In an increasingly digitized world, the concept of “cash” has expanded far beyond physical banknotes and coins. Today, sending “cash” often means instantly transferring digital funds between individuals with just a few taps on a smartphone. Venmo, a leading peer-to-peer (P2P) payment application, has revolutionized how millions manage and exchange money in their daily lives. For anyone looking to streamline their personal finances, split bills effortlessly, or simply send money to friends and family with unparalleled convenience, understanding how to effectively use Venmo is no longer a luxury but a fundamental skill.

This guide delves into the mechanics of sending money through Venmo, firmly placing its functionality within the realm of personal finance and financial tools. We will explore its core features, provide a step-by-step walkthrough of the payment process, discuss essential security measures, and illustrate how Venmo can be intelligently integrated into your broader financial strategy. By the end of this article, you will be equipped with the knowledge to navigate Venmo with confidence, ensuring your digital transactions are as smooth, secure, and financially savvy as possible.

Understanding Venmo’s Core Functionality in Personal Finance

Venmo has cemented its position as a ubiquitous financial tool for millions, fundamentally altering how we perceive and conduct small-scale monetary exchanges. At its heart, Venmo is more than just a payment app; it’s a social financial platform designed to make splitting costs and sending money as easy as sending a text message.

What is Venmo and How Does it Work?

Launched in 2009 and later acquired by PayPal, Venmo quickly gained traction for its user-friendly interface and unique social feed, which displays anonymized (or public, depending on user settings) transactions between friends. It operates as a digital wallet, allowing users to send and receive money directly from their Venmo balance, linked bank accounts, debit cards, or credit cards. The premise is simple: you connect your financial institutions to the app, and Venmo acts as an intermediary, facilitating the transfer of funds between users. Instead of fumbling for cash or dealing with inconvenient bank transfers, Venmo enables instant, or near-instant, digital transactions. For personal finance, this means managing small debts, contributing to group expenses, or even paying for services from local vendors becomes remarkably straightforward, eliminating common friction points associated with traditional payment methods.

The Benefits of Using Venmo for Sending Money

The advantages of incorporating Venmo into your personal financial toolkit are numerous and impactful, primarily centering around speed, convenience, and simplified expense management. Firstly, Venmo offers unparalleled speed, with most P2P transfers completing almost instantaneously, allowing for immediate settlement of debts or contributions. This real-time capability is a significant upgrade from conventional bank transfers, which can often take days to process. Secondly, convenience is paramount; all transactions are conducted directly from your smartphone, eliminating the need for physical cash or even a wallet in many scenarios. This makes splitting restaurant bills, sharing utility costs with roommates, or contributing to a collective gift incredibly easy. Furthermore, Venmo provides a clear digital record of all your transactions, which can be invaluable for personal budgeting and tracking expenditures. Instead of relying on memory or disparate receipts, your Venmo history offers a consolidated overview of your digital cash flow, aiding in better financial organization and oversight.

Distinguishing Between “Cash” and Digital Funds on Venmo

It’s crucial for users, particularly those navigating their personal finances, to understand the distinction between physical “cash” and the “digital funds” exchanged via Venmo. When we talk about “sending cash via Venmo,” it doesn’t imply physical currency changes hands. Instead, it refers to the transfer of monetary value that resides digitally within the Venmo ecosystem or is debited directly from a linked financial account. Venmo itself does not handle physical cash. Funds received on Venmo are held in your Venmo balance, which can then be used for future payments within the app, or transferred out to a linked bank account. This digital nature is fundamental to the app’s efficiency, but it also means users should be mindful of their Venmo balance as part of their overall liquid assets, understanding that while readily accessible, it is not physical cash in hand. For sophisticated personal finance management, integrating this digital balance into your budgeting and asset tracking is essential.

Step-by-Step Guide to Sending Money on Venmo

Sending money through Venmo is designed to be intuitive, but a clear understanding of each step ensures a smooth and secure transaction. This section provides a detailed walkthrough, ensuring users can confidently navigate the process from setup to confirmation.

