) Ratio and Down Payment: A larger down payment means a lower LTV, signifying less risk for the lender. Borrowers with substantial down payments typically secure better rates.

- Loan Type and Term: Different loan products (e.g., FHA, VA, conventional) and terms (e.g., 15-year vs. 30-year) come with varying rates. Shorter-term loans generally have lower rates because the lender’s money is tied up for less time.

- Loan Amount: Very small or very large loan amounts can sometimes have slightly different pricing adjustments.

The Current Landscape: What’s Driving Rates Today?

The trajectory of mortgage rates is a constant topic of discussion and analysis, particularly given recent economic volatility. Understanding the present drivers is key to making informed decisions.

Recent Trends and Historical Context

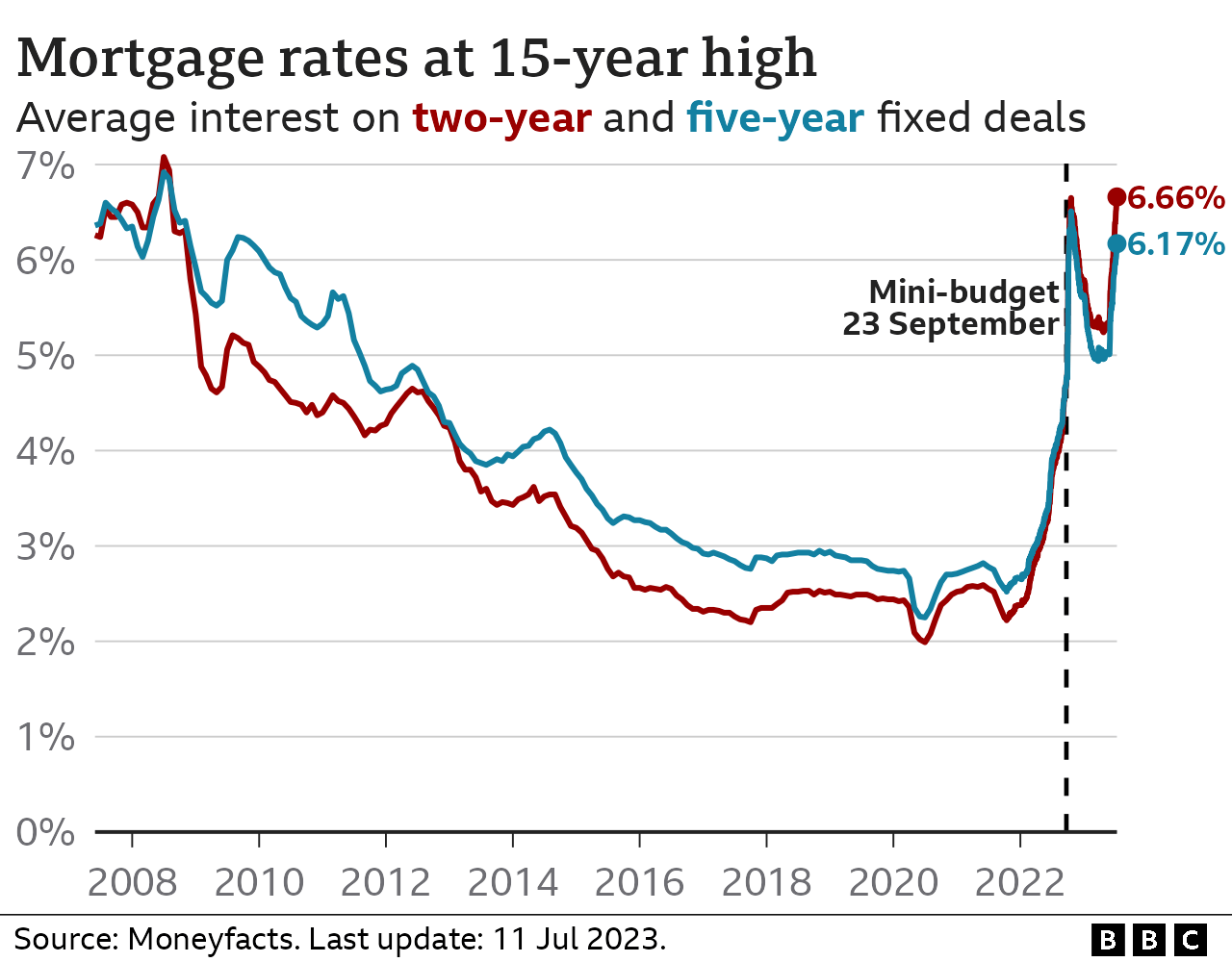

Over the past few decades, mortgage rates have seen significant swings, from historical lows experienced during the post-2008 recession and the COVID-19 pandemic, to the more elevated levels seen in previous eras and again in recent years. The ultra-low rates of 2020-2021 provided an unprecedented opportunity for homebuyers and refinancers, but this period was short-lived. Since then, we’ve witnessed a substantial climb, largely in response to aggressive monetary policy aimed at taming inflation. While current rates might seem high compared to recent historical lows, a broader historical perspective shows them to be closer to long-term averages, albeit with unique underlying economic pressures.

Impact of Inflationary Pressures

Inflation is arguably the single most dominant factor influencing mortgage rates today. When inflation runs hot, the purchasing power of money diminishes. Lenders, who are essentially giving you money today in exchange for future payments, demand a higher return to compensate for the expected loss of that money’s value over time. This “inflation premium” is built into interest rates. Additionally, the actions taken by central banks to combat inflation directly impact rates.

The Federal Reserve’s Role and Market Expectations

The Federal Reserve plays a pivotal, albeit indirect, role in shaping mortgage rates. By raising the federal funds rate – the rate at which banks lend to each other overnight – the Fed increases the cost of borrowing for financial institutions. These higher costs are then passed on to consumers across various loan products, including mortgages. The market constantly anticipates the Fed’s next moves, and these expectations alone can cause rates to shift even before an official announcement. Furthermore, quantitative tightening (the Fed reducing its balance sheet by letting bonds mature without reinvesting) also contributes to upward pressure on long-term rates by reducing demand for mortgage-backed securities. Uncertainty around the Fed’s future path, especially concerning when rate cuts might occur, keeps volatility in the mortgage market elevated.

