The seemingly simple question, “What are rates today?” unlocks a vast and complex world of financial dynamics that profoundly influence every aspect of our economic lives. From the price of borrowing money to the return on our savings, from the cost of goods and services to the competitiveness of international trade, various financial rates act as the fundamental levers of the global economy. Understanding these rates — their current levels, the forces driving them, and their multifaceted impacts — is not merely an academic exercise; it is an essential component of prudent personal finance, shrewd investment strategy, and informed business decision-making.

In an ever-evolving economic environment, marked by global events, central bank policies, and market sentiment, rates are rarely static. They are a snapshot, a momentary reflection of underlying economic health and future expectations. This article delves into the current landscape of key financial rates, exploring their significance, their interconnections, and the strategies individuals and businesses can employ to navigate them effectively.

Decoding Interest Rates: The Central Bank’s Influence

At the heart of many financial discussions surrounding “rates” lies the concept of interest rates. These are the costs of borrowing money or the returns earned on lending it, and they are largely dictated by the policies of central banks worldwide.

The Federal Funds Rate and Its Ripple Effect

In the United States, the Federal Reserve’s target for the federal funds rate is perhaps the most pivotal interest rate. This is the rate at which commercial banks lend and borrow their excess reserves from each other overnight. While not directly charged to consumers, changes to this benchmark rate trigger a cascade of effects throughout the financial system. When the Federal Reserve raises this rate, it typically signals a tightening of monetary policy, aiming to curb inflation or cool down an overheating economy. Conversely, a reduction in the rate is often intended to stimulate economic activity.

Today, central banks globally have either been in a hiking cycle to combat persistent inflation or are now holding steady, contemplating the timing of potential cuts. This stance significantly influences all other rates downstream. For consumers and businesses, a higher federal funds rate translates to increased borrowing costs across the board.

