Car insurance is often viewed as a static monthly bill—a mandatory “tax” on mobility that many consumers pay without a second thought. However, in the realm of personal finance, car insurance represents one of the most flexible and optimizable recurring expenses in a household budget. With inflation impacting premiums and insurance underwriting algorithms becoming increasingly complex, staying loyal to a single provider for decades can often result in what financial experts call a “loyalty penalty.”

Learning how to switch car insurance effectively is more than just a clerical task; it is a sophisticated financial move that can free up hundreds, if not thousands, of dollars in annual cash flow. This guide explores the strategic nuances of transitioning between insurers, ensuring you maintain continuous coverage while maximizing your financial return.

1. The Financial Logic of Switching: Why Timing and Market Analysis Matter

The primary driver for switching car insurance is usually cost, but the underlying financial logic is rooted in market competition and risk assessment. Insurance companies frequently update their rating tiers. A company that was the most affordable for you three years ago may have changed its risk appetite or experienced a surge in claims in your geographic area, leading to price hikes.

When to Re-evaluate Your Premiums

Financial planners generally recommend a “policy audit” every twelve months or whenever a major life event occurs. Significant changes in your life—such as getting married, buying a home, or improving your credit score—can drastically alter your risk profile in the eyes of an underwriter. For instance, if you have recently moved from a high-density urban center to a quiet suburb, your probability of an accident decreases, yet your current insurer may not automatically adjust your rate downward unless you prompt a review or seek a competitor’s quote.

Identifying the “Loyalty Penalty”

It is a paradox of modern finance that new customers are often offered better rates than long-standing policyholders. This is due to customer acquisition strategies where insurers offer aggressive introductory pricing to gain market share. Over time, these rates “creep” upward. By switching, you essentially perform a form of “insurance arbitrage,” moving your business to where the capital requirement is lowest for the same level of protection.

2. Preparing Your Financial Portfolio for a Switch

Before you begin soliciting quotes, you must treat your insurance as a component of your broader financial portfolio. You are not just buying a piece of paper; you are transferring risk. To do this effectively, you need a clear understanding of your current coverage and your actual needs.

Assessing Coverage Needs vs. Budgetary Constraints

The first step is a side-by-side comparison of your current declarations page. You need to identify your limits for bodily injury liability, property damage, and uninsured motorist coverage. From a wealth management perspective, if your net worth has increased since you first took out your policy, you may actually need more coverage (specifically higher liability limits) to protect your assets from potential lawsuits. Conversely, if you are driving an older vehicle that has depreciated significantly, you might consider dropping collision or comprehensive coverage to save on premiums, as the cost of the insurance may outweigh the potential payout.

The Impact of Credit Scores on Insurance Rates

In many jurisdictions, your “insurance-based credit score” plays a pivotal role in the premium you are quoted. Before switching, it is wise to ensure your credit report is accurate. A higher credit score signals financial stability to insurers, often resulting in lower premiums. If you have spent the last year paying down debt or correcting errors on your credit report, you are in a prime position to switch and capture the savings that your improved financial standing entitles you to.

