In the rapidly evolving landscape of personal finance, the transition from physical currency to digital ecosystems has been nothing short of revolutionary. Among the various tools that have facilitated this shift, Cash App has emerged as a dominant force. Originally launched as a simple peer-to-peer (P2P) payment service, it has expanded into a multi-faceted financial platform. Understanding how to send money via Cash App is no longer just a technical skill; it is a fundamental component of modern financial literacy. This guide explores the mechanics, strategic advantages, and security protocols of using Cash App within your broader financial strategy.

The Evolution of Personal Finance through Digital Wallets

The way we interact with money has shifted from static bank accounts to dynamic, mobile-first interfaces. Peer-to-peer payment systems have bridged the gap between traditional banking and the immediate needs of the modern consumer.

The Rise of Peer-to-Peer (P2P) Systems

The convenience of P2P systems lies in their ability to bypass the friction of traditional wire transfers or the physical limitations of cash. In the past, settling a dinner bill or paying a roommate for utilities required a trip to an ATM or a multi-day bank transfer. Today, digital wallets allow for the instantaneous movement of capital. This velocity of money is a hallmark of the modern economy, enabling individuals to manage their liquidity with unprecedented precision.

Why Cash App Stands Out in the Fintech Landscape

Cash App, developed by Block, Inc., distinguishes itself by offering a suite of services that go beyond simple transfers. While competitors focus primarily on the social aspect of payments, Cash App integrates banking features, stock trading, and cryptocurrency acquisition. For the user, this means that “sending money” is just the entry point into a comprehensive financial ecosystem. Its popularity stems from its accessibility and the $Cashtag system, which provides a layer of privacy and branding to individual financial identities.

Getting Started: Setting Up Your Digital Financial Ecosystem

Before executing your first transaction, it is essential to establish a secure and functional foundation. A well-configured account ensures that your funds remain liquid and your transactions remain uninterrupted.