Setting Up Your Venmo Account for Transactions

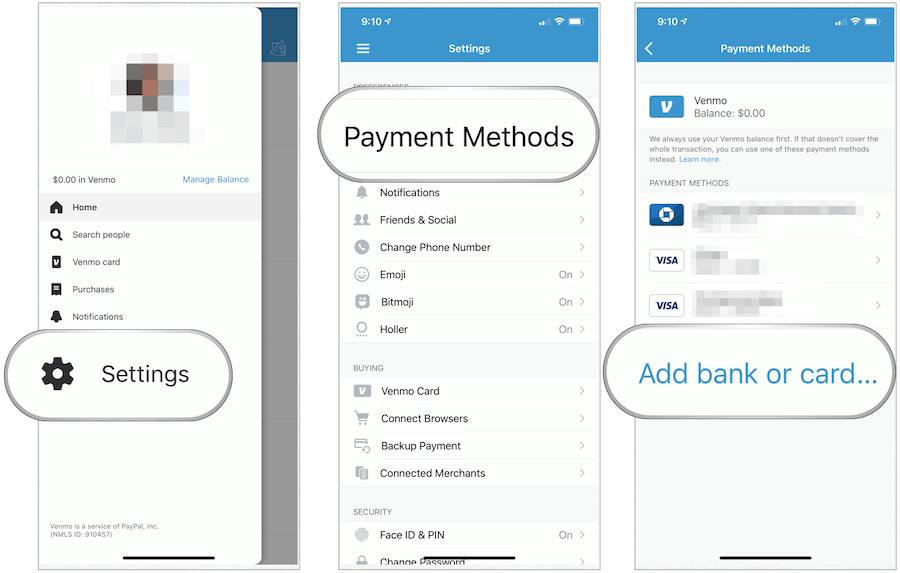

Before you can send any funds, you’ll need a fully functional Venmo account. The first step involves downloading the Venmo app from your smartphone’s app store (available on iOS and Android). Once installed, you’ll proceed with the sign-up process, which typically requires providing your name, email address, and phone number. Venmo adheres to “Know Your Customer” (KYC) regulations, so you’ll also need to verify your identity, often through SMS verification to your phone number and sometimes by linking a bank account.

The critical step for sending money is adding a payment method. Venmo allows you to link a bank account (via instant verification or micro-deposits), a debit card, or a credit card. While linking a bank account or debit card usually incurs no fees for sending money, using a credit card for P2P payments typically incurs a 3% transaction fee, which is an important consideration for your personal finance budgeting. Properly setting up these payment sources ensures that you have the necessary funds available when you initiate a payment and allows Venmo to debit the selected account.

