In an increasingly complex financial landscape, understanding who you can trust with your money and critical decisions is paramount. This brings us to the concept of fiduciary services – a term often heard but not always fully understood. At its core, fiduciary service represents a sacred trust, a legal and ethical commitment by one party to act solely in the best interests of another. Whether managing personal wealth, overseeing business assets, or navigating the intricate world of estate planning, fiduciaries are held to the highest standards of care, loyalty, and good faith. This article will delve deep into what fiduciary services entail, how they intersect with personal finance and business operations, the transformative role of technology, and why brand and reputation are non-negotiable for anyone operating under this esteemed banner.

The Bedrock of Trust: Defining Fiduciary Services

A fiduciary is an individual or organization that holds a legal or ethical relationship of trust with one or more other parties (referred to as the principal or beneficiary). In this relationship, the fiduciary is entrusted with acting on behalf of the principal, often in matters involving money, property, or legal decisions. The defining characteristic of a fiduciary relationship is the obligation to prioritize the principal’s interests above their own. This isn’t merely a suggestion; it’s a legally binding duty with serious implications for breach of trust.

Core Principles and Responsibilities

The duties of a fiduciary are stringent and multifaceted, designed to protect the principal from potential conflicts of interest or negligence. These core principles include:

- Duty of Loyalty: The fiduciary must act solely in the best interests of the client, avoiding any conflicts of interest. This means no self-dealing, no secret profits, and no prioritizing their own gains over the client’s. If a conflict arises, it must be disclosed, and often, the fiduciary must recuse themselves or obtain explicit consent from the client.

- Duty of Prudence (or Care): Fiduciaries must act with the care, skill, prudence, and diligence that a prudent person acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims. This requires thorough research, informed decision-making, and a deep understanding of the risks and opportunities associated with the client’s situation. For investment fiduciaries, this often translates to diversifying portfolios, monitoring investments, and making decisions based on sound financial principles rather than speculation.

- Duty of Good Faith: This is an overarching principle requiring honesty, integrity, and fair dealing in all interactions. It underpins all other duties, ensuring that the fiduciary’s actions are always transparent and motivated by the client’s welfare.

- Duty to Disclose: Fiduciaries must fully disclose all material facts, including any potential conflicts of interest, fees, and the risks associated with recommendations. Transparency is key to maintaining trust.

- Duty to Avoid Conflicts of Interest: As mentioned under loyalty, fiduciaries must actively identify and avoid situations where their personal interests or those of another client could conflict with the interests of the principal.

- Duty to Impartiality: If acting for multiple beneficiaries (e.g., in a trust), the fiduciary must treat all beneficiaries fairly and impartially, without favoring one over another.

Who Acts as a Fiduciary?

The scope of fiduciary relationships is broad, encompassing various professional roles. Common examples include:

- Financial Advisors/Planners: Many financial professionals operate under a fiduciary standard, particularly those registered with the SEC. They are obligated to recommend investments and strategies that are truly in the client’s best interest, regardless of commissions or other incentives.

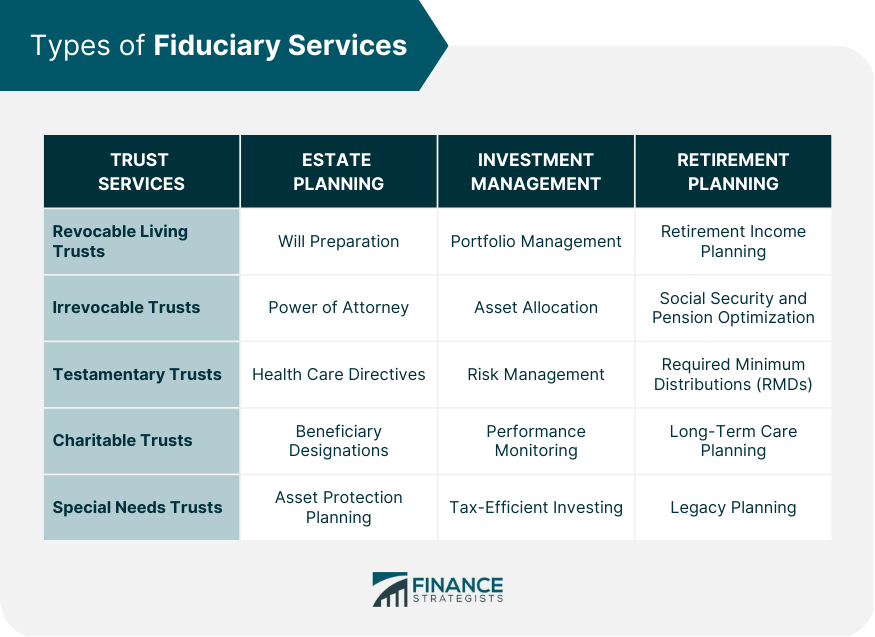

- Trustees: Individuals or entities appointed to manage assets held in a trust for the benefit of designated beneficiaries. They administer the trust according to its terms, making distributions and managing investments prudently.