Types of Mortgages and Their Rate Implications

The choice of mortgage product significantly impacts the rate you secure and your long-term financial commitment. Each type comes with its own set of characteristics and rate considerations.

Fixed-Rate Mortgages

Fixed-rate mortgages are the most common choice, renowned for their stability. The interest rate remains constant for the entire loan term, which typically ranges from 10 to 30 years.

- Predictability: Your principal and interest payment will never change, offering peace of mind and simplified budgeting.

- Common Terms: The 30-year fixed-rate mortgage is the most popular, offering lower monthly payments due to the extended repayment period. A 15-year fixed-rate mortgage typically comes with a lower interest rate than a 30-year, but requires higher monthly payments, allowing borrowers to pay off their home much faster and save significantly on total interest.

- Rate Premium: Fixed rates usually start higher than initial adjustable rates because lenders assume the risk of future interest rate increases.

Adjustable-Rate Mortgages (ARMs)

ARMs offer an initial period (e.g., 5, 7, or 10 years) where the interest rate is fixed, often at a lower rate than comparable fixed-rate mortgages. After this introductory period, the rate adjusts periodically, typically once a year, based on a market index plus a fixed margin.

- Initial Savings: ARMs can be attractive for borrowers who plan to sell or refinance before the fixed-rate period ends, or for those who anticipate their income increasing significantly in the future.

- Rate Uncertainty: The primary drawback is the risk that your payments could increase substantially if market rates rise after the fixed period. Most ARMs have caps that limit how much the rate can increase in a single adjustment period and over the life of the loan, but payments can still become unpredictable.

- Hybrid ARMs: These are the most common type, designated by two numbers (e.g., 5/1 ARM). The first number indicates the length of the fixed-rate period in years, and the second indicates how often the rate will adjust after that period (e.g., every 1 year).

Government-Backed Loans (FHA, VA, USDA)

These loans are insured or guaranteed by federal agencies, making them more accessible to certain borrower groups and often coming with specific rate considerations.

- FHA Loans: Insured by the Federal Housing Administration, these loans are popular for first-time homebuyers or those with lower credit scores. They often have more lenient credit and down payment requirements. While FHA rates are generally competitive with conventional loans, they require mortgage insurance premiums (MIP) which add to the overall cost.