Initiating a Payment: The “Pay or Request” Feature

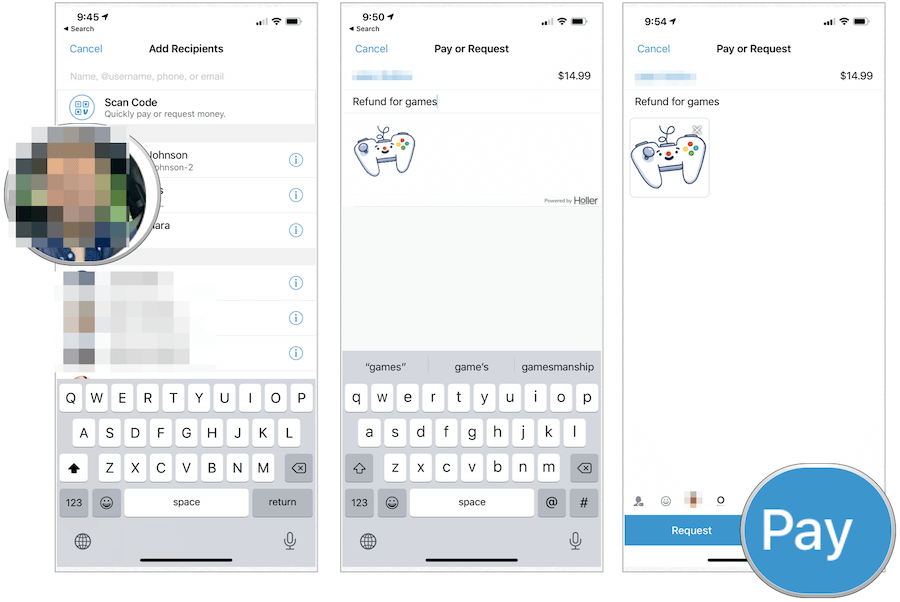

Once your account is set up, sending money is straightforward. Look for the prominent “Pay or Request” button, usually represented by a pencil and paper icon or a dollar sign, at the bottom or top right of the app’s main screen. Tapping this will take you to the payment interface. Here, you’ll need to specify the recipient. You can search for them by their Venmo username, phone number, or email address. If they’re nearby, you might even be able to scan their unique Venmo QR code.

After selecting the recipient, enter the exact amount you wish to send. Below the amount, there’s a crucial field for adding a note or memo. This is where you describe the purpose of the payment (e.g., “Dinner,” “Rent,” “Concert Tickets”). For personal finance tracking and clarity, always include a descriptive note. It serves as a digital paper trail, reminding both you and the recipient of the transaction’s context. Finally, ensure you select the correct payment source from your linked options (Venmo balance, bank account, debit card, or credit card). If you have funds in your Venmo balance, it will typically be the default source.

Confirming and Sending Your Payment

Before finalizing the transaction, Venmo will present you with a review screen. This is your opportunity to double-check all the details: the recipient’s name/username, the amount, the payment note, and the selected payment source. Carefully review this information to prevent errors, as reversing an erroneous Venmo payment to the wrong person can be challenging, if not impossible, especially for P2P transactions.

Pay particular attention to any fees displayed, especially if you are using a credit card, which will incur that 3% sender fee. Once you are satisfied with all the details, tap the “Pay” button. Venmo will then process the transaction. The recipient will receive an instant notification, and the funds will either immediately appear in their Venmo balance or be accessible for transfer to their bank account. The payment will also be recorded in your transaction history, providing an easily accessible record for your personal financial management.

Managing Your Venmo Transactions and Balances

Effective personal finance involves not just sending money, but also proficiently managing received funds and monitoring your transaction history. Venmo offers robust tools to help you keep track of your money within the app.

Receiving and Accepting Funds

When someone sends you money via Venmo, the funds typically appear in your Venmo balance almost instantly. You’ll receive a notification within the app and usually via email or SMS, depending on your notification settings. These received funds become part of your available Venmo balance. Unlike some other platforms, Venmo generally doesn’t require you to “accept” individual payments from friends; they automatically credit your balance.

Once the funds are in your Venmo balance, you have two primary options for their use. You can choose to keep them in your Venmo balance to fund future payments to others through the app. This is convenient for active Venmo users who frequently send and receive money. Alternatively, you can transfer the funds out of your Venmo balance to a linked bank account. Understanding how to manage these received funds is a key aspect of integrating Venmo into your overall personal financial strategy, ensuring your money is where you need it, when you need it.

Transferring Funds from Venmo to Your Bank Account

Moving funds from your Venmo balance to your personal bank account is a common and important step for many users, allowing them to consolidate their money or access it for purposes outside of Venmo. Venmo offers two main transfer options:

- Standard Transfer: This option is free and typically takes 1-3 business days for the funds to arrive in your linked bank account. It’s the most cost-effective choice for those who don’t need immediate access to their funds.

- Instant Transfer: For a small fee (usually 1.75% of the transferred amount, with a minimum fee of $0.25 and a maximum fee of $25.00), you can transfer funds to an eligible debit card or linked bank account within minutes, often within 30 minutes. This is ideal for situations where immediate access to funds is critical, but it’s important to factor the fee into your personal financial calculations.

To initiate a transfer, simply navigate to the “Me” tab, tap “Manage Balance,” and then select “Transfer Money.” You’ll then choose your desired transfer amount, the linked bank account or debit card, and your preferred transfer speed. Be mindful of Venmo’s transfer limits, which can vary based on your account verification status.

