Facing a tax bill you can’t immediately pay can be a daunting experience, often leading to stress and uncertainty. However, the Internal Revenue Service (IRS) understands that taxpayers sometimes encounter financial hardships, and they offer various payment solutions to help individuals and businesses fulfill their tax obligations. Ignoring the IRS or hoping the problem will disappear is never a viable strategy; instead, proactive communication and setting up a structured payment plan are essential steps toward financial recovery and peace of mind. This comprehensive guide will walk you through the process of understanding your options and establishing a payment plan with the IRS, ensuring you navigate this challenge effectively and responsibly.

Understanding Your Tax Obligations and Options

Before delving into the specifics of setting up a payment plan, it’s crucial to understand why you might owe the IRS and the fundamental importance of addressing the issue head-on. A clear understanding of your situation is the first step toward finding the most appropriate solution.

Why You Might Owe the IRS

There are numerous reasons why you might find yourself with an unexpected tax bill. Common culprits include under-withholding from your paycheck throughout the year, underpaying estimated taxes if you’re self-employed or have significant investment income, errors in calculating your tax liability, or unexpected taxable income not accounted for. Sometimes, life events like receiving a large bonus, cashing out investments, or selling property can also lead to a higher tax burden than anticipated. Regardless of the reason, the key is to accurately assess the amount owed and understand that it’s a legitimate government debt.

The Importance of Proactive Communication

Many taxpayers make the mistake of ignoring IRS notices, hoping the problem will simply vanish. This approach is highly detrimental. Ignoring a tax debt will only lead to escalating penalties and interest, making the original amount significantly larger over time. The IRS has robust collection powers, including the ability to levy bank accounts, garnish wages, and place liens on property. By contrast, demonstrating a willingness to work with the IRS by communicating your situation and proposing a payment solution can prevent these severe actions and often results in more favorable terms. Proactive engagement signals responsibility and a commitment to resolving the debt, which the IRS generally views positively.

Overview of IRS Payment Options

The IRS provides several avenues for taxpayers who cannot pay their tax liability in full by the deadline. These options are designed to accommodate different financial situations, from temporary cash flow issues to more severe long-term financial distress. The primary payment plans include Short-Term Payment Plans, Installment Agreements, Offers in Compromise (OIC), and in extreme cases, Currently Not Collectible (CNC) status. Each option has specific eligibility criteria and implications, making it vital to choose the one that best fits your circumstances. Understanding these options is the foundation for successfully setting up a payment plan.

Exploring IRS Payment Plan Solutions

The IRS offers a spectrum of solutions, each tailored to different financial predicaments. Deciding which option is right for you requires an honest assessment of your financial health and a clear understanding of what each plan entails.

Short-Term Payment Plan

If you can pay off your tax liability within 180 days but need a little extra time beyond the original due date, a short-term payment plan might be suitable. While this option provides a temporary reprieve, interest and penalties still apply. It’s an excellent choice for those experiencing a temporary cash flow problem, perhaps waiting for a bonus or a specific asset sale to materialize. You can typically request this plan online through the IRS’s Online Payment Agreement application, by phone, or by responding to an IRS notice.

Offer in Compromise (OIC)

An Offer in Compromise (OIC) allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe. This option is typically considered when a taxpayer’s financial situation makes it unlikely that they will ever be able to pay the full amount due. The IRS considers OICs based on “doubt as to collectibility,” meaning they believe you cannot pay. The process involves a thorough financial investigation by the IRS, requiring significant documentation of your income, expenses, and assets. It’s a complex application, often requiring the assistance of a tax professional, and not all OICs are accepted. If accepted, it can provide significant relief, but it’s crucial to meet all compliance requirements during and after the OIC process.

Installment Agreement (IA)