Linking Bank Accounts and Ensuring Liquidity

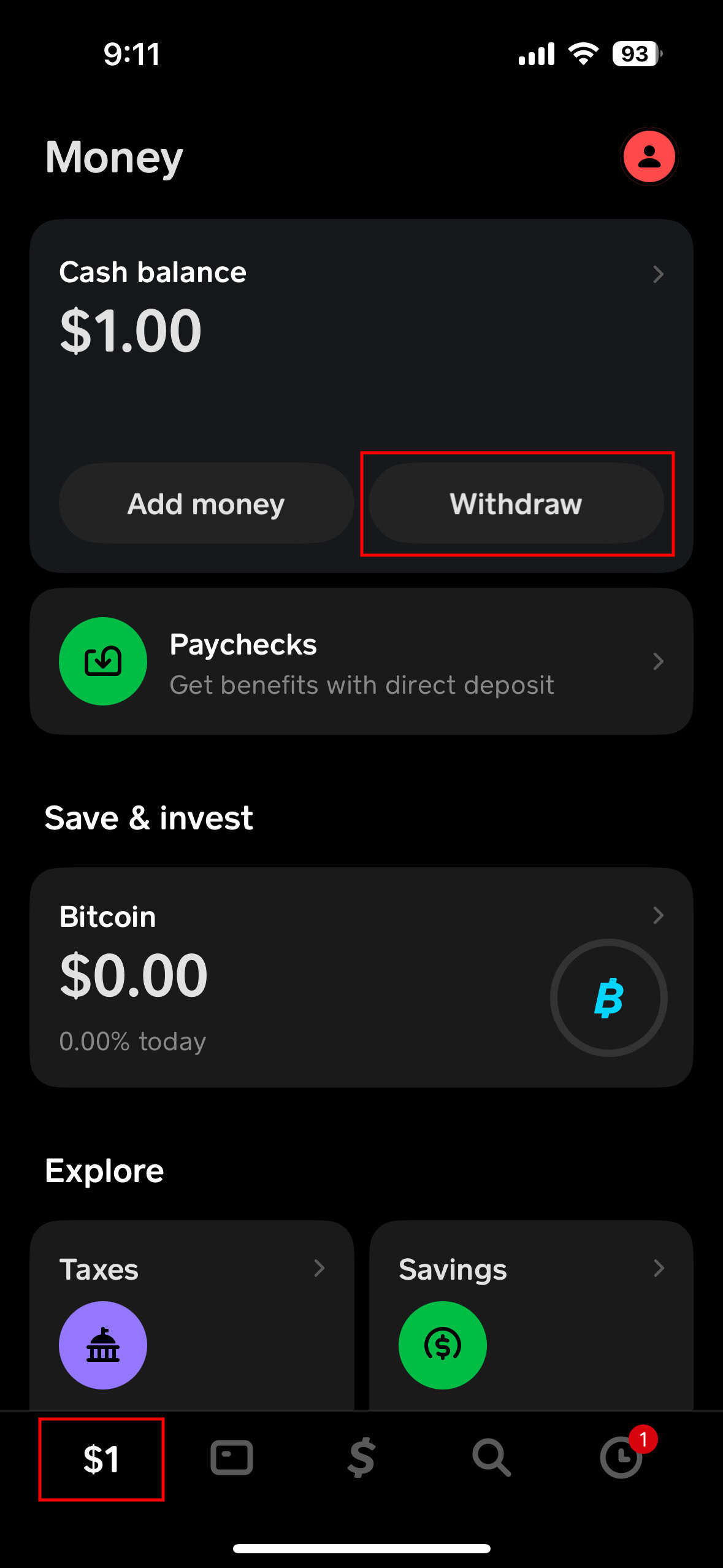

To send money, you must first source the capital. Cash App allows users to link debit cards, credit cards, and traditional bank accounts. From a financial management perspective, linking a debit card is generally preferred, as it avoids the 3% transaction fee associated with credit cards. Furthermore, keeping a balance within the app—known as “Cash Balance”—can act as a secondary checking account, providing a buffer for immediate payments without needing to pull from a primary savings vehicle.

Understanding the $Cashtag and Identity Verification

A unique feature of Cash App is the $Cashtag, a personalized username that allows others to find you without sharing sensitive information like phone numbers or email addresses. However, for a user to move significant amounts of money, identity verification is mandatory. This process involves providing your full legal name, date of birth, and the last four digits of your Social Security number. For those using the app as a primary tool for side hustles or business transactions, this verification is the key to unlocking higher sending and receiving limits, which are essential for scaling personal financial operations.

Executing Transactions: A Step-by-Step Tactical Guide

The primary function of Cash App is the seamless transfer of value. While the interface is designed for simplicity, understanding the nuances of the process can prevent costly errors.

