Securing a business loan is often a pivotal step for entrepreneurs and established companies looking to grow, manage cash flow, or invest in new opportunities. Whether you’re launching a startup, expanding operations, purchasing equipment, or navigating a challenging economic climate, external funding can provide the necessary capital injection. However, the process of qualifying for a business loan can seem daunting, with lenders scrutinizing various aspects of your business and personal financial history. It’s not simply about asking for money; it’s about demonstrating your ability to repay it, showcasing the viability of your business, and presenting a compelling case for investment.

This guide will demystify the qualification process, outlining the critical criteria lenders evaluate, the essential documentation required, and strategic steps you can take to significantly enhance your chances of approval. By understanding the lender’s perspective and meticulously preparing your application, you can navigate the journey to securing the capital your business needs to thrive.

Understanding Lender Expectations: The Core C’s of Credit

Lenders, regardless of their size or type, typically employ a systematic approach to assess loan applicants. This framework is often summarized by the “Five C’s of Credit”: Character, Capacity, Capital, Collateral, and Conditions. Mastering these areas is fundamental to presenting a strong loan application.

Character: The Borrower’s Reputation and Experience

“Character” refers to the trustworthiness and integrity of the business owner and key management team. Lenders want to feel confident that you are reliable and committed to repaying the loan.

- Personal Credit Score: This is often the first thing a lender will examine, especially for small businesses or startups. A strong personal credit score (generally FICO 680+) demonstrates a history of responsible financial management. Late payments, defaults, or excessive debt on your personal credit can significantly hinder your chances, as lenders view the business owner’s financial discipline as a proxy for the business’s.

- Business Credit Score: Once your business has established its own credit history (e.g., D&B PAYDEX score, Experian Intelliscore), lenders will scrutinize this as well. A robust business credit profile built on timely payments to suppliers and vendors reflects financial stability.

- Industry Experience and Management Team: Lenders assess the experience and expertise of the management team. Do you and your key personnel have a proven track record in the industry? A strong management team with relevant experience increases confidence in the business’s ability to execute its plan and adapt to challenges.

- Business History: The length of time your business has been operational can also play a role. Established businesses with several years of consistent performance often have an advantage over very new ventures.

Capacity: Ability to Repay the Loan

Perhaps the most crucial C, “Capacity” evaluates your business’s ability to generate sufficient cash flow to comfortably cover loan repayments. Lenders want objective evidence that your business can meet its financial obligations without undue strain.

- Cash Flow Analysis: Lenders will meticulously review your cash flow statements to understand how much money is coming in and going out of your business. Positive, consistent cash flow is a strong indicator of repayment capacity. They often look at Debt Service Coverage Ratio (DSCR), which compares the cash flow available to pay current debt obligations. A DSCR of 1.25 or higher is generally considered good.

- Profitability: Your business’s net profit margins are a key indicator of its financial health. Consistent profitability over several years demonstrates a sustainable business model.

- Debt-to-Income Ratio (or Debt-to-Equity Ratio for businesses): This ratio helps lenders understand how much debt your business is already carrying relative to its income or equity. A high existing debt burden can signal a higher risk.

- Historical Financial Performance: Lenders will analyze several years of financial statements (typically 2-3 years) to identify trends, stability, and growth patterns. They’re looking for consistency and positive momentum.

Capital: Your Investment in the Business

“Capital” refers to the financial stake you and your partners have personally invested in the business. Lenders want to see that you have “skin in the game,” demonstrating your commitment and reducing the lender’s risk.

- Owner’s Equity: The amount of capital contributed by the owners or shareholders. A significant owner’s equity shows belief in the business’s future and provides a buffer against losses.

- Personal Investment: For startups or small businesses, lenders often look at the personal funds owners have put into the business. This can include personal savings, investments, or even personal assets used to secure a loan. The higher your personal stake, the more invested you are in the business’s success, aligning your interests with the lender’s.

Collateral: Assets to Secure the Loan

“Collateral” consists of assets that can be pledged to secure the loan. If your business defaults on the loan, the lender has the right to seize and sell these assets to recover their funds.

- Types of Collateral: Common forms of business collateral include real estate (commercial property), equipment, inventory, accounts receivable, and even intellectual property. For smaller loans or startups, personal assets like homes or marketable securities may be required as collateral, especially if business assets are insufficient.

- Asset Valuation: Lenders will assess the fair market value of any pledged collateral to ensure it adequately covers the loan amount. They typically lend a percentage of the collateral’s value, known as the loan-to-value (LTV) ratio.

