In the modern financial landscape, the boundary between traditional banking and digital liquidity has become increasingly porous. Cash App, developed by Block, Inc., has evolved from a simple peer-to-peer (P2P) payment service into a robust financial ecosystem that rivals traditional checking accounts. For many users, the Cash App balance serves as a primary hub for daily spending, micro-investing, and even receiving a paycheck. However, to leverage the full utility of this financial tool, one must first understand the various mechanisms for injecting capital into the ecosystem. Knowing how to put money on Cash App is not merely a technical necessity; it is a foundational step in managing personal cash flow and digital assets efficiently.

The Evolution of Mobile Finance: Why Funding Your Cash App Matters

The shift toward a cashless society has accelerated the adoption of digital wallets. Unlike traditional banks, which often come with bureaucratic hurdles and delayed processing times, platforms like Cash App offer a streamlined approach to money management. By maintaining a balance within the app, users gain access to a versatile suite of financial products, including the Cash Card (a Visa debit card), fractional stock investing, and Bitcoin trading.

The Shift from Traditional Banking to Digital Wallets

For decades, personal finance was anchored by the brick-and-mortar bank account. While these institutions remain vital for long-term stability, they often lack the agility required for the modern digital economy. Digital wallets have filled this gap by providing “instant” utility. Funding your digital wallet allows for immediate peer-to-peer transfers, which have become the standard for splitting bills, paying vendors at local markets, or sending gifts to family members. This agility is the primary driver behind the millions of users who now treat their Cash App balance as a secondary—or even primary—spending account.