- Executors: Appointed by a will to manage the estate of a deceased person, pay debts, and distribute assets to heirs.

- Guardians: Legal representatives appointed to make personal and financial decisions for minors or incapacitated adults.

- Corporate Board Members: Directors of a company have a fiduciary duty to the shareholders, requiring them to act in the company’s best long-term interests.

- Pension Fund Managers: Responsible for managing retirement funds on behalf of employees, ensuring the security and growth of those assets.

Understanding these roles underscores the critical responsibility fiduciaries bear and why their services are foundational to stable financial management.

Money Matters: Fiduciary Services in Personal and Business Finance

At its heart, fiduciary service often revolves around the strategic management of money – whether it’s an individual’s life savings or a corporation’s sprawling financial infrastructure. The advice and decisions made by a fiduciary can have profound, long-lasting impacts on financial well-being, making their role indispensable across both personal and business finance spheres.

Navigating Personal Wealth: Investment and Financial Planning

For individuals, fiduciary services are a cornerstone of sound personal finance and investing. Many seek out fiduciary financial advisors because they want assurance that the advice they receive is unbiased and truly tailored to their unique circumstances and goals.

- Investment Management: A fiduciary investment advisor will assess a client’s risk tolerance, financial goals (e.g., retirement, college savings, home purchase), and time horizon. They then construct and manage a diversified investment portfolio designed to achieve these objectives while adhering to the fiduciary duty of prudence. This often involves continuous monitoring, rebalancing, and making adjustments based on market conditions and changes in the client’s life. The emphasis is on long-term growth and preservation of capital, not on generating short-term trading commissions.

- Retirement Planning: Fiduciaries help individuals understand their retirement needs, project future expenses, and develop strategies to save adequately. This includes advising on 401(k)s, IRAs, annuities, and other retirement vehicles, always with the client’s best interest at the forefront.

- Estate Planning: Preparing for the future involves more than just accumulating wealth; it also means ensuring its proper distribution and protection after one’s passing. Fiduciary services in estate planning involve helping clients draft wills, establish trusts, and make arrangements for healthcare directives and powers of attorney. The goal is to minimize taxes, avoid probate, and ensure that assets are distributed according to the client’s wishes, protecting beneficiaries.

- Holistic Financial Planning: Beyond specific investment or estate needs, many fiduciaries offer comprehensive financial planning, integrating budgeting, debt management, insurance needs, and tax planning to create a cohesive strategy for lifelong financial security. This ensures all aspects of a client’s financial life are considered, optimizing outcomes and building resilience.

Safeguarding Business Assets and Succession

Fiduciary duties extend significantly into the realm of business finance, where the stakes can be even higher due to the involvement of multiple stakeholders and complex corporate structures.

- Business Succession Planning: For business owners, planning for succession is crucial. A fiduciary can help structure buy-sell agreements, identify potential successors, and manage the valuation and transfer of ownership. This ensures business continuity, protects the value of the enterprise, and provides for the financial well-being of the departing owner and their family.

- Corporate Governance: Board members, as fiduciaries, are tasked with making decisions that benefit the company and its shareholders. This includes oversight of financial reporting, strategic direction, risk management, and executive compensation, all performed with diligence and loyalty to the corporate entity.

- Managing Employee Benefits: Employers often act as fiduciaries for their employees’ retirement plans (like 401(k)s). They are responsible for prudently selecting and monitoring plan investments, ensuring reasonable fees, and acting in the best interests of the plan participants. Failing to uphold this duty can lead to significant legal and financial penalties.

- Trust Services for Businesses: Businesses might establish trusts for various reasons, such as holding escrow funds, managing charitable contributions, or providing for employee stock ownership plans (ESOPs). Professional corporate trustees act as fiduciaries, administering these trusts according to the specified terms, ensuring compliance, and managing assets responsibly.

In both personal and business contexts, the fiduciary relationship is a safeguard, providing a layer of protection and expertise that is invaluable when making critical financial decisions.

