In the rapidly evolving landscape of financial technology, peer-to-peer (P2P) payment applications have transitioned from luxury conveniences to essential digital tools. At the forefront of this revolution is Venmo, a software powerhouse owned by PayPal that has effectively redefined how individuals interact with digital currency. For the modern user, Venmo is more than just a payment portal; it is a sophisticated social-financial ecosystem built on a framework of seamless user experience (UX) and robust backend security. Understanding how to navigate this application requires a deep dive into its interface, its technical protocols, and the security measures that safeguard every transaction.

Navigating the Venmo Ecosystem: The Tech Stack and User Interface

The brilliance of Venmo lies in its deceptive simplicity. Behind the minimalist interface is a complex software architecture designed to handle millions of concurrent requests without latency. To begin using the platform, a user must first engage with the onboarding technical stack, which involves more than just entering an email address.

Account Setup and Verification Protocols

The initial setup process is a masterclass in streamlined digital onboarding. When a user downloads the Venmo app (available on iOS and Android), the software initiates a series of verification protocols. This includes Know Your Customer (KYC) compliance layers, where the app verifies the user’s identity through mobile phone numbers and email addresses. From a technical standpoint, Venmo utilizes encrypted data transmission to link the app to a user’s traditional banking infrastructure. This is achieved via Plaid or similar API integrations, which allow the app to communicate securely with thousands of financial institutions without the app itself storing sensitive login credentials for your bank.

Understanding the User Interface: The Social Feed vs. The Wallet

Venmo’s UI is unique among P2P apps due to its social-first architecture. The “Social Feed” is a live stream of transactions (with amounts hidden) that uses a proprietary API to display interactions among contacts. For the tech-savvy user, navigating this involves understanding the “Me” tab—the centralized command center of the app. Here, the software displays the “Venmo Balance,” which acts as a digital ledger. Unlike traditional banking apps that reflect a direct pull from a vault, the Venmo wallet is a virtual holding pen that requires specific software triggers to move funds into the legacy banking system.

The Technical Process of Initiating a Transfer

Executing a payment on Venmo is a multi-step software interaction that begins with user discovery and ends with an encrypted transaction confirmation. Every “Send” command triggers a sequence of backend events that ensure the digital assets reach the correct destination.

Searching for Users: QR Codes and Syncing Contacts

To send money, the app must first identify the recipient’s unique digital signature. Venmo offers several methods for this:

- Contact Syncing: The app requests permission to access the mobile device’s contact list via the OS-level API, matching phone numbers against its internal database.

- The Venmo Handle: Each user has a unique alphanumeric string (the @username) which functions as a pointer in Venmo’s database.

- QR Code Integration: Utilizing the device’s camera hardware, Venmo’s scanning software decodes a proprietary QR matrix. This is the most technically secure way to ensure you are sending money to the intended recipient, as it eliminates the risk of “typosquatting” or sending funds to a similarly named account.

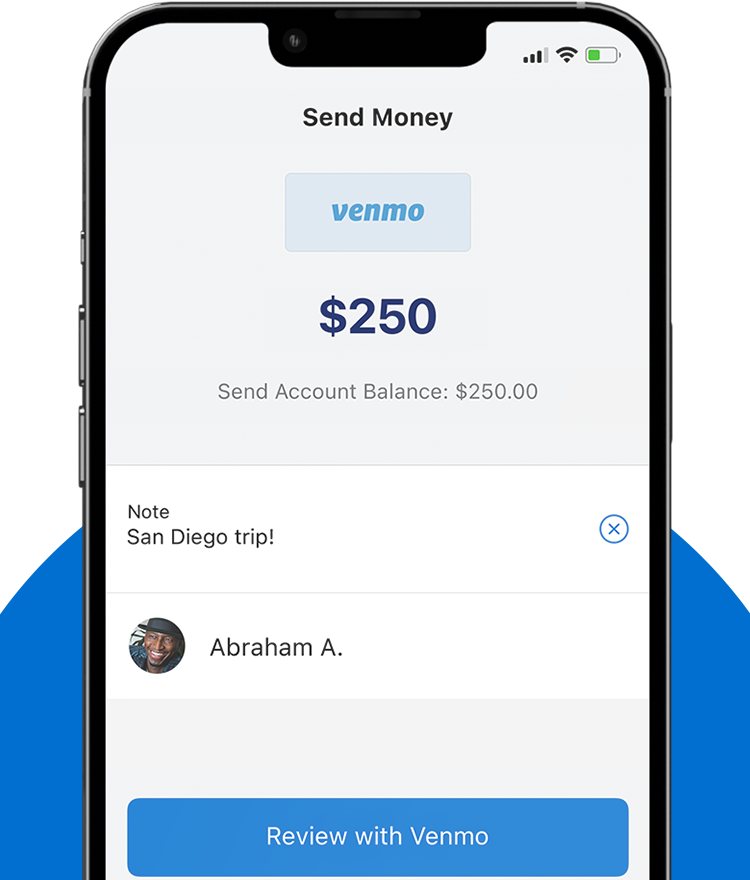

Executing the Payment: Step-by-Step Walkthrough

Once the recipient is identified, the user enters the “Pay or Request” interface. The technical workflow follows this logic:

- Input Validation: The software ensures a numerical value is entered and that a note (text or emoji) is attached. From a data-entry perspective, the note field is mandatory because it serves as a metadata tag for the transaction ledger.