Sending Money: The Core Mechanics

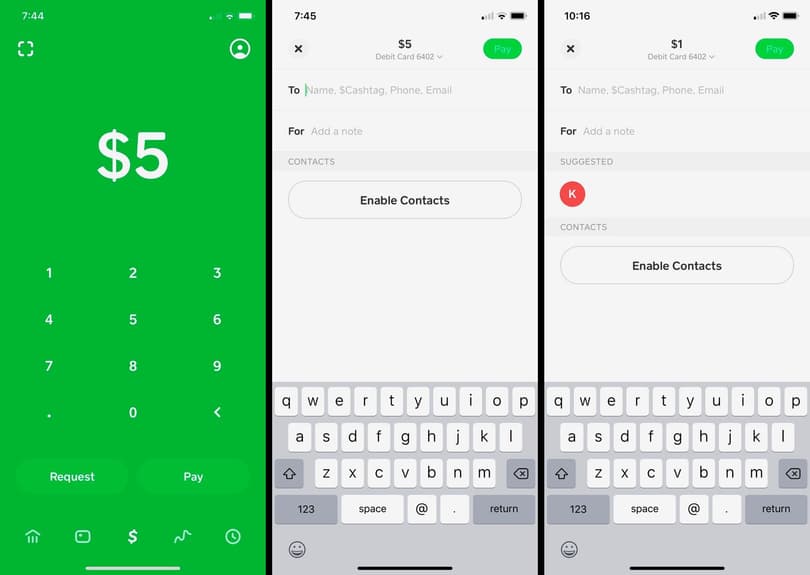

To initiate a payment, the user enters the desired amount on the app’s home screen and selects “Pay.” From there, you must enter the recipient’s $Cashtag, email, or phone number. A critical step often overlooked is the “Note” field. In a professional or organized personal finance context, labeling transactions (e.g., “August Rent” or “Consulting Fee”) is vital for record-keeping and tax preparation. Once you tap “Pay” in the top right corner, the transaction is usually instantaneous.

Requesting Funds and Managing Pending Payments

Financial management is a two-way street. Cash App’s “Request” feature is an effective tool for invoicing or collecting shared expenses. When a request is sent, the recipient receives a notification to approve the transfer. Monitoring the “Activity” tab is crucial here; it provides a real-time ledger of all outgoing and incoming flows. If a payment is marked as “Pending,” it may require additional action from either the sender or receiver—such as an identity check or a manual acceptance of funds from a first-time contact.

Beyond Simple Transfers: Optimizing Cash App for Personal Wealth

For the savvy user, Cash App is more than a way to pay a friend back for coffee. It is a tool that can be optimized to grow and manage wealth.

Utilizing the Cash Card for Daily Budgeting

The “Cash Card” is a customizable Visa debit card linked directly to your Cash App balance. From a financial strategy standpoint, the Cash Card is an excellent tool for “envelope budgeting.” By transferring a specific weekly allowance to your Cash App balance and using only the Cash Card for discretionary spending, you can protect your primary bank account from overspending. Additionally, the “Boosts” feature offers instant discounts at various retailers, providing a small but consistent return on everyday expenses.

Introduction to Micro-Investing and Bitcoin Integration

One of the most powerful features of the platform is the ability to move money directly from your balance into the markets. Users can purchase fractional shares of stocks or exchange-traded funds (ETFs) with as little as $1. This democratizes investing, allowing individuals to practice “dollar-cost averaging” with the leftover funds from their P2P transfers. Similarly, the integrated Bitcoin wallet allows for the purchase, receipt, and sending of cryptocurrency. By treating the app as a gateway to diversified assets, the user transforms a simple payment tool into a wealth-building instrument.

Security and Financial Best Practices in the Digital Age

As with any financial tool, the convenience of digital transfers comes with inherent risks. Safeguarding your capital requires a combination of technical settings and behavioral discipline.

Protecting Your Capital from Fraud and Phishing

Because Cash App transactions are instantaneous and generally irreversible, the platform is a frequent target for bad actors. To mitigate risk, users should enable the “Security Lock” feature, which requires a passcode or biometric ID (FaceID/TouchID) before any money can be sent. Furthermore, it is a cardinal rule of digital finance never to send money to someone promising a “prize” or “flipping” your cash. Treat your $Cashtag with the same level of caution you would treat a physical wallet; only transact with verified individuals or reputable businesses.

Limits, Fees, and Tax Implications of P2P Usage

Understanding the cost of doing business on the app is essential for maintaining a healthy bottom line. While standard deposits to your bank account are free (taking 1–3 days), “Instant Deposits” carry a percentage-based fee. For those using Cash App for a side hustle or business, it is important to stay informed about IRS regulations regarding 1099-K forms. As of current tax laws, receiving payments for goods and services over a certain threshold may be reported to the IRS. Distinguishing between “Personal” and “Business” account types within the app settings is a necessary step for accurate financial reporting and ensuring that your tax liabilities are clearly defined.

In conclusion, mastering the use of Cash App is about more than knowing which buttons to press; it is about integrating a powerful digital tool into a broader strategy of financial efficiency and security. By leveraging its P2P capabilities, utilizing the Cash Card for budgeting, and exploring its investing features, you can take full control of your financial life in the digital era. Whether you are a student managing a budget or an entrepreneur handling micro-transactions, the ability to send and manage money through this platform is a cornerstone of modern personal finance.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.