The Tech Revolution: Modernizing Fiduciary Practices

The financial services industry, including fiduciary offerings, is in the midst of a technological transformation. While the core principles of trust and loyalty remain immutable, technology is rapidly reshaping how fiduciary services are delivered, managed, and accessed. From AI-driven insights to robust digital security, tech advancements are not just enhancing efficiency but also expanding the reach and sophistication of fiduciary support.

AI and Automation: Enhancing Efficiency and Insights

Artificial Intelligence (AI) and automation are becoming powerful allies for fiduciaries, enabling them to provide more personalized, efficient, and data-driven services.

- Automated Portfolio Management: Robo-advisors, powered by AI algorithms, can manage diversified portfolios based on client risk profiles and financial goals. While not fully replacing human advisors for complex situations, they offer a low-cost, automated fiduciary solution for many investors, particularly those just starting out.

- Personalized Financial Planning: AI tools can analyze vast amounts of financial data – spending habits, income, assets, liabilities – to generate highly personalized financial plans and recommendations. This allows fiduciaries to identify subtle patterns, predict future needs, and offer proactive advice that would be arduous for a human to process manually.

- Risk Assessment and Fraud Detection: AI algorithms can monitor transactions and client behavior in real-time to identify anomalies indicative of fraud or excessive risk. This enhances the fiduciary’s ability to protect client assets and maintain compliance with regulatory requirements.

- Compliance Monitoring: AI-powered software can automatically scan for potential conflicts of interest, ensure adherence to investment mandates, and flag any activities that might violate fiduciary duties, significantly reducing the administrative burden and human error in compliance.

- Back-Office Automation: Routine tasks such as data entry, report generation, and client onboarding can be automated, freeing up fiduciary professionals to focus on higher-value activities like client consultation and strategic planning. This enhances productivity and allows for a greater focus on the human element of the relationship.

Digital Security and Compliance in a Connected World

With the increased reliance on digital platforms comes the amplified need for robust digital security. Fiduciaries are entrusted with highly sensitive financial and personal information, making them prime targets for cyberattacks.

- Advanced Encryption: Fiduciary firms deploy state-of-the-art encryption technologies to protect client data both in transit and at rest, safeguarding against unauthorized access.

- Multi-Factor Authentication (MFA): Implementing MFA for client portals and internal systems adds a critical layer of security, verifying user identity beyond just a password.

- Cybersecurity Protocols: Comprehensive cybersecurity frameworks, including regular vulnerability assessments, penetration testing, and employee training on phishing prevention, are essential to protect client assets from digital threats.

- Blockchain Technology: While still nascent in widespread adoption, blockchain holds promise for enhancing transparency, security, and immutability of financial records, potentially streamlining compliance and secure asset transfer for fiduciaries in the future.

- Regulatory Technology (RegTech): RegTech solutions leverage AI and machine learning to help fiduciaries navigate the complex and ever-evolving landscape of financial regulations, ensuring continuous compliance with standards like GDPR, CCPA, and specific financial industry rules. This is vital for maintaining the trust and legal standing required of a fiduciary.

Innovative Financial Tools and Client Portals

Technology has also transformed how clients interact with their fiduciaries and access their financial information.

- Client Portals and Dashboards: Secure online portals provide clients with 24/7 access to their investment portfolios, financial plans, performance reports, and important documents. These personalized dashboards offer a clear, consolidated view of their financial standing, enhancing transparency and engagement.

- Mobile Apps: Many fiduciary firms offer dedicated mobile applications, allowing clients to track investments, communicate with their advisors, and receive real-time updates on their financial goals, bringing financial management directly to their fingertips.

- Financial Aggregation Tools: These tools allow fiduciaries and clients to consolidate all financial accounts – bank accounts, credit cards, investments, loans – into a single platform, providing a holistic view of net worth and cash flow, which is crucial for comprehensive financial planning.

- Virtual Collaboration Tools: Video conferencing and secure messaging platforms facilitate seamless communication between fiduciaries and clients, regardless of geographical location, making advice more accessible and timely.

The integration of these technological advancements allows fiduciaries to operate with greater precision, security, and client accessibility, reinforcing their ability to meet the high standards of their duty in the digital age.

Building Trust and Reputation: The Fiduciary’s Brand Imperative

While technology provides the tools and money is the subject, the enduring success of any fiduciary service hinges on an intangible yet supremely powerful asset: trust. Trust is not given; it is earned, nurtured, and meticulously maintained. For fiduciaries, this translates directly into their brand and reputation, which are arguably more critical than in almost any other industry. A strong, trustworthy brand isn’t just about marketing; it’s about the very essence of their business.

The Power of a Transparent Brand Identity

A fiduciary’s brand identity must consistently project reliability, integrity, and competence. It’s the promise they make to their clients, and every aspect of their operation should reinforce that promise.