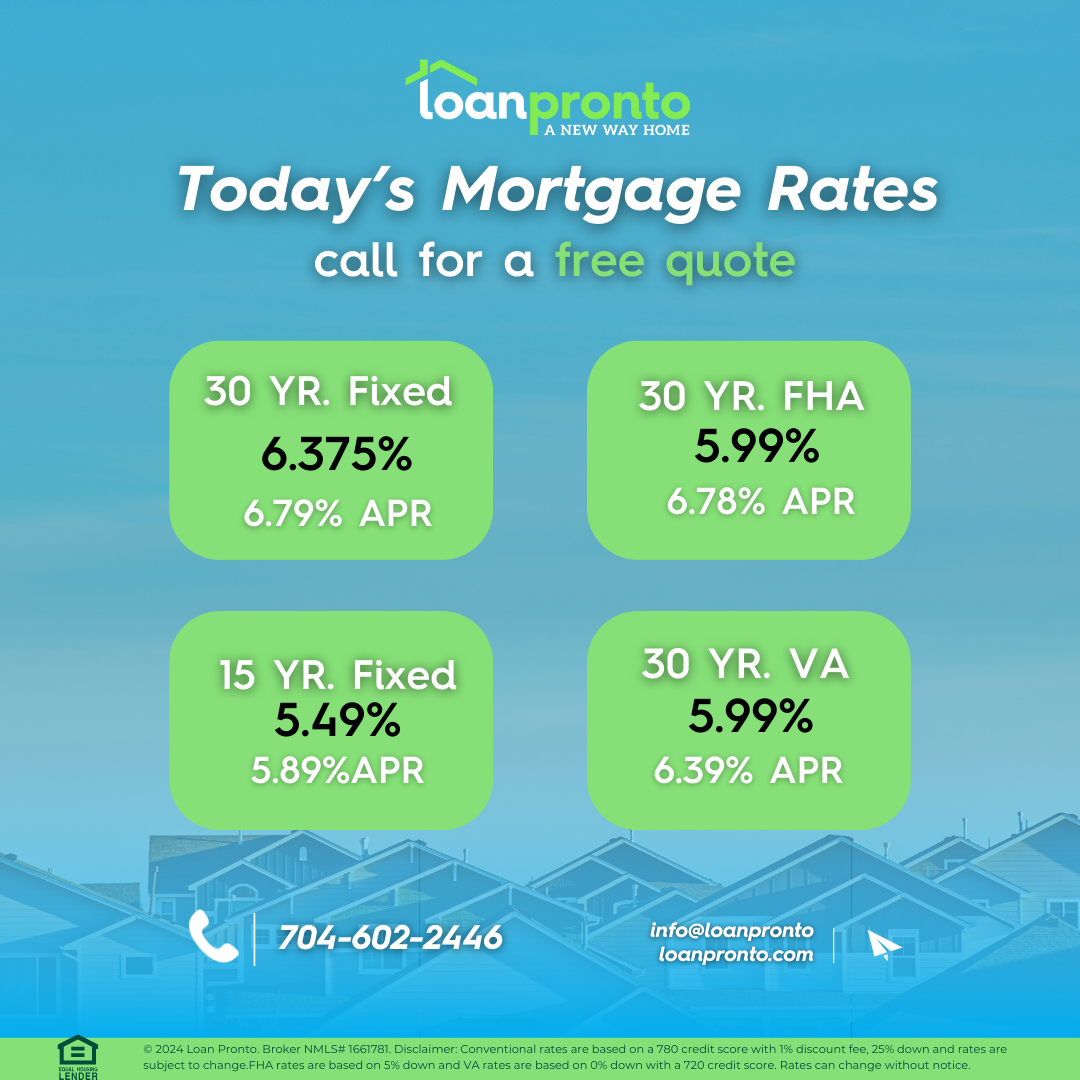

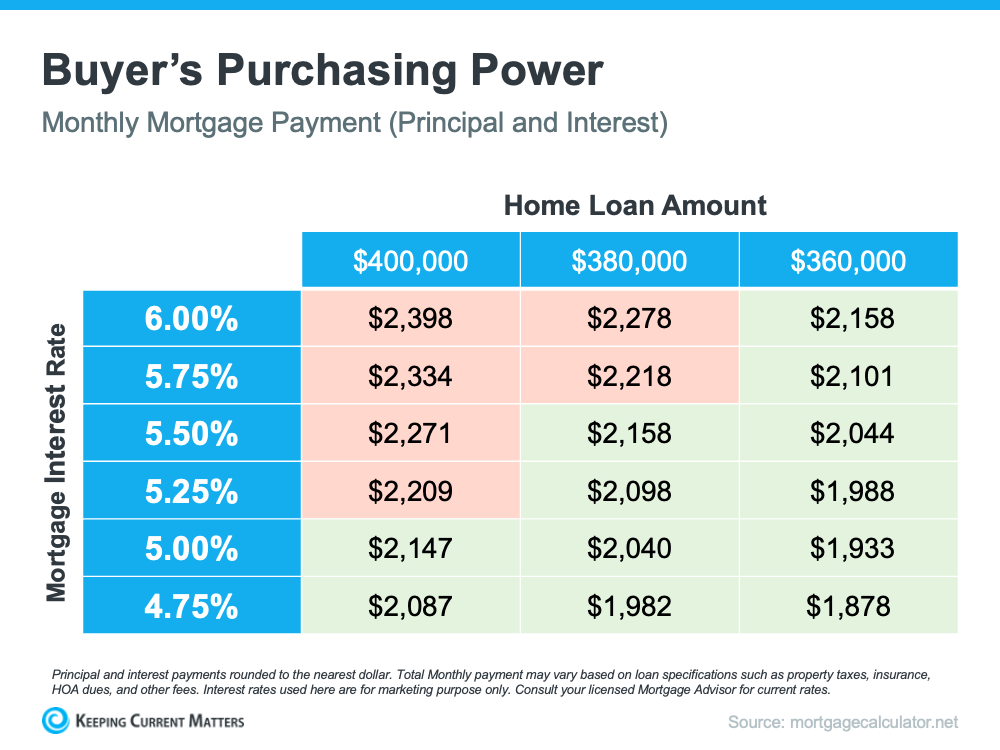

Mortgage Rates: A Cornerstone of Housing Affordability

For most individuals, mortgage rates represent one of the most significant financial rates. These rates, which determine the cost of financing a home purchase or refinancing an existing mortgage, are heavily influenced by the federal funds rate and the bond market, particularly the yield on 10-year Treasury notes. When interest rates rise, mortgage rates generally follow suit, making homeownership more expensive and impacting housing affordability.

Today’s mortgage rates have seen considerable volatility over the past few years. After historic lows, they surged as central banks aggressively raised policy rates. This has led to higher monthly payments for new borrowers and has effectively ‘locked in’ many existing homeowners with lower rates, influencing the supply and demand dynamics in the housing market. Understanding whether current rates favor fixed-rate or adjustable-rate mortgages, or if refinancing is advantageous, is crucial for homeowners and prospective buyers.

Savings Accounts and CDs: The Return on Your Deposits

While borrowers face higher costs, savers often see a silver lining when interest rates rise. Savings account rates and Certificates of Deposit (CD) rates typically move in tandem with broader interest rate trends, albeit with a lag and often at a lower magnitude than lending rates. High-yield savings accounts and CDs have become more attractive in recent periods, offering a more meaningful return on idle cash than in previous low-interest rate environments.

