Navigating the landscape of homeownership often begins with a fundamental question: what are the current interest rates on home loans? This isn’t just a casual query; it’s the cornerstone of financial planning for millions of aspiring homeowners and those looking to refinance. Mortgage interest rates are dynamic, influenced by a complex interplay of economic indicators, Federal Reserve policies, global events, and individual borrower profiles. Understanding these rates is crucial, as even a seemingly small percentage point difference can translate into tens of thousands of dollars over the lifespan of a 15-year or 30-year mortgage, significantly impacting monthly payments and overall affordability.

In today’s ever-evolving financial climate, staying informed about the latest trends and understanding the mechanisms that drive these rates is not merely advantageous—it’s essential. This comprehensive guide will delve into the current state of home loan interest rates, unpack the primary factors that dictate their movement, offer strategies for securing the most favorable terms, and explore their broader implications for the housing market and your personal finances. Whether you’re a first-time homebuyer, considering a refinance, or simply curious about the economic currents affecting real estate, gaining clarity on interest rates is your first step towards making an informed and financially sound decision.

Understanding the Dynamics of Mortgage Rates

Mortgage rates are not static figures but rather a reflection of the broader economic environment and the specific risks associated with lending. To truly grasp “current interest rates,” one must first understand the underlying forces that cause them to fluctuate daily, weekly, and yearly.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

The first distinction prospective borrowers encounter is between fixed-rate and adjustable-rate mortgages.

- Fixed-Rate Mortgages: These loans maintain the same interest rate for the entire duration of the loan term, typically 15 or 30 years. This predictability offers stability, making budgeting easier as monthly principal and interest payments remain constant. They are often preferred in periods of economic uncertainty or when rates are perceived to be low.

- Adjustable-Rate Mortgages (ARMs): ARMs start with a lower fixed interest rate for an initial period (e.g., 3, 5, 7, or 10 years), after which the rate adjusts periodically based on a predetermined index plus a margin. While the initial lower rate can make homes more affordable in the short term, the risk lies in potential future rate increases, which could lead to significantly higher monthly payments. ARMs are often more attractive when borrowers expect interest rates to fall or plan to sell/refinance before the adjustment period.

Key Economic Indicators Influencing Rates

Several macroeconomic factors exert significant influence over mortgage rates:

- Inflation: Perhaps the most critical driver. Lenders charge higher interest rates to compensate for the erosion of purchasing power due to inflation. When inflation is high or expected to rise, mortgage rates generally follow suit.

- Economic Growth: A strong economy typically means more demand for loans and higher rates, as businesses expand and consumers spend. Conversely, a weakening economy might lead to lower rates to stimulate borrowing and investment.

- Employment Data: Robust job growth signals a healthy economy, which can contribute to higher inflation and, consequently, higher interest rates. Unemployment, on the other hand, can suggest economic weakness and put downward pressure on rates.

- Housing Market Activity: High demand for homes can, indirectly, put upward pressure on rates as the overall economy is perceived as strong. Inventory levels and sales volumes also play a role in the broader lending environment.

The Federal Reserve’s Role and Monetary Policy

While the Federal Reserve (the Fed) does not directly set mortgage rates, its actions profoundly impact them.

- Federal Funds Rate: The Fed sets the target for the federal funds rate, which is the rate banks charge each other for overnight borrowing. Changes to this benchmark ripple through the financial system, influencing the prime rate and, subsequently, other lending rates, including those for mortgages.

- Quantitative Easing/Tightening: In periods of economic stress, the Fed might engage in quantitative easing (QE) by buying mortgage-backed securities (MBSs) to inject liquidity into the market and push down long-term rates. Conversely, quantitative tightening (QT) involves selling or letting MBSs mature, which can lead to higher long-term rates.

- Forward Guidance: The Fed’s communication about its future policy intentions (known as forward guidance) can also influence market expectations and, thus, current mortgage rates. Expectations of future rate hikes often cause current rates to climb.

Factors Shaping Your Specific Interest Rate

Beyond the broader economic landscape, the interest rate you are offered on a home loan is highly personalized. Lenders assess individual borrower profiles to determine the level of risk involved, which directly translates into the rate they are willing to provide.

Your Credit Score and Financial Health

Your creditworthiness is arguably the most significant personal factor.

- Credit Score (FICO Score): A higher credit score (typically 740+) indicates a responsible borrower with a strong history of repaying debts, qualifying you for the most favorable interest rates. Lower scores, conversely, signal higher risk to lenders, resulting in higher rates or even denial of a loan.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI (generally below 43%) demonstrates that you can comfortably manage additional debt, making you a less risky borrower.

- Payment History: A consistent history of on-time payments across all your debts reinforces your reliability as a borrower.

Loan-to-Value (LTV) Ratio and Down Payment

The Loan-to-Value (LTV) ratio measures the amount of your loan compared to the appraised value of the home.

