Navigating the landscape of significant purchases, be it a new vehicle, a substantial appliance, or even certain financial products, often introduces a labyrinth of additional costs beyond the advertised price. Among these, “dealer fees” stand out as one of the most common and often confusing elements, capable of significantly impacting your total outlay. In an era where financial literacy and savvy consumerism are paramount, understanding what these fees entail, why they exist, and how to approach them is not just beneficial—it’s essential for smart money management. This article will deconstruct dealer fees, exploring their nature, their financial implications, and equipping you with strategies to navigate them effectively, all while considering the evolving roles of technology and brand reputation in today’s marketplace.

Deconstructing Dealer Fees: The ‘Hidden’ Costs of Acquisition

At first glance, a price tag can seem straightforward. However, the moment you engage with a dealership, a new layer of charges often surfaces. These are the dealer fees, and failing to account for them can quickly derail your carefully planned budget.

What Exactly Are Dealer Fees?

Dealer fees, in their essence, are additional charges imposed by a dealership on top of the agreed-upon selling price of an item, most commonly associated with vehicle purchases. They are distinct from government-mandated fees like sales tax, registration, and license plate charges, which are non-negotiable and collected by the state. Instead, dealer fees are charges the dealership levies to cover various operational costs, administrative processes, or simply to boost their profit margins. While some argue they are necessary to maintain business operations, many consumers perceive them as an unnecessary burden or a “hidden” cost. Understanding this distinction is crucial: government fees are statutory; dealer fees are often discretionary and, critically, often negotiable. The proliferation of these fees, sometimes vaguely itemized, has made transparency a key concern for consumers and a differentiator for dealerships.

Common Types of Dealer Fees Explained

The terminology surrounding dealer fees can be diverse and sometimes intentionally opaque. However, a few common types frequently appear on purchase agreements:

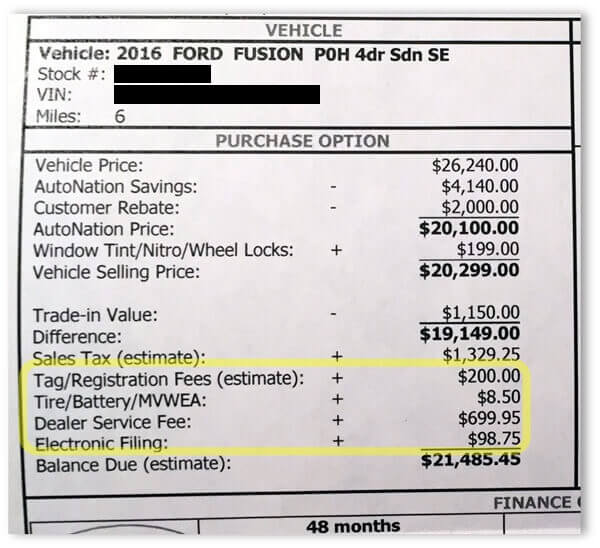

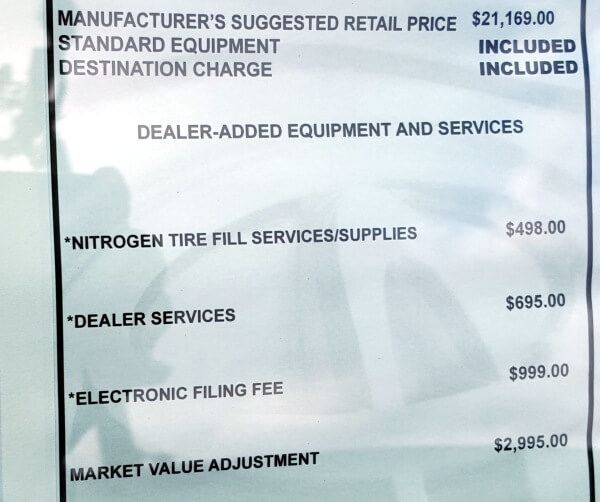

- Documentation Fee (Doc Fee): This is perhaps the most ubiquitous dealer fee. It’s charged to cover the administrative costs associated with preparing and processing all the paperwork for the sale, including sales contracts, financing agreements, and title and registration documents. Doc fees vary significantly by state and even by dealership. While some states cap these fees (e.g., California, New York), others have no limits, leading to charges ranging from under $100 to over $1,000. While a legitimate cost for the dealer, the actual overhead per transaction for paperwork is often much lower than the fee charged, making it a significant profit center.

- Preparation Fee / Dealer Prep Fee: Sometimes distinct from a manufacturer’s “destination fee” (which covers shipping from the factory to the dealership and is usually non-negotiable and included in the MSRP), a dealer prep fee is purportedly for getting the vehicle ready for sale. This might include washing, detailing, removing plastic coverings, and performing a final inspection. While some preparation is necessary, charging an additional fee for this can be questionable, as it’s often considered part of the basic cost of doing business.