- Clarity and Simplicity: The brand message should clearly articulate what fiduciary services are offered, the values that guide the firm, and how clients’ interests are prioritized. Jargon should be minimized, and complex concepts explained in an accessible manner.

- Corporate Identity and Design: The visual elements – logo, website design, collateral materials – must convey professionalism and stability. A clean, sophisticated, and user-friendly digital presence, for example, signals a modern, trustworthy entity, especially given the emphasis on financial tools and digital security.

- Ethical Communication: All marketing and communication strategies must be grounded in transparency. Exaggerated claims, misleading statistics, or a lack of clear fee disclosures can quickly erode trust. A fiduciary’s brand should openly communicate their fee structure, potential conflicts, and the legal obligations they operate under.

- Personal Branding for Advisors: For individual financial advisors, personal branding is equally crucial. Their online presence, professional certifications, thought leadership content (e.g., articles on financial trends, investment strategies), and testimonials contribute significantly to their perceived expertise and trustworthiness. This builds a personal connection that reinforces the institutional brand.

Cultivating Reputation Through Ethical Practice

Reputation is the sum of a fiduciary’s actions and behaviors over time. It’s built not just on what they say, but consistently on what they do, particularly when faced with challenges or difficult decisions.

- Consistent Ethical Conduct: Every decision, every recommendation, and every interaction must reflect the fiduciary’s core duties of loyalty and prudence. A single instance of perceived self-interest or negligence can shatter years of trust building. This includes adhering to strict codes of conduct and professional standards, often overseen by regulatory bodies.

- Client Success Stories and Testimonials: While direct endorsements can be regulated in the fiduciary space, anonymized case studies (with client consent) or client satisfaction metrics can effectively illustrate the positive impact of fiduciary services. Showing how a fiduciary has helped clients achieve their financial goals or navigate complex situations builds credibility.

- Proactive Problem Solving: When issues arise, a fiduciary’s reputation is strengthened by their ability to address problems transparently, swiftly, and always with the client’s best interest at heart. This includes clear communication about market downturns, investment performance, or any administrative challenges.

- Industry Leadership and Advocacy: Contributing to public education about financial literacy, advocating for stronger consumer protections, or participating in industry best practices groups can enhance a fiduciary’s reputation as a thought leader and a guardian of ethical standards within the financial sector. This aligns with a broader brand strategy of being a reliable source of information on money and technology trends.

- Digital Footprint Management: In the digital age, a fiduciary’s reputation is also shaped by online reviews, social media engagement, and news coverage. Proactively managing this digital footprint, responding professionally to feedback, and ensuring a positive online narrative are essential for reputation management.

Ultimately, a strong brand for a fiduciary is synonymous with unwavering integrity, clear communication, and a demonstrable commitment to placing clients’ interests first. It is the intangible asset that underpins every financial transaction and strategic decision, allowing clients to confidently entrust their most valuable assets to another’s care.

Choosing the Right Fiduciary: What to Look For

Given the profound impact a fiduciary can have on your financial future, selecting the right one is a decision that demands careful consideration. It’s not just about finding someone knowledgeable, but someone who aligns with your values and whose practice mirrors the high standards outlined above.

First and foremost, always verify that an advisor explicitly states they operate under a fiduciary standard at all times. This is a non-negotiable requirement. Ask about their certifications, such as Certified Financial Planner (CFP®), which often entails a fiduciary oath. Understand their fee structure – whether it’s fee-only (where they are compensated solely by you, minimizing conflicts of interest), fee-based (which might include commissions), or commission-based. While fee-only is often preferred for strict fiduciary assurance, transparency in any compensation model is key.

Leverage technology in your search. Utilize online resources and financial tools to research potential fiduciaries, check their regulatory history (e.g., through FINRA BrokerCheck or the SEC’s IARD system), and read reviews. Pay attention to how they integrate technology into their services – do they offer secure client portals, utilize modern financial planning software, and demonstrate a strong commitment to digital security? This indicates a forward-thinking practice attuned to both efficiency and protection.

Finally, consider their brand and reputation. Look for consistency in their messaging, evidence of long-term client relationships, and a clear demonstration of ethical practice. A fiduciary’s brand should resonate with trust and transparency. Schedule initial consultations with several candidates to assess their communication style, their understanding of your specific needs, and whether you feel a genuine sense of rapport and confidence in their ability to act solely in your best interest. Remember, entrusting your financial well-being to a fiduciary is a long-term relationship built on mutual trust and transparency.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.