Monitoring Your Venmo Activity and History

Keeping a close eye on your Venmo activity is crucial for sound personal financial management. The app provides a comprehensive transaction history within the “Me” tab. Here, you can view all your past payments sent and received, along with their associated notes, dates, and amounts.

This detailed history serves multiple purposes:

- Budgeting and Expense Tracking: You can easily review how much you’ve spent and received over time, helping you categorize expenses and stick to your budget. The notes you add to payments become particularly useful here.

- Reconciliation: It allows you to reconcile your Venmo transactions with your bank statements or other financial records, ensuring accuracy and identifying any discrepancies.

- Dispute Resolution: While rare for P2P payments, having a clear record of transactions can be helpful if there’s ever a dispute or misunderstanding with another user.

Additionally, Venmo offers privacy settings for your transactions. You can choose for payments to be public, visible to friends, or entirely private. For personal finance and privacy, setting most transactions to “private” is often the recommended default, especially for sensitive financial exchanges.

Security Best Practices and Common Pitfalls

While Venmo offers immense convenience, leveraging it responsibly requires a diligent approach to security and an awareness of its limitations. Protecting your digital funds is as important as safeguarding physical cash.

Protecting Your Venmo Account and Funds

The first line of defense for your Venmo account is a strong, unique password. Avoid easily guessable combinations and consider using a password manager. Beyond a strong password, enable Two-Factor Authentication (2FA) immediately. This adds an extra layer of security, requiring a code sent to your phone or email in addition to your password when logging in from a new device. This significantly reduces the risk of unauthorized access.

Be constantly vigilant against phishing scams. These often involve deceptive emails or messages impersonating Venmo, attempting to trick you into revealing your login credentials or personal financial information. Always verify the sender and URL before clicking links or entering data. Only link bank accounts or debit cards that you trust and actively monitor. If you lose your phone or suspect unauthorized activity, immediately log out of all devices and change your password, then contact Venmo support. Treating your Venmo account with the same security protocols as your bank account is paramount for protecting your personal finances.

Understanding Venmo’s Purchase Protection and Limitations

A critical aspect of Venmo’s functionality, especially for those who use it beyond just friends and family, is its purchase protection policy. Venmo offers limited purchase protection primarily for eligible business profiles and certain authorized merchants when the “goods and services” payment type is selected. This protection typically covers items that are not received, are significantly not as described, or are fraudulent.

However, a crucial caveat for personal finance users is that most standard peer-to-peer (P2P) payments between friends and family are NOT covered by Venmo’s Purchase Protection. This means that if you send money to a friend for an item and they fail to deliver, or if you accidentally send money to the wrong person, it can be extremely difficult to recover those funds. Venmo explicitly advises sending money only to people you know and trust. For transactions involving goods or services with acquaintances or strangers, it is advisable to use the “goods and services” toggle (which incurs a fee, typically paid by the seller) or consider alternative payment methods that offer more robust buyer protection, such as PayPal’s broader coverage or credit card payments. This distinction is vital for minimizing financial risk.

Troubleshooting Common Venmo Issues

Even with careful use, you might occasionally encounter issues with Venmo. Common problems include failed payments, funds not appearing, or concerns about unauthorized transactions.

- Failed Payments: If a payment fails, first check your linked payment method. Is there sufficient balance? Has the card expired? Is your bank experiencing issues? Sometimes, a temporary app glitch can be resolved by restarting the app or your device.

- Disputed Transactions: While rare for P2P transactions to be formally disputed and reversed by Venmo, if you accidentally send money to the wrong person, your best first step is to politely request the recipient to send the money back. If they refuse or you can’t reach them, contact Venmo Support immediately. They might be able to mediate, but success is not guaranteed without purchase protection.

- Unauthorized Activity: If you notice transactions you didn’t make, promptly report them to Venmo support. They can investigate and guide you through the process of securing your account and potentially recovering funds if fraud is confirmed.