- Advertising Fee: This fee is intended to offset the dealership’s advertising and marketing expenses. Dealerships invest heavily in local, regional, and national advertising campaigns to attract customers. Some pass a portion of these costs directly to the consumer through a flat fee per sale. This is a prime example of a fee that often seems arbitrary to the consumer and is highly negotiable.

- Dealer Add-ons / Market Adjustments: These are extra products or services that a dealership might include, or try to include, in the purchase price. Common examples include paint protection, fabric protection, VIN etching, nitrogen-filled tires, extended warranties, security systems, or even simply a “market adjustment” fee due to high demand and low supply. While some of these might have perceived value, they are almost always highly marked up and are, without exception, optional and highly negotiable. These add-ons are often presented as “mandatory” or already installed, but a discerning buyer should always question their necessity and cost.

- Financing Fees: If you opt to finance your purchase through the dealership’s lending partners, you might encounter additional fees related to loan origination, processing, or administration. These can sometimes be rolled into the overall loan amount, increasing your interest payments over time. It’s crucial to compare these against external financing options from banks or credit unions.

Even as technology streamlines many of these processes – with digital signature tools, advanced CRM software managing customer data, and AI-powered chatbots handling initial inquiries – the fundamental concept of these fees has largely persisted. While modern tech might reduce some manual labor, the fees often remain, illustrating their function as a revenue stream rather than a direct reflection of administrative expenditure.

The Financial Impact and Negotiation Strategy

Understanding the various types of dealer fees is merely the first step. The real challenge, and opportunity, lies in comprehending their cumulative financial impact and developing effective strategies to minimize them.

Why Understanding Dealer Fees Matters for Your Wallet

The aggregate sum of various dealer fees can significantly inflate the final “out-the-door” price of a purchase, often by hundreds or even thousands of dollars. An advertised price that seems attractive can quickly become less appealing once these additional charges are factored in. For example, a vehicle listed at $30,000 might easily climb to $32,000 or more with the addition of a $500 doc fee, a $300 advertising fee, and an $800 dealer add-on package. This increase has several critical financial implications:

- Higher Total Cost: Directly increases the amount you pay, diminishing the value of any negotiation on the vehicle’s base price.

- Increased Loan Principal: If you finance the purchase, dealer fees are typically rolled into the loan amount. This means you’ll pay interest on these fees for the entire term of your loan, further increasing your overall cost of ownership.

- Budget Deviation: Unanticipated fees can cause you to exceed your budget, potentially leading to financial strain or requiring you to settle for a less suitable purchase.

- Diminished Equity: Paying unnecessary fees means a larger portion of your initial investment is for non-asset-generating costs, potentially affecting your equity in the item, particularly in the early stages of ownership.

For individuals striving for sound personal finance, every dollar saved is a dollar earned. Being vigilant about dealer fees is a cornerstone of smart budgeting and ensures that your hard-earned money is spent on value, not inflated administrative charges.

Empowering Yourself: Strategies for Negotiating Dealer Fees

Armed with knowledge, you are in a stronger position to negotiate. Effective negotiation isn’t about confrontation; it’s about informed communication and leveraging your position as a valuable customer.

- Research is Key (Tech-Enabled): Before stepping foot into a dealership, use online resources to research average dealer fees in your state or region. Websites like Edmunds, Kelley Blue Book, and various consumer protection forums often provide state-specific information. You can even check review sites for specific dealerships to see if customers complain about excessive fees. Use price comparison apps and tools to get a baseline “out-the-door” price. Remember to maintain digital security while researching; public Wi-Fi can be risky, and using a VPN can protect your privacy when browsing sensitive financial information.

- Ask for an Itemized Breakdown Upfront: Do not wait until you’re in the finance office. Early in the discussion, request a detailed, itemized list of all fees that will be added to the agreed-upon selling price. Insist on seeing the “out-the-door” price clearly stated. This forces transparency and allows you to evaluate the full cost from the beginning.

- Negotiate the “Out-the-Door” Price: Instead of focusing solely on the vehicle’s price or your monthly payment, always negotiate the total “out-the-door” price, which includes the vehicle, all fees, and taxes. This strategy prevents the dealership from lowering the vehicle price only to inflate fees elsewhere.

- Challenge “Mandatory” Fees (Tactfully): While government fees (tax, title, registration) are genuinely non-negotiable, many dealer-imposed fees are. Politely question each fee. Ask what it covers, why it’s necessary, and if it can be removed or reduced. For example, if a “prep fee” is listed, you can point out that preparation is part of their operational cost. For dealer add-ons, simply state you don’t want them.

- Leverage Competition: If you have an offer (including all fees) from another dealership, use it as leverage. Dealerships often compete fiercely, and knowing you’re ready to walk away can prompt them to remove or reduce fees to match a competitor’s total price.