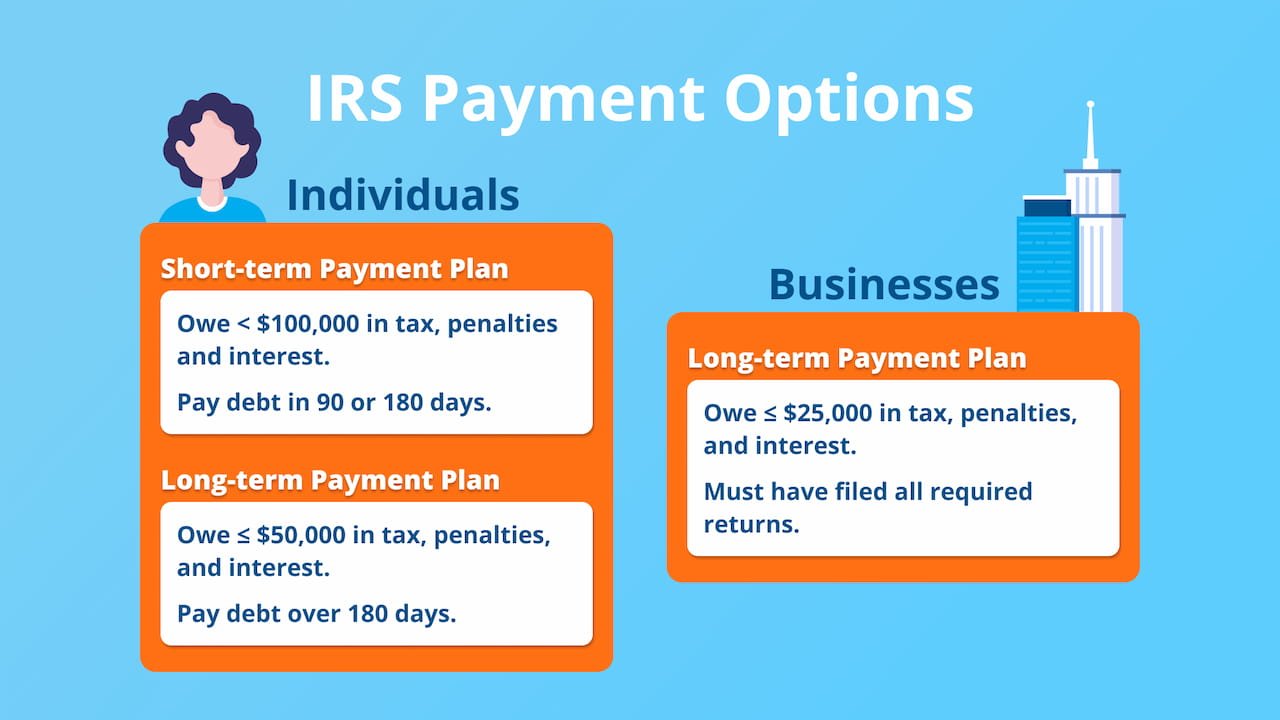

The Installment Agreement is the most common and accessible payment plan for most taxpayers. It allows you to make monthly payments for up to 72 months (six years). While interest and penalties continue to accrue, the penalty for failure to pay is often reduced when you enter into an Installment Agreement.

Streamlined Installment Agreements

For balances below a certain threshold (currently $50,000 for individuals and $25,000 for businesses, including tax, penalties, and interest), you can usually qualify for a streamlined Installment Agreement without needing to provide extensive financial disclosure. This makes the application process relatively simple and quick. You can often apply online and receive immediate approval.

Non-Streamlined Installment Agreements

If your tax liability exceeds the streamlined thresholds, or if the IRS requires further information, you might need a non-streamlined Installment Agreement. This option requires you to provide a detailed financial statement (typically Form 433-F for individuals or Form 433-B for businesses), outlining your income, expenses, and assets. The IRS will review this information to determine your ability to pay and establish an appropriate monthly payment amount.

How to Apply for an Installment Agreement

You can apply for an Installment Agreement in several ways:

- Online: The IRS’s Online Payment Agreement application is the quickest way for many taxpayers, especially for streamlined agreements.

- By Phone: You can call the IRS directly to discuss your options and set up an agreement.

- By Mail: You can submit Form 9465, Installment Agreement Request, along with your tax return or a separate letter to the IRS.

Currently Not Collectible (CNC) Status

In cases of extreme financial hardship, where paying your taxes would leave you unable to meet basic living expenses, the IRS might place your account in “Currently Not Collectible” (CNC) status. This is a temporary measure, meaning the IRS agrees to postpone collection efforts for a period, typically one year, but can be longer if financial hardship persists. During this time, penalties and interest continue to accrue, and the IRS will periodically review your financial situation to see if it has improved. While in CNC status, the statute of limitations for collection continues to run. This option is reserved for truly dire situations and requires comprehensive financial disclosure.

The Application Process: Step-by-Step Guidance

Navigating the application process for an IRS payment plan requires diligence and organization. Following these steps will help ensure a smooth and successful application.

Gather Necessary Documentation

Regardless of the payment plan you’re pursuing, having your financial documents in order is paramount. This includes copies of your filed tax returns, bank statements, pay stubs or other proof of income, a list of all assets and liabilities, and records of essential monthly living expenses (housing, utilities, food, medical, transportation). For Offer in Compromise or non-streamlined Installment Agreements, the IRS will specifically request detailed financial information, often through forms like Form 433-A (Collection Information Statement for Wage Earners and Self-Employed Individuals) or Form 433-F (Collection Information Statement).

Determine Your Ability to Pay

Before approaching the IRS, it’s wise to assess your own ability to pay. The IRS uses specific guidelines for allowable living expenses. By completing forms like 433-F, you can get a clearer picture of what the IRS will consider “reasonable” expenses and thus what your disposable income is for tax payments. This pre-assessment can help you propose a realistic monthly payment amount that the IRS is likely to accept. Be honest and realistic about your income and expenses; attempts to mislead the IRS will only complicate matters.

Choose the Right Payment Plan

Based on your financial assessment and understanding of the various IRS options, choose the payment plan that best suits your situation.

- Short-Term Plan: If you expect to pay in full within 180 days.