For individuals focused on capital preservation and modest growth, monitoring these rates is essential. The difference between a 0.5% annual percentage yield (APY) and a 4.0% APY on a substantial savings balance can amount to hundreds or thousands of dollars in interest earned annually, making careful selection of banking products vital today.

Loan Rates: Credit Cards, Personal Loans, and Auto Financing

Beyond mortgages, various other consumer and business loan rates are directly tied to the central bank’s policy. Credit card interest rates, often variable, adjust relatively quickly to changes in the federal funds rate. This means that carrying a balance on credit cards becomes significantly more expensive during periods of rising rates. Similarly, personal loan rates and auto loan rates also reflect the prevailing interest rate environment, influencing the cost of financing everything from unexpected expenses to new vehicle purchases. Businesses, too, face higher costs for lines of credit, term loans, and other forms of debt financing. For anyone planning to borrow today, understanding these rates is paramount to managing their debt burden effectively.

Beyond Interest: Other Critical Financial Rates

While interest rates dominate the conversation, several other crucial financial rates play a significant role in shaping our economic reality, from the grocery store aisle to global trade desks.

Inflation Rates: The Erosion of Purchasing Power

The inflation rate measures the pace at which the general level of prices for goods and services is rising, and consequently, the purchasing power of currency is falling. Typically measured by indices like the Consumer Price Index (CPI), inflation is a rate that impacts everyone. When inflation is high, the cost of living increases, and consumers find their money buys less than it did before. Central banks often raise interest rates to combat high inflation, aiming to reduce demand and stabilize prices.

Today, many economies have experienced elevated inflation levels stemming from supply chain disruptions, strong consumer demand, and geopolitical events. While some countries are seeing inflation moderate from its peaks, it often remains above central bank targets, creating a persistent challenge for household budgets and requiring careful financial planning to preserve real wealth.

Exchange Rates: Global Trade and Travel Implications

Exchange rates represent the value of one currency in relation to another. For example, the rate of the US dollar against the Euro tells you how many Euros you can get for one dollar. These rates are constantly fluctuating due to a myriad of factors, including interest rate differentials, economic performance, political stability, and market speculation.

For individuals, exchange rates directly impact the cost of international travel and online shopping from foreign retailers. For businesses, they dictate the cost of imports and the competitiveness of exports, influencing profit margins and strategic decisions about international expansion. A strong domestic currency makes imports cheaper but exports more expensive, while a weaker currency has the opposite effect. Monitoring today’s exchange rates is vital for global businesses and international investors.

Investment Return Rates: Stocks, Bonds, and Alternative Assets

Investors are constantly evaluating investment return rates across various asset classes. This includes the expected returns from stocks, which offer potential capital appreciation and dividends; bonds, which provide fixed or variable interest payments; and alternative assets like real estate, commodities, or private equity. These return rates are not isolated; they are profoundly influenced by the broader interest rate environment, inflation expectations, and economic growth forecasts.

For instance, when interest rates are high, bonds become more attractive relative to stocks, as their fixed payments offer a competitive, lower-risk return. This can lead to a reallocation of capital. Similarly, real estate investment returns are affected by mortgage rates and economic conditions. Understanding current and projected return rates for different asset classes is fundamental to constructing a diversified and resilient investment portfolio today.

The Far-Reaching Impact: Personal Finance and Investment Strategies

The interplay of these various rates has profound implications for personal financial management and investment decision-making. Adapting to the current rate environment requires strategic thinking and proactive adjustments.

For Savers: Maximizing Returns in a Dynamic Environment

In a higher-rate environment, savers have more opportunities to earn significant returns on their cash.

- High-Yield Savings Accounts: Shop around for the best APYs from online banks, which often offer rates significantly higher than traditional brick-and-mortar institutions.

- Certificates of Deposit (CDs): Consider laddering CDs with varying maturities to take advantage of rising rates while maintaining some liquidity.

- Money Market Accounts: These accounts can offer competitive rates and check-writing privileges.

- Short-Term Bonds/Treasury Bills: For those comfortable with slightly more complexity, short-term government bonds can offer attractive, low-risk returns that benefit directly from central bank rate hikes.

The key for savers today is to be proactive and ensure their cash isn’t sitting in accounts earning minimal interest.

For Borrowers: Optimizing Debt Management

Rising rates pose challenges for borrowers, making debt more expensive.

- Prioritize High-Interest Debt: Focus on paying down credit card balances and other high-interest loans first to minimize the impact of compounding interest.

- Consider Fixed-Rate vs. Variable-Rate Debt: For new loans, evaluate the stability of fixed rates against the potential volatility of variable rates. For existing variable-rate debt, explore options to convert to a fixed rate if possible and advantageous.