- Source Selection: The user selects the funding source. The app’s logic engine prioritizes the Venmo Balance. If the balance is zero, the software automatically switches to the secondary linked source (Debit Card, Credit Card, or Bank Account).

- The Final Trigger: When the “Pay” button is pressed, the app generates a transaction ID. This is an irreversible command within the Venmo internal database, although the actual movement of funds through the ACH (Automated Clearing House) system may take longer.

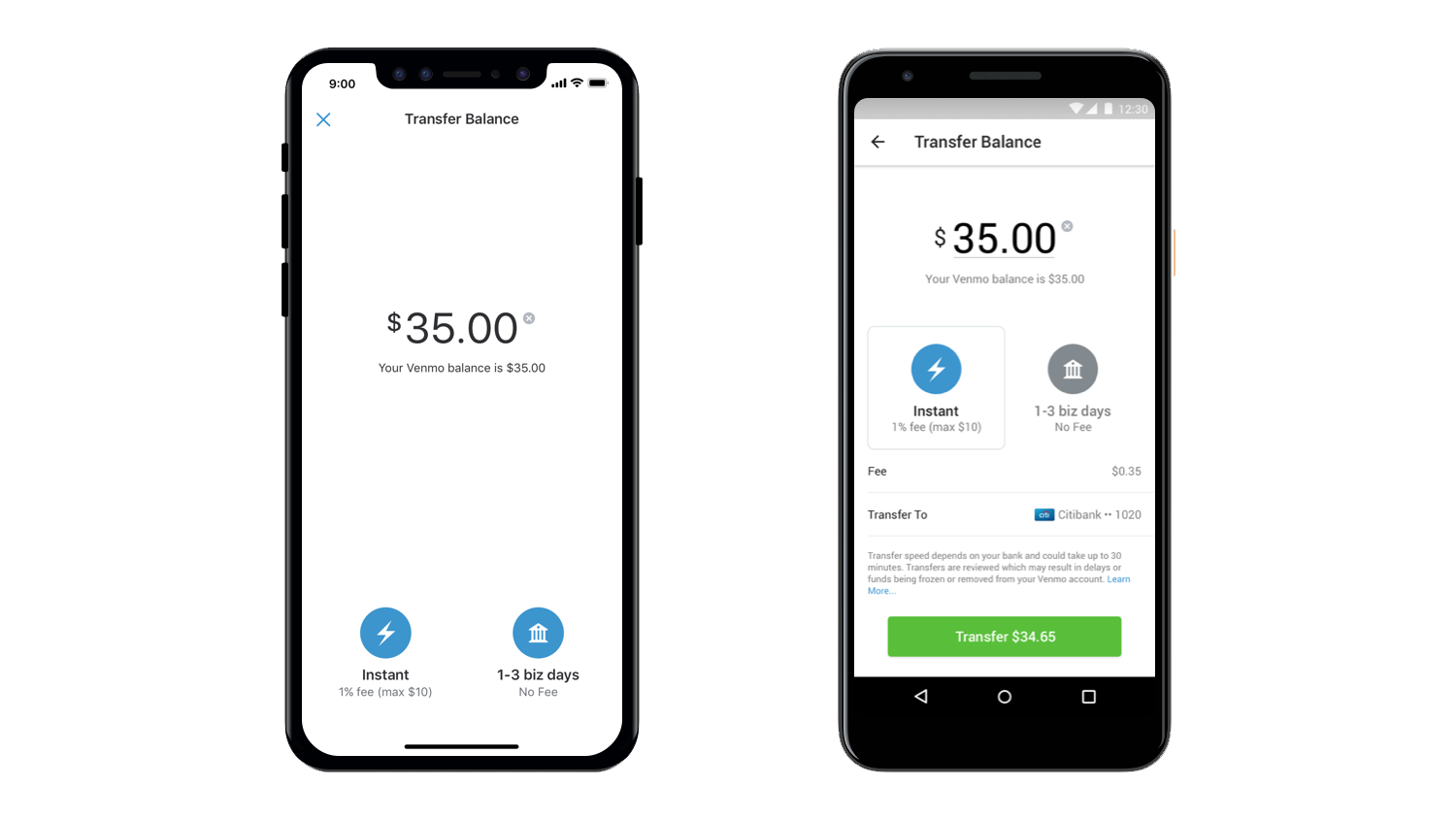

The Backend: How Venmo Processes Instant vs. Standard Transfers

When you send money, Venmo uses different software pathways depending on the chosen speed. A “Standard Transfer” utilizes the legacy ACH network, which is a batch-processing system. However, the “Instant Transfer” feature utilizes the Real-Time Payments (RTP) network or the Visa/Mastercard “Fast Funds” APIs. This allows the software to bypass the 1-3 day waiting period by communicating directly with the recipient’s debit card network to authorize an immediate credit, usually within seconds.