- Importance: While not always strictly necessary for every loan type (e.g., some unsecured lines of credit), providing solid collateral significantly lowers the lender’s risk and can lead to more favorable loan terms and higher approval chances, especially for larger loan amounts.

Conditions: Economic and Industry Factors

“Conditions” refer to the external factors that could impact your business’s ability to repay the loan. These are often outside of your direct control but are crucial for lenders to assess risk.

- Economic Climate: General economic trends, such as inflation, interest rates, and consumer spending, can affect your business’s performance. Lenders will consider the broader economic outlook when evaluating your application.

- Industry Outlook: The health and future prospects of your specific industry are also critical. Is your industry growing, stable, or declining? Is it highly competitive? A favorable industry outlook enhances your business’s potential for success.

- Purpose of the Loan: Lenders want to know precisely how you intend to use the loan funds. Is it for expansion, working capital, equipment purchase, or debt consolidation? A clear, well-justified purpose that aligns with business growth or stability will be viewed more favorably.

- Competitive Landscape: Understanding your competitive environment and your business’s unique selling proposition helps lenders assess market viability and sustainability.

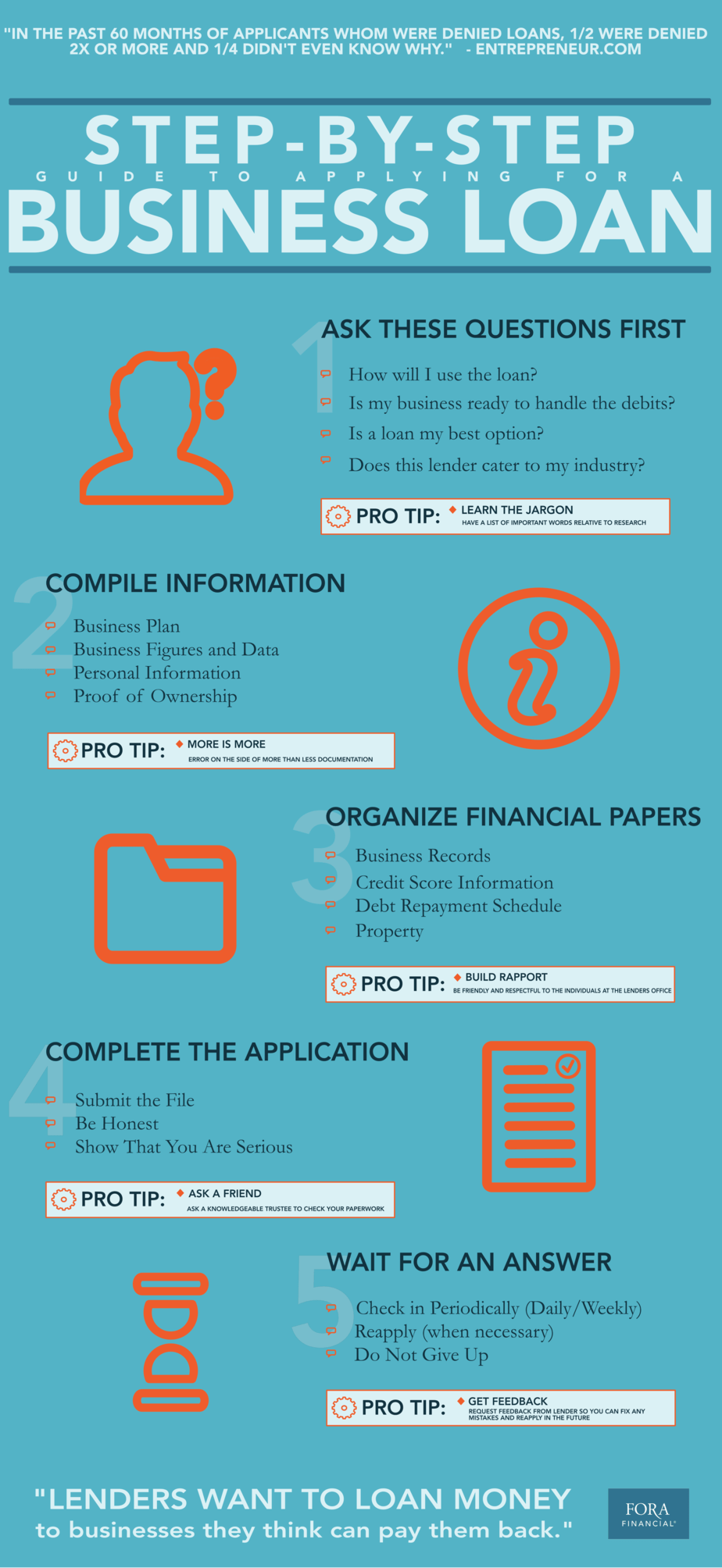

Essential Documents and Financial Preparedness

Even if you tick all the boxes for the Five C’s, a poorly presented application with missing or inaccurate documents can lead to rejection. Thorough preparation of your paperwork is non-negotiable.