- Don’t Be Afraid to Walk Away: This is your most powerful negotiating tool. If a dealership is unwilling to be transparent, remove excessive fees, or meet your desired “out-the-door” price, be prepared to leave. There are always other dealerships and other options. Many times, a salesperson will find a way to meet your terms once they realize you’re serious about taking your business elsewhere.

- Consider External Financing: Secure pre-approved financing from your bank or credit union before visiting the dealership. This provides a benchmark and allows you to decline any unfavorable financing fees or rates offered by the dealer.

Remember, a dealership’s brand strategy often involves building customer relationships and positive reputation. By demonstrating your preparedness and reasonable expectations, you’re not just a negotiator, you’re a discerning customer whose future business and positive review could benefit their brand.

Navigating the Digital Age of Car Buying: Tech, Transparency, and Brand Trust

The internet has revolutionized the way consumers research, compare, and ultimately purchase goods and services. This transformation extends to high-value items, profoundly impacting how dealer fees are perceived and managed.

Technology’s Role in Unmasking and Managing Dealer Fees

The digital ecosystem offers unprecedented tools for consumers to gain clarity and control over their purchases:

- Online Marketplaces and Aggregators: Platforms like CarGurus, TrueCar, Edmunds, and Kelley Blue Book have become indispensable for vehicle shoppers. These sites allow consumers to compare prices from multiple dealerships, often providing an estimate of the “out-the-door” price (though sometimes excluding all fees, requiring careful verification). They also offer vehicle history reports (e.g., CarFax), consumer reviews, and expert insights, all contributing to a more informed buying decision. Some even provide “guaranteed pricing” that includes specific fees, increasing transparency.

- Dealership Websites and Digital Tools: Increasingly, dealerships are enhancing their online presence to offer a more seamless and transparent buying experience. Many now feature detailed pricing breakdowns on their websites, including some common fees. Online calculators help estimate monthly payments, and some even allow for full online purchases with transparent pricing. Chatbots and AI tools embedded on these sites can provide immediate answers to fee-related questions, although a human follow-up is still advisable for definitive answers.

- Financial Apps and Calculators: A plethora of personal finance apps and online calculators empower consumers to budget meticulously. These tools help estimate total loan costs, factor in interest and fees, and compare different financing scenarios, ensuring that dealer fees don’t disproportionately burden long-term financial health.

- Digital Security and Privacy: While technology offers immense advantages, it also introduces risks. When sharing personal financial information online for loan applications or price quotes, it’s crucial to prioritize digital security. Using secure connections, strong passwords, and being wary of phishing attempts can protect against identity theft and financial fraud. Reputable dealer sites will have robust security measures in place (e.g., HTTPS encryption), which consumers should always verify.

Building Brand Trust and Reputation in a Fee-Conscious Market

In a world where information spreads instantly through social media and online reviews, a dealership’s approach to fees can make or break its brand.

- Dealer Transparency as a Brand Differentiator: Dealerships that proactively provide transparent pricing, including a clear breakdown of all fees, cultivate a stronger sense of trust with consumers. This transparency can become a significant competitive advantage, drawing in customers who are wary of “hidden” costs. A clear, ethical approach to pricing builds a positive brand image and fosters long-term customer loyalty.

- The Impact of Online Reviews and Social Proof: Customer experiences, particularly those involving unexpected or excessive fees, are often shared on review platforms like Yelp, Google Reviews, and dedicated automotive forums. A pattern of complaints about hidden fees can severely damage a dealership’s online reputation, deterring potential buyers. Conversely, dealerships lauded for their fair pricing and transparency often see a boost in their brand equity and business. Marketing and brand strategy must acknowledge that a brand’s reputation is increasingly built on authentic customer experiences, not just advertising.

- Ethical Marketing and Communication: Effective brand communication in the digital age goes beyond flashy ads. It involves clearly explaining the value proposition of any additional services or products and justifying fees with honest explanations, rather than vague statements. Dealers who focus on educating the consumer and offering genuine value, instead of trying to slip in extra charges, are better positioned to succeed in a competitive and informed market. By aligning their marketing messages with their actual sales practices, dealerships can reinforce a trustworthy brand identity.

Conclusion

Dealer fees, while a common component of many significant purchases, should never be accepted without scrutiny. They represent a substantial portion of your overall cost and directly impact your personal finance. By understanding what these fees are, how they affect your wallet, and leveraging modern technology for research and communication, you empower yourself to negotiate effectively.

In an increasingly transparent digital world, dealerships that embrace clarity and fair practices in their fee structures are the ones building enduring brand trust and customer loyalty. As a consumer, your vigilance is your greatest asset. Approach every purchase with an informed perspective, a clear budget, and the confidence to advocate for the best possible financial outcome. Your money works hard for you; ensure it’s not being spent on fees that don’t deliver equivalent value.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.