- Down Payment: A larger down payment results in a lower LTV ratio. Lenders perceive lower LTVs as less risky because the borrower has more equity in the home. A common threshold is 20% down, which not only often secures a better interest rate but also typically eliminates the need for private mortgage insurance (PMI).

- Equity: For refinancing, the amount of equity you have in your home plays a similar role. More equity often means better rates.

Loan Term, Type, and Lender Selection

The specifics of the loan product you choose also influence the rate.

- Loan Term: Shorter loan terms (e.g., 15-year fixed) generally come with lower interest rates than longer terms (e.g., 30-year fixed). While monthly payments are higher with a 15-year loan, you pay significantly less interest over the life of the loan.

- Loan Type: Government-backed loans (FHA, VA, USDA) often have different rate structures and qualification criteria compared to conventional loans. FHA loans, for instance, might be more accessible for those with lower credit scores but typically require mortgage insurance premiums for the life of the loan.

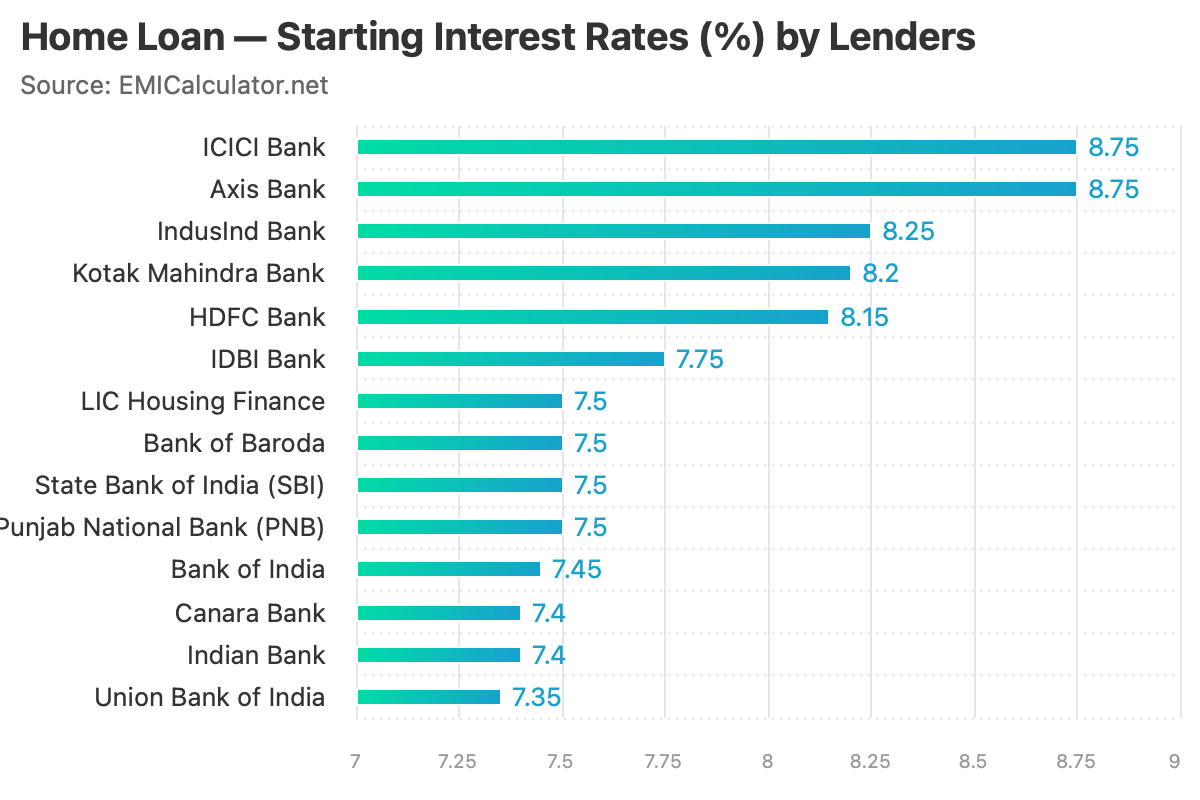

- Lender Selection: Different lenders (banks, credit unions, online lenders, mortgage brokers) have varying cost structures, risk appetites, and overheads, leading to differences in the rates they offer. Shopping around is critical.

Navigating the Market: Strategies for Securing the Best Rate

Given the personalized nature of mortgage rates and their profound long-term impact, being proactive and strategic is paramount to securing the most favorable terms.

Shopping Around and Comparing Lenders

This is perhaps the single most effective strategy. Many borrowers make the mistake of only checking with one or two lenders.

- Obtain Multiple Quotes: Apply for pre-approval with at least 3-5 different lenders (banks, credit unions, online lenders, and mortgage brokers). Do this within a short window (typically 14-45 days) to minimize the impact on your credit score, as multiple mortgage inquiries within this timeframe are often treated as a single inquiry.