- VA Loans: Guaranteed by the Department of Veterans Affairs, these loans are available to eligible service members, veterans, and surviving spouses. They offer significant benefits, including no down payment requirements and typically very competitive interest rates, often among the lowest available. There is usually a funding fee, but no ongoing mortgage insurance.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans are for low- to moderate-income borrowers in eligible rural areas. They also typically require no down payment and offer competitive rates, but income and property location restrictions apply.

Strategies for Securing the Best Mortgage Rate

Even in a challenging market, proactive steps can significantly improve your chances of securing a favorable mortgage rate.

Improving Your Financial Profile

Lenders view you through the lens of risk, and a stronger financial profile translates to lower perceived risk and better rates.

- Boost Your Credit Score: Pay bills on time, reduce credit card balances, avoid opening new lines of credit before applying for a mortgage, and dispute any errors on your credit report. A higher score directly correlates with lower rates.

- Reduce Debt-to-Income (DTI) Ratio: Pay down existing debts, especially high-interest credit cards or personal loans. A lower DTI indicates you have more disposable income to cover your mortgage payments.

- Increase Savings and Down Payment: A larger down payment reduces your loan-to-value (LTV) ratio, signaling less risk to the lender. It can also help you avoid private mortgage insurance (PMI) on conventional loans, further reducing your monthly housing cost.

Shopping Around and Comparing Lenders

One of the most effective strategies is to obtain quotes from multiple lenders. Mortgage rates can vary significantly from one institution to another, even on the same day for the same borrower.

- Get Multiple Quotes: Contact at least 3-5 different lenders – including banks, credit unions, and mortgage brokers. Don’t just look at the advertised rate; request a Loan Estimate (LE) which details the interest rate, estimated monthly payment, and closing costs.

- Compare Apples to Apples: Ensure you’re comparing the same loan type, term, and rate lock period across all estimates. Pay close attention to lender fees (origination fees, underwriting fees, etc.) as these can add up.

- Leverage Competition: If one lender offers a particularly good rate, you can sometimes use that as leverage to negotiate a better deal with another preferred lender.

Understanding Rate Locks and Buy-Down Options

Timing and specific loan features can also play a role in optimizing your rate.

- Rate Lock: Once you’ve found a suitable rate, you can “lock” it for a specific period (e.g., 30, 45, or 60 days) during the underwriting process. This protects you from rate increases before closing, but it typically doesn’t allow you to benefit if rates fall. Longer lock periods can sometimes come with a slightly higher rate or a fee.

- Mortgage Points (Buy-Downs): You can pay an upfront fee, known as “points,” to reduce your interest rate. One point typically equals 1% of the loan amount. This can be a wise strategy if you plan to stay in the home for a long time, as the savings on interest can eventually outweigh the upfront cost. Conversely, lenders also offer “lender credits” where they pay some of your closing costs in exchange for a slightly higher interest rate.

Refinancing Opportunities

For current homeowners, refinancing can be a powerful tool to adjust to new market conditions.

- Lowering Your Interest Rate: If current rates are significantly lower than your existing mortgage rate, refinancing can reduce your monthly payments and overall interest paid.

- Changing Loan Term: You can refinance a 30-year loan into a 15-year loan to pay it off faster (though with higher monthly payments) or extend a shorter-term loan to reduce payments.

- Cash-Out Refinance: This allows you to tap into your home equity by taking out a new, larger loan and receiving the difference in cash, often used for home improvements or debt consolidation. However, it means taking on more debt.

- Consider Break-Even Point: Always calculate the break-even point for a refinance – how long it will take for the savings from a lower interest rate to offset the closing costs of the new loan.

Conclusion

Mortgage rates are a cornerstone of the housing market, directly impacting affordability and shaping the financial landscape for millions. Their current levels are a complex interplay of economic indicators, central bank policy, and global events, making it crucial for prospective homeowners and those looking to refinance to stay informed and proactive. By understanding the fundamentals of how rates are determined, the current drivers behind their movements, the various mortgage products available, and, most importantly, by strategically preparing your finances and diligently shopping for the best terms, you can position yourself to make the most informed and beneficial decisions in today’s dynamic market. Navigating mortgage rates successfully requires patience, research, and a clear understanding of your personal financial goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.