- Refinancing Opportunities: While general rates may be high, specific refinancing opportunities might arise, particularly for mortgages if individual circumstances or market conditions shift. Regularly review your loan terms.

- Budgeting: Stricter budgeting becomes even more critical to manage increased debt servicing costs without compromising other financial goals.

For Investors: Adapting Portfolios to Rate Swings

Investors must adapt their portfolios to the changing rate environment.

- Fixed Income: High interest rates make new bond issues more attractive. Investors may consider increasing their allocation to bonds, particularly shorter-duration bonds to mitigate interest rate risk, or bond funds.

- Equities: Rising rates can sometimes temper equity valuations, particularly for growth stocks that rely on future earnings discounted at a higher rate. Investors might lean towards value stocks, dividend-paying stocks, or sectors that are less sensitive to interest rate fluctuations.

- Diversification: A well-diversified portfolio across different asset classes, geographies, and sectors remains the best defense against market volatility and uncertainty related to rate changes.

- Inflation Hedges: Consider assets that perform well during inflationary periods, such as real estate (REITs), commodities, or Treasury Inflation-Protected Securities (TIPS).

Business Finance and Economic Considerations

Beyond individual finances, current rates significantly shape the broader business landscape and macroeconomic outlook, influencing corporate strategy, investment, and employment.

Cost of Capital: Corporate Borrowing and Expansion

For businesses, interest rates directly impact their cost of capital. When borrowing rates are high, it becomes more expensive for companies to take out loans for expansion, research and development, inventory management, or mergers and acquisitions. This can lead to a slowdown in corporate investment, as projects that might have been viable at lower interest rates become unprofitable. Small and medium-sized enterprises (SMEs), which often rely more heavily on bank financing, can be particularly sensitive to these changes. Today’s elevated rates force businesses to be more selective with their investments, focusing on projects with higher expected returns.

Consumer Spending and Economic Growth

The cumulative effect of interest rates on personal finance also impacts consumer spending, which is a major driver of economic growth. Higher mortgage payments, more expensive credit card debt, and increased costs for auto loans mean consumers have less disposable income for discretionary spending. This can lead to a slowdown in retail sales, reduced demand for various goods and services, and ultimately, a moderation of economic growth. Central banks often engineer these slowdowns to bring down inflation, but they must balance this with the risk of triggering a recession.

Global Competitiveness and Policy Responses

Exchange rates play a critical role in a nation’s global competitiveness. A stronger domestic currency makes a country’s exports more expensive for foreign buyers and imports cheaper for domestic consumers. This can negatively impact export-oriented businesses but benefit those relying on imported raw materials. Central banks and governments closely monitor these dynamics, sometimes intervening in currency markets or adjusting other economic policies to maintain a favorable balance of trade and support domestic industries. Today, countries with higher interest rates often see their currencies strengthen, attracting foreign investment seeking better returns.

Preparing for Tomorrow: Proactive Financial Planning

Understanding “what are rates today” is just the starting point. The dynamic nature of financial markets necessitates continuous monitoring and proactive planning.

Staying Informed: Key Indicators to Watch

To effectively navigate the rate environment, individuals and businesses should stay informed about key economic indicators. This includes central bank announcements, inflation reports (CPI, PCE), employment data, GDP growth figures, and retail sales numbers. These indicators provide clues about the likely future direction of interest rates and the broader economy. Subscribing to reputable financial news sources and using financial tools to track market data can be invaluable.

Diversification and Risk Management

No matter the prevailing rate environment, diversification remains a cornerstone of sound financial planning. Spreading investments across different asset classes (equities, bonds, real estate, cash equivalents), geographies, and sectors helps to mitigate risk and smooth out returns. For borrowers, diversifying debt (e.g., a mix of fixed and variable rates) can provide flexibility. Risk management also involves having an emergency fund, adequate insurance, and a clear understanding of your financial goals and risk tolerance.

Seeking Professional Guidance

The complexity of financial markets and the nuances of various rates can be overwhelming. Seeking advice from qualified financial planners, investment advisors, or business consultants can provide tailored strategies and insights. Professionals can help assess individual circumstances, optimize portfolios, manage debt, and plan for future financial goals, ensuring decisions are aligned with one’s objectives in the current rate environment.

Conclusion

The question “What are rates today?” opens a window into the dynamic heart of the global economy. From the interest rates set by central banks that influence borrowing and saving costs, to inflation rates that impact purchasing power, and exchange rates that shape international commerce, these figures are not just statistics; they are powerful forces that touch every financial decision we make. By diligently tracking these rates, understanding their implications, and proactively adjusting personal and business financial strategies, we can move from merely observing the financial landscape to confidently navigating it, positioning ourselves for resilience and growth no matter what tomorrow’s rates may bring.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.