Venmo’s support center, accessible through the app or their website, provides FAQs and direct contact options (email, chat, phone). Proactive communication and prompt action are key to resolving financial issues efficiently.

Integrating Venmo into Your Personal Financial Strategy

Beyond its transactional utility, Venmo can be a powerful tool for enhancing specific aspects of your personal financial management, from budgeting to strategic payment choices.

Venmo for Budgeting and Expense Splitting

Venmo excels at simplifying shared expenses, making it an invaluable asset for those who frequently split costs with friends, family, or roommates. Whether it’s dividing a restaurant bill, collecting contributions for a group gift, or managing monthly household utilities, Venmo streamlines these often-cumbersome financial interactions. By using descriptive notes for each payment, you can easily categorize and track your shared spending within the app’s transaction history. This makes it simpler to reconcile accounts at the end of the month, ensuring everyone pays their fair share and eliminating awkward cash exchanges or IOUs. For those employing budgeting apps or spreadsheets, Venmo’s digital records can be easily exported or manually logged, providing clear insights into a significant portion of social spending and shared financial obligations, thereby supporting more accurate budget adherence.

When to Use Venmo vs. Other Payment Methods

Choosing the right payment method for different financial situations is a hallmark of intelligent personal finance. Venmo is ideally suited for informal, relatively small-value, domestic peer-to-peer payments where trust between parties is high. It’s perfect for repaying a friend for coffee, splitting a taxi fare, or contributing to a casual group activity.

However, there are scenarios where other methods are more appropriate:

- Large-Value Transfers: For significant sums, especially those involving property or major assets, traditional bank transfers, wire transfers, or certified checks often provide more robust security, tracking, and legal recourse.

- International Transfers: Venmo is currently limited to the United States. For sending money internationally, services like Wise (formerly TransferWise), Xoom, or traditional wire transfers are necessary.

- Business Transactions with Unknown Parties: For purchasing goods or services from individuals you don’t know well, or for larger business-to-consumer transactions, credit cards or PayPal (using its buyer protection features) offer stronger consumer protections against fraud or non-delivery.

- Anonymity: If anonymity is desired, cash remains the only truly untraceable method.

Understanding these distinctions helps you leverage Venmo for its strengths while relying on other financial tools when their features align better with your specific financial needs and risk tolerance.

The Future of Digital Cash and P2P Payments

The evolution of Venmo is indicative of a broader trend towards a cashless society and the increasing integration of digital tools into everyday financial management. As technology advances, P2P payment platforms are continually enhancing their features, moving beyond simple transfers to offer budgeting tools, investment options, and deeper integration with other financial services. Venmo itself has introduced features like a debit card, credit card, and the ability to buy/sell cryptocurrency, further solidifying its role as a multifaceted financial platform.

The future will likely see even greater emphasis on security, instantaneity, and interoperability between various digital payment systems. For individuals, this means having access to an ever-growing suite of tools to manage their money more efficiently, track spending with greater precision, and engage in financial transactions with unprecedented ease. Embracing platforms like Venmo, while understanding their nuances and limitations, is a vital step in navigating this evolving landscape and maintaining control over your personal finances in the digital age.

Conclusion

Sending money via Venmo has become an indispensable aspect of modern personal finance, offering a blend of speed, convenience, and social connectivity that traditional methods simply cannot match. From setting up your account and initiating payments to wisely managing your digital balance, Venmo empowers users to handle everyday financial transactions with remarkable ease.

However, true mastery of this financial tool extends beyond mere functionality. It encompasses a disciplined approach to security, a clear understanding of its purchase protection limitations, and the strategic integration of Venmo into your broader financial strategy. By prioritizing strong passwords, enabling two-factor authentication, using descriptive payment notes for budgeting, and discerning when to use Venmo versus other payment methods, you can harness its full potential while safeguarding your financial well-being.

As the digital frontier of personal finance continues to expand, platforms like Venmo will play an increasingly central role. By becoming proficient in its use, you’re not just learning “how to send cash via Venmo”; you’re actively embracing a smarter, more efficient way to manage your money in the 21st century.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.