Advanced Software Features and Group Dynamics

Venmo’s utility extends beyond simple one-to-one transfers. The software includes several advanced features designed for group environments and professional workflows.

Utilizing the Split Feature for Collaborative Payments

One of the most technically useful features in the Venmo app is the “Split” function. When a user makes a payment at a merchant or sends a large sum to one individual, the app allows them to trigger a split-request logic. By selecting a previous transaction, the user can choose multiple contacts. The software then calculates the divided amounts—handling the floating-point math to ensure the total equals the original transaction—and sends out individual “Request” pings. This automation reduces the manual friction of calculating and requesting funds individually.

Venmo for Business: Integrating the App into Commercial Workflows

For freelancers and small business owners, Venmo has introduced a “Business Profile” feature. This is a distinct technical layer within the same app. When a user switches to a business profile, the software enables different tax-reporting algorithms and provides a distinct set of analytics. From a tech perspective, business profiles allow for the generation of professional invoices and provide the user with a “verified” badge, which is a cryptographic marker of trust within the network. It also integrates with third-party software via the PayPal/Venmo developer API, allowing businesses to accept Venmo payments on their websites or within other mobile apps.

Digital Security and Data Privacy in P2P Apps

As with any software that handles financial data, security is the paramount concern. Venmo employs a multi-layered defense-in-depth strategy to protect users’ digital assets and personal information.

Multi-Factor Authentication and Biometric Locks

On the client side, Venmo utilizes the security hardware of the smartphone. This includes integration with FaceID, TouchID, and Android Biometrics. By requiring a biometric handshake before the app opens or before a payment is finalized, Venmo adds a layer of physical security that passwords cannot match. Furthermore, the app employs Multi-Factor Authentication (MFA) whenever a login is attempted from an unrecognized device or IP address, sending a time-sensitive TOTP (Time-based One-Time Password) to the registered mobile device.

Privacy Settings: Managing the Visibility of Your Transaction Log

A unique technical aspect of Venmo is its privacy toggle. Every transaction is a data point that can be set to Public, Friends, or Private.

- Public: The transaction is indexed in the global feed.

- Friends: Only users within the sender’s and recipient’s synced contact lists can view the metadata.

- Private: The transaction is only visible to the two parties involved and Venmo’s internal auditors.

From a digital privacy standpoint, tech experts generally recommend the “Private” setting. This prevents “data scraping,” where malicious actors might use public transaction history to map out a user’s social circle or spending habits for social engineering attacks.

Protecting Your Digital Identity from Common Social Engineering Scams

The biggest vulnerability in the Venmo ecosystem isn’t the software itself, but the human element. Scammers often use “phishing” or “smishing” (SMS phishing) to trick users into revealing their MFA codes. Venmo’s software now includes automated warnings when a user attempts to send money to an unverified account or a user not in their contact list. These “friction points” are intentional design choices meant to force the user to pause and verify the recipient’s identity before the cryptographic transfer is finalized.

The Future of Venmo within the Global Tech Ecosystem

As we look toward the future, Venmo is evolving from a simple payment app into a comprehensive digital wallet. The integration of new technologies suggests that Venmo will continue to be a central pillar of the “fintech” world.

Crypto Integration and Blockchain Assets

Venmo has recently integrated a cryptocurrency layer into its software. Users can now buy, sell, and hold assets like Bitcoin and Ethereum directly within the app. This required a massive technical overhaul, linking Venmo’s internal ledger with external blockchain nodes. While the “sending” of crypto between users is handled off-chain within Venmo’s database to save on gas fees, the underlying assets are secured using institutional-grade cold storage solutions.

API Connectivity and Third-Party App Integration

The future of Venmo lies in its “platformization.” Through the “Braintree” payment gateway (a PayPal service), developers can integrate “Pay with Venmo” buttons into third-party apps like Uber, Airbnb, or DoorDash. This creates a seamless software bridge where the user never has to leave the merchant’s app to authorize a payment, using an OAuth-style token exchange to verify the transaction securely.

By understanding the technical nuances of Venmo—from its API-driven user discovery to its multi-layered security protocols—users can move beyond basic functionality and truly master the tool. Venmo is not just a way to send money; it is a sophisticated piece of software that represents the current pinnacle of P2P financial technology. As the app continues to integrate blockchain assets and expand its merchant ecosystem, its role as a primary digital interface for the modern economy will only solidify.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.