Comprehensive Business Plan: Your Roadmap for Success

A well-crafted business plan is more than just a formality; it’s a strategic document that outlines your business’s vision, operations, and financial projections. It demonstrates to lenders that you have a clear understanding of your business and a viable strategy for success.

- Executive Summary: A concise overview of your business, its mission, and its goals.

- Company Description: Legal structure, history, and current status.

- Market Analysis: Your target market, industry trends, and competitive analysis.

- Organization & Management: The structure of your business and the expertise of your management team.

- Service or Product Line: Detailed description of what you offer.

- Marketing & Sales Strategy: How you plan to reach customers and generate revenue.

- Financial Projections: Crucial for lenders. This includes projected profit and loss statements, cash flow statements, and balance sheets for at least the next 3-5 years, along with assumptions backing these figures.

Robust Financial Statements: A Clear Picture of Your Health

Lenders will demand recent and historical financial statements to verify your capacity and capital. These documents should be professionally prepared and reflect an accurate financial picture.

- Profit & Loss (Income Statement): Shows your revenue, costs, and profit over a specific period (e.g., quarterly, annually). Lenders typically ask for the past 2-3 years, plus year-to-date.

- Balance Sheet: A snapshot of your business’s assets, liabilities, and owner’s equity at a specific point in time. It provides insight into your business’s financial health and solvency.

- Cash Flow Statement: Details the cash inflows and outflows from operating, investing, and financing activities. This is vital for assessing your ability to generate cash for repayments.

- Business Tax Returns: Typically required for the past 2-3 years, these corroborate your financial statements.

- Personal Tax Returns: Often requested for business owners, especially for smaller businesses, to assess personal financial stability.

Personal and Business Credit Reports: Knowing Your Score

Before approaching lenders, it’s crucial to obtain and review both your personal and business credit reports.

- Review for Accuracy: Dispute any errors immediately, as even small inaccuracies can negatively impact your score.

- Understand Your Scores: Knowing your scores will help you anticipate how lenders perceive your creditworthiness and address any weaknesses proactively.

Legal and Business Registration Documents: Proof of Legitimacy

Lenders need to verify that your business is legally established and compliant.

- Business Licenses and Permits: Proof that your business is authorized to operate.

- Articles of Incorporation/Organization: Documents that establish your business’s legal structure (e.g., LLC, Corporation).

- Employer Identification Number (EIN): Your business’s federal tax ID.

- Ownership Agreements: Partnership agreements, operating agreements, or bylaws if applicable.

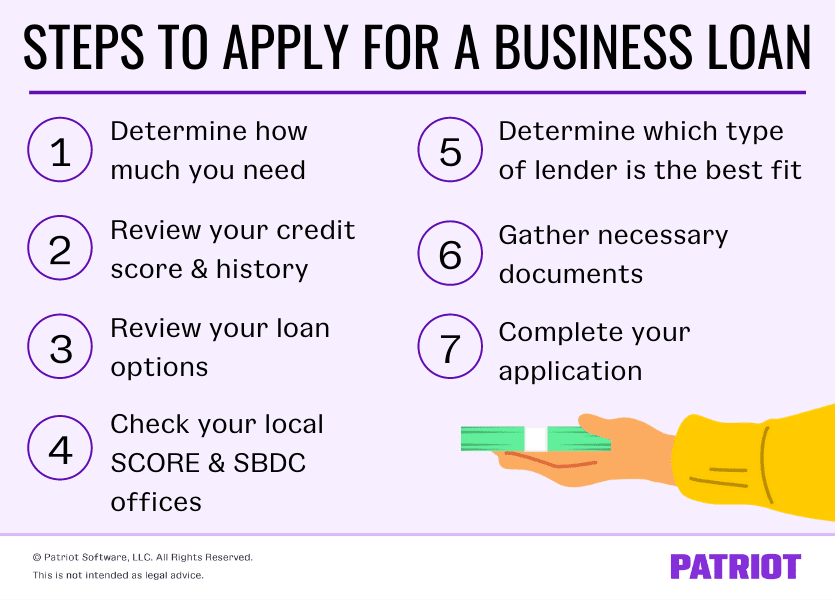

Strategic Steps to Enhance Your Loan Eligibility

Beyond compiling documents, there are proactive measures you can take to bolster your loan application and improve your overall financial standing in the eyes of a lender.