- Installment Agreement: If you need more time but can make regular monthly payments. Consider streamlined if you qualify.

- Offer in Compromise: If you genuinely cannot afford to pay the full amount due to long-term financial hardship.

- Currently Not Collectible: If paying would prevent you from meeting basic living necessities.

If unsure, starting with an Installment Agreement request is often a good first step, as it’s the most common and often easiest to secure.

Submitting Your Request

Once you’ve gathered your documents and chosen a plan, submit your request.

- Online: For many Installment Agreements, the IRS Online Payment Agreement application is instant.

- By Phone: Call the IRS at 1-800-829-1040 (individuals) or 1-800-829-4933 (businesses). Have all your information ready.

- By Mail: Complete and mail Form 9465 (Installment Agreement Request) or the relevant OIC forms (Form 656, Offer in Compromise, and Form 433-A (OIC) or Form 433-B (OIC)).

After submission, for more complex agreements like OICs or non-streamlined IAs, an IRS representative may contact you for further information or negotiation.

What to Do While Waiting for Approval

Even while your payment plan request is pending, it’s advisable to continue making payments if you can. This demonstrates good faith to the IRS and can help reduce the amount of interest and penalties accruing. Crucially, ensure you continue to file all future tax returns on time, even if you can’t pay the new tax due. Failure to file on time can jeopardize your payment plan application or an existing agreement.

Maintaining Your Payment Plan and Avoiding Future Issues

Securing a payment plan is a significant step, but maintaining it is equally important. Adhering to the terms of your agreement and implementing strategies to prevent future tax debt are crucial for long-term financial stability.

Adhering to Payment Schedule

Once your payment plan is approved, strictly adhere to the agreed-upon payment schedule. Missing payments can lead to the default of your agreement, reinstating original penalties, potentially increasing interest, and prompting the IRS to resume aggressive collection actions. If you anticipate difficulty making a payment, contact the IRS immediately to discuss your options before missing a payment. They may be willing to temporarily adjust your plan or offer alternatives.

Filing All Future Tax Returns on Time

A fundamental condition for any IRS payment agreement, including Installment Agreements and Offers in Compromise, is that you must file all future tax returns on time. This applies even if you don’t expect to be able to pay the tax you owe for those subsequent years. Failure to file on time is a common reason for a payment plan to be terminated by the IRS.

Paying Future Taxes

Beyond filing on time, you are also required to pay any new tax liabilities in full and on time. This often means adjusting your tax withholding (for employees) or increasing your estimated tax payments (for self-employed individuals and those with other income sources). Proactive tax planning is essential to prevent accumulating new tax debt while you’re still paying off an old one.

Reviewing Your Agreement Periodically

Your financial situation can change. If your income decreases significantly, you might be able to request a lower monthly payment. Conversely, if your income increases, you might be able to pay off your debt faster, reducing the total interest paid. Periodically review your agreement and your finances to ensure the plan remains appropriate for your current circumstances. Contact the IRS to discuss any necessary adjustments.

Seeking Professional Help

For complex tax situations, large tax debts, or if you’re pursuing an Offer in Compromise, consulting a qualified tax professional—such as a Certified Public Accountant (CPA), an Enrolled Agent (EA), or a tax attorney—is highly recommended. These professionals can help you understand your options, prepare necessary documentation, negotiate with the IRS on your behalf, and ensure you comply with all terms. Their expertise can save you time, stress, and potentially a significant amount of money.

Common Pitfalls and Best Practices

Avoiding common mistakes can make the process of setting up and maintaining an IRS payment plan much smoother.

Don’t Ignore IRS Notices

This cannot be stressed enough. Every letter from the IRS requires attention. Ignoring them allows penalties and interest to compound, and collection actions to escalate.

Be Honest and Thorough

When providing financial information to the IRS, ensure all disclosures are accurate and complete. Misrepresenting your financial situation can lead to severe consequences, including criminal charges.

Understand Penalties and Interest

Be aware that interest and penalties continue to accrue on unpaid balances, even with an approved payment plan. While an Installment Agreement may reduce the failure-to-pay penalty rate, interest generally continues until the debt is fully satisfied.

Keep Records of All Communications

Maintain meticulous records of all correspondence with the IRS, including copies of forms submitted, payment confirmations, and notes from phone calls (including date, time, and agent’s name/ID). This documentation is crucial if disputes arise.

Proactive Planning

The best strategy is to prevent tax debt from occurring in the first place. Regularly review your tax withholdings or estimated tax payments, keep accurate financial records, and consult with a tax professional if your income or financial situation changes significantly.

In conclusion, encountering a tax debt you can’t immediately pay is a challenging but manageable situation. The IRS provides clear pathways to resolve these issues through various payment plans. By understanding your options, diligently following the application process, and committing to the terms of your agreement, you can effectively manage your tax liability, mitigate further penalties, and restore your financial stability. Proactive engagement, honesty, and a commitment to compliance are your most powerful tools in navigating the process of setting up a payment plan with the IRS.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.