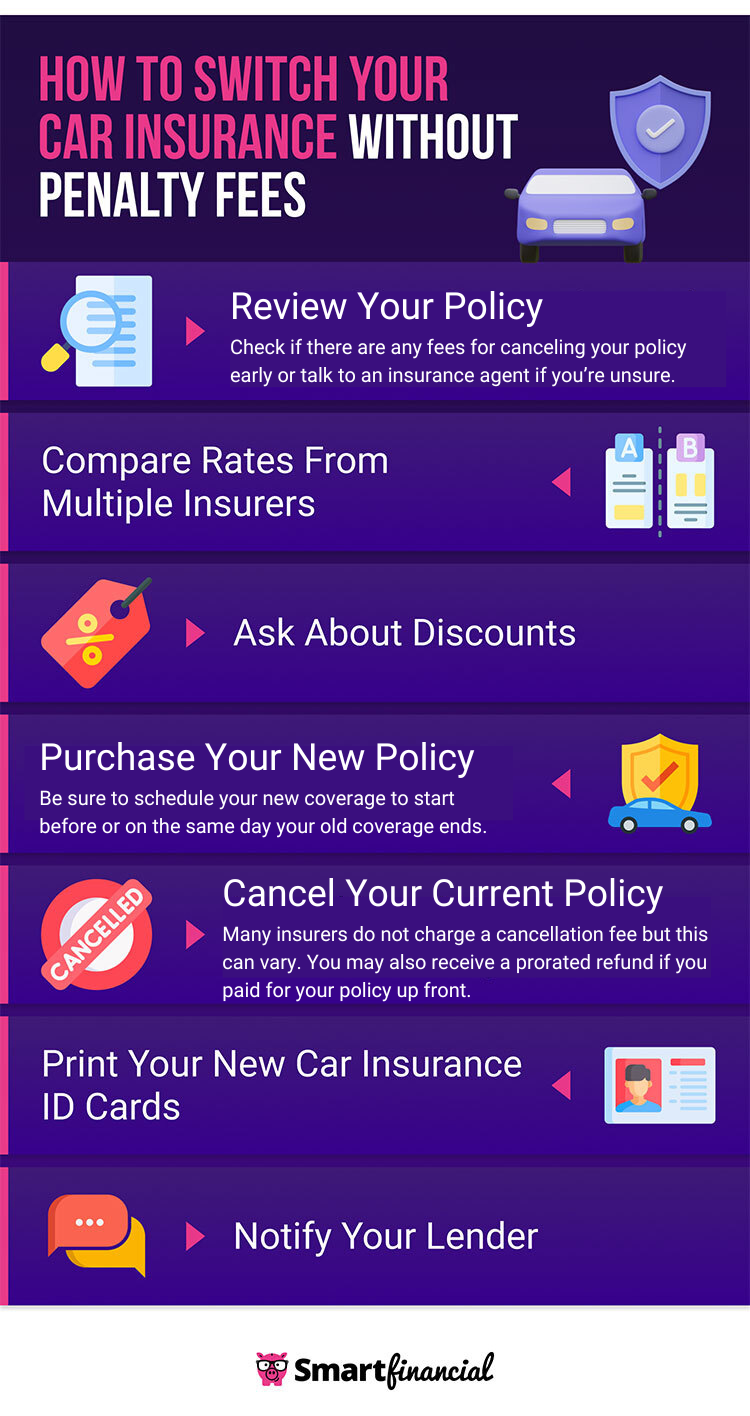

3. The Execution: A Step-by-Step Guide to the Transition

Once you have determined that a switch is financially advantageous, the execution must be precise. Gaps in insurance coverage are not only illegal in most places but can lead to a “high-risk” classification, which will cause your future premiums to skyrocket.

Comparison Shopping and Capturing Multiple Quotes

To get an accurate financial picture, obtain quotes from at least three to five different carriers. Use the exact same coverage limits for each to ensure an apples-to-apples comparison. It is important to look beyond the “big brand” names; regional insurers often have lower overhead and can offer highly competitive rates for specific demographics. During this phase, utilize online comparison tools but be prepared to speak with an agent to see if there are “unlisted” financial incentives, such as discounts for certain professional affiliations or alumni associations.

The Cancellation Process and Avoiding Overlap

The most critical financial step in the transition is the timing of the cancellation. Never cancel your old policy until you have a signed, bound, and funded new policy in hand. Once the new policy is active, contact your old insurer to cancel. Most companies will provide a pro-rated refund for any unused premium you have already paid. This “refund check” can be redirected immediately into your emergency fund or an investment account, turning your insurance switch into a micro-investment event.

4. Maximizing Savings Through Strategic Discounts and Deductibles

The final stage of switching car insurance is fine-tuning the new policy to ensure it offers the best value. This involves leveraging the structural elements of the policy to lower the “total cost of ownership” for your vehicle.

Strategic Use of Higher Deductibles

One of the most effective ways to lower your premium is to increase your deductible. From a personal finance standpoint, if you have a robust emergency fund, you should consider a $1,000 or $1,500 deductible rather than the standard $500. By “self-insuring” the first thousand dollars of a potential claim, you can significantly reduce your monthly fixed costs. The money saved on premiums over a two-year period often exceeds the extra $500 you would have to pay in the event of an accident.

Leveraging Multi-Policy and Professional Discounts

When switching, look for “bundling” opportunities. While the focus here is car insurance, moving your homeowners or renters insurance to the same carrier can trigger a multi-policy discount ranging from 10% to 25%. Additionally, ask about “affinity discounts.” Many insurers offer lower rates to engineers, educators, federal employees, or members of specific credit unions. These are essentially low-risk pools that you can join to benefit from the collective financial stability of that group.

5. Long-Term Financial Management of Insurance Assets

Switching your car insurance is not a one-time event but a recurring strategy for financial health. The insurance market is dynamic, and your personal financial situation is constantly evolving.

By maintaining a disciplined approach to insurance—reviewing your policy annually, understanding the underlying risk factors, and being willing to move your capital to a more efficient provider—you treat your car insurance as a managed asset rather than a sunk cost. This proactive management is a hallmark of sophisticated personal finance. It ensures that you are always protected against catastrophic loss while maintaining the leanest possible operational budget for your household.

In conclusion, switching car insurance is a powerful tool in your financial arsenal. It requires a blend of market research, risk assessment, and precise execution. When done correctly, it reinforces your financial security and optimizes your monthly cash flow, proving that even the most mundane expenses can be leveraged for greater financial freedom.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.