- Compare Loan Estimates: Lenders are required to provide a “Loan Estimate” form detailing the interest rate, closing costs, and other loan terms. Scrutinize these forms carefully, paying attention to the Annual Percentage Rate (APR), which includes fees and other costs beyond just the interest rate.

Improving Your Creditworthiness

Prior to applying for a mortgage, taking steps to boost your credit score can yield substantial savings.

- Review Your Credit Report: Obtain free copies of your credit report from Equifax, Experian, and TransUnion. Dispute any errors immediately.

- Pay Down Debt: Reduce balances on credit cards and other revolving credit. A lower credit utilization ratio (how much credit you’re using versus how much is available) can significantly improve your score.

- Avoid New Credit: Refrain from opening new credit accounts or making large purchases on existing credit in the months leading up to your mortgage application.

- On-Time Payments: Ensure all bill payments are made on time, every time. Payment history is the biggest factor in your credit score.

Understanding Discount Points and Closing Costs

Beyond the raw interest rate, various fees and costs influence the overall expense of your loan.

- Discount Points: These are upfront fees paid to the lender at closing to “buy down” your interest rate. One point typically costs 1% of the loan amount. If you plan to stay in the home for a long time, paying points can save you money over the life of the loan, but it’s essential to calculate the break-even point.

- Closing Costs: These include appraisal fees, origination fees, title insurance, attorney fees, and more. While some closing costs are fixed, others can be negotiated. Factor these into your overall loan comparison.

The Importance of Rate Locks

Once you’ve found a desirable rate, you can “lock” it for a specific period (e.g., 30, 45, or 60 days).

- Protection from Fluctuations: A rate lock protects you from potential increases in interest rates while your loan application is being processed.

- Timing is Key: Lenders typically charge a small fee for longer lock periods. It’s crucial to lock your rate when you’re confident in your chosen lender and are far enough along in the process that your closing date is within the lock period.

The Impact of Interest Rates on Home Affordability and the Market

Current interest rates extend their influence far beyond individual loan terms; they are a critical determinant of home affordability and play a pivotal role in shaping the broader housing market.

Calculating Your Monthly Payments and Long-Term Costs

Even a slight shift in interest rates can dramatically alter the financial burden of homeownership.

- Monthly Payment: A higher interest rate means a larger portion of your monthly payment goes toward interest, leaving less for principal repayment. This directly impacts your budget and how much home you can afford.

- Total Interest Paid: Over a 30-year mortgage, the cumulative difference in interest paid between a 6% rate and a 7% rate on a $400,000 loan can amount to tens, if not hundreds, of thousands of dollars. Online mortgage calculators are invaluable tools for understanding these long-term implications.

Refinancing Opportunities and Considerations

Existing homeowners closely monitor interest rates for potential refinancing opportunities.

- Lowering Monthly Payments: If current rates drop significantly below your existing mortgage rate, refinancing can lead to lower monthly payments, freeing up cash flow.

- Changing Loan Terms: Refinancing can also allow you to switch from an ARM to a fixed-rate mortgage, reduce your loan term, or tap into your home equity.

- Cost-Benefit Analysis: Refinancing incurs new closing costs, so it’s essential to calculate whether the savings from a lower interest rate outweigh these upfront expenses. A general rule of thumb is to consider refinancing if you can lower your rate by at least 0.75% to 1.00%.

Market Trends and Future Rate Projections

The direction of interest rates significantly impacts buyer demand and housing inventory.

- Buyer Demand: Lower rates typically stimulate buyer demand by making homes more affordable, often leading to increased sales and potentially higher home prices. Conversely, rising rates can cool down the market, reducing demand and sometimes leading to price stabilization or even slight declines.

- Seller Behavior: In a high-rate environment, some potential sellers might be reluctant to list their homes if it means trading their low-rate mortgage for a new, higher-rate one. This can affect inventory levels.

- Expert Forecasts: While no one can predict the future with certainty, financial institutions and economic analysts regularly publish forecasts for interest rates. These projections, based on anticipated economic performance and central bank policies, can provide valuable insights for planning but should always be taken with a degree of caution.

Conclusion: Making Informed Decisions in a Dynamic Landscape

The question “what are the current interest rates on home loans?” opens the door to a complex but critical area of personal finance. From the broader strokes of global economic health and central bank policy to the granular details of an individual’s credit score and down payment, myriad factors converge to determine the cost of borrowing for a home.

In a market characterized by constant flux, staying educated is your most potent tool. Regularly monitor economic news, compare offers from multiple lenders, and meticulously evaluate the long-term financial implications of your chosen loan product. Whether you are embarking on the exciting journey of homeownership, considering a refinance, or simply aiming to deepen your understanding of the financial world, a clear grasp of mortgage interest rates empowers you to make decisions that align with your financial goals and secure your future. The dream of homeownership is achievable, and armed with knowledge, you can navigate the path to it with confidence and clarity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.