Improve Your Credit Score(s): A Foundation of Trust

This is perhaps the most impactful step you can take.

- Pay Bills On Time, Every Time: Payment history is the biggest factor in both personal and business credit scores.

- Reduce Existing Debt: A lower debt burden demonstrates better financial management and frees up cash flow.

- Keep Credit Utilization Low: For revolving credit, try to use less than 30% of your available credit limit.

- Correct Errors: Regularly check your credit reports for inaccuracies and dispute them promptly.

Strengthen Your Cash Flow: Demonstrate Repayment Ability

Optimizing your cash flow directly addresses the “Capacity” criterion.

- Optimize Accounts Receivable: Invoice promptly, follow up on overdue payments, and consider offering early payment discounts.

- Manage Accounts Payable: Negotiate favorable payment terms with suppliers without jeopardizing relationships.

- Control Expenses: Regularly review and cut unnecessary expenditures.

- Increase Sales and Profit Margins: Ultimately, more revenue and higher profitability naturally improve cash flow.

Build a Strong Relationship with a Lender: Your Financial Partner

Developing a relationship with a bank or credit union before you need a loan can be invaluable.

- Bank Where You Have Accounts: Lenders prefer to work with businesses they already know. If your business banking is with a particular institution, they’ll have access to your transaction history.

- Attend Small Business Events: Network with local bankers and financial advisors.

- Seek Advice: Even if you’re not ready for a loan, discussing your business goals with a bank’s business advisor can provide insights into what they look for.

Explore Different Loan Options: Find the Right Fit

Not all business loans are created equal. Researching and understanding various financing products can help you identify the one best suited to your needs and eligibility.

- SBA Loans: Backed by the Small Business Administration, these loans often have more flexible terms and lower down payments than traditional bank loans, making them accessible to a wider range of businesses.

- Term Loans: Traditional loans with a fixed repayment schedule over a set period.

- Lines of Credit: Flexible funding that allows you to draw and repay funds as needed, ideal for managing working capital.

- Equipment Financing: Specifically for purchasing machinery or equipment, using the equipment itself as collateral.

- Invoice Factoring/Financing: Selling your accounts receivable for immediate cash, useful for businesses with slow-paying clients.

- Alternative Lenders: Online lenders often have faster application processes and more lenient criteria but may come with higher interest rates.

Common Pitfalls to Avoid When Applying for a Business Loan

Even with the best intentions, applicants can make mistakes that jeopardize their chances of approval. Being aware of these common pitfalls can help you steer clear of them.

Incomplete or Inaccurate Documentation: The Application Killer

Submitting an application with missing documents or data that doesn’t align across different reports (e.g., tax returns vs. financial statements) is a red flag for lenders. It wastes their time and signals a lack of attention to detail or even potential dishonesty. Always double-check everything before submission.

Unrealistic Financial Projections: Over-optimism Can Hurt

While optimism is a good trait for an entrepreneur, overly aggressive or unsubstantiated financial projections will be viewed with skepticism. Lenders want to see realistic, well-researched forecasts that are backed by solid assumptions and market data, not wishful thinking.

Poorly Defined Loan Purpose: Lenders Want Clarity

Lenders need to understand exactly why you need the money and how it will be used to grow or stabilize your business. Vague statements like “for working capital” are insufficient. Specify how the funds will directly contribute to revenue generation, cost reduction, or operational efficiency.

Ignoring Your Personal Credit: It Matters More Than You Think

Especially for small businesses, your personal credit history is often a primary indicator of your financial responsibility. Many entrepreneurs mistakenly believe that only their business credit matters. Neglecting personal credit can severely impact your ability to secure business funding.

Waiting Until the Last Minute: Preparation is Key

Applying for a loan when you’re already in a desperate financial situation puts you at a disadvantage. It shows poor financial planning and can force you to accept less favorable terms. Start the qualification process well in advance of when you actually need the funds, allowing ample time for preparation, gathering documents, and addressing any issues.

Qualifying for a business loan is a comprehensive process that demands thorough preparation, transparency, and a deep understanding of your business’s financial health. By focusing on the Five C’s of Credit, meticulously preparing your documentation, proactively strengthening your financial position, and avoiding common missteps, you significantly enhance your chances of securing the capital needed to propel your business forward. Approach the process strategically, and view lenders not just as sources of funding, but as potential partners in your business’s success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.