Cash App as a Central Hub for Personal Finance

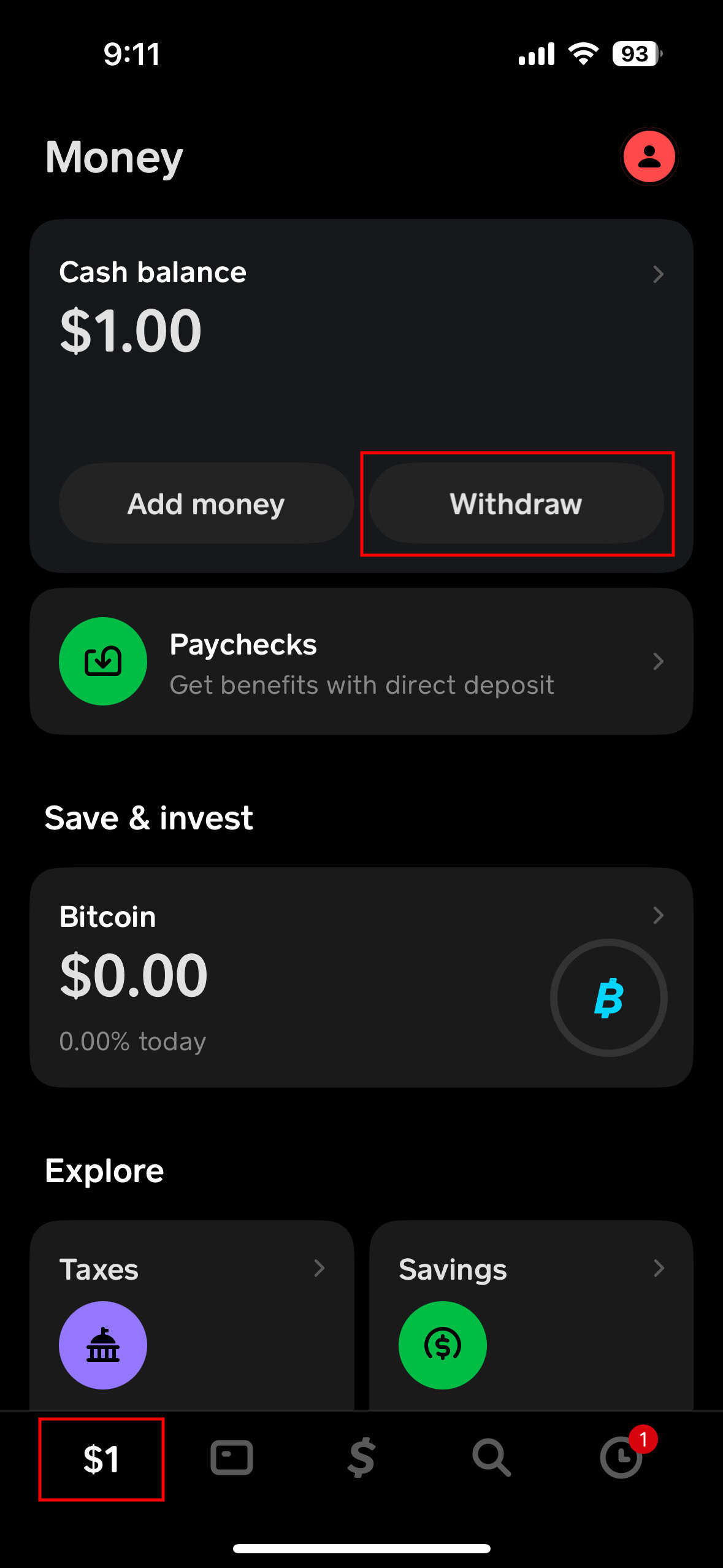

Once capital is loaded into the Cash App ecosystem, it transforms from stagnant currency into an active financial instrument. With a funded account, a user is no longer just a spectator in the economy; they are a participant. The ability to move money into the app opens doors to “Boosts”—instant cash-back rewards—and the ability to automate savings through round-ups. Consequently, understanding the diverse methods of funding is the first step toward optimizing one’s personal financial strategy.

Primary Methods for Adding Money to Your Cash App Balance

There are three primary digital avenues for funding a Cash App account: linking a traditional bank account or debit card, setting up a direct deposit, and receiving funds from other users. Each method serves a different financial need, ranging from immediate liquidity to long-term income management.

Linking Your Bank Account and Debit Card

The most common way to put money on Cash App is by linking a supported debit card or bank account. To do this, users navigate to the “Banking” or “My Cash” tab and select “Add Cash.”

- The Debit Card Advantage: Linking a debit card allows for the near-instantaneous transfer of funds from a traditional bank to the Cash App balance. This is ideal for users who need to make a quick purchase or send money to a friend immediately.

- ACH Transfers: While debit cards are faster, linking a bank account via the Routing and Account number allows for larger transfers and provides a backup if a card is lost or expired. This method uses the Automated Clearing House (ACH) network, which is the backbone of the American electronic financial system.

Direct Deposit: Streamlining Your Income

For those who use Cash App as their primary financial tool, setting up a direct deposit is the most efficient funding strategy. Cash App provides users with a routing and account number, just like a traditional bank.

By directing a portion of a paycheck, tax refund, or government stimulus to Cash App, users can bypass the traditional “wait time” associated with bank transfers. In many cases, Cash App makes direct deposit funds available up to two days earlier than traditional banks. From a personal finance perspective, this improves liquidity and allows for faster allocation of capital toward bills, savings, or investments.

Receiving Peer-to-Peer Transfers

The “P2P” aspect of the app is perhaps its most famous feature. Receiving money from friends, family, or clients is an effortless way to increase your balance. Unlike the “Add Cash” feature, which pulls money from your own external accounts, receiving a transfer increases your net liquidity within the app without depleting your external bank balance. For freelancers and side-hustlers, this has become a preferred method of receiving payments due to the lack of complex invoicing and the speed of transaction.

How to Add Physical Cash at Retail Locations

Despite the digital revolution, many individuals still operate within a cash-based economy. One of the most significant innovations in the Cash App ecosystem is the ability to bridge the gap between physical paper money and digital currency. This is particularly useful for unbanked or underbanked individuals who need to digitize their earnings to pay online bills or invest.

Utilizing the “Paper Money” Deposit Feature

To put physical money on Cash App, the platform utilizes a “Paper Money” feature found within the banking tab. When selected, the app generates a unique barcode. A user can take this barcode to a participating retailer, where the cashier scans it and accepts the physical cash. Once the transaction is processed, the funds appear in the Cash App balance almost instantly. This removes the need to visit a traditional bank branch or ATM to deposit funds, effectively turning thousands of retail locations into “micro-branches” for the user.

Participating Retailers and Convenience Factors

Cash App has partnered with a wide array of national retailers to facilitate these deposits. Major chains such as Walmart, Walgreens, 7-Eleven, Family Dollar, and Rite Aid are common participants. This vast network ensures that even users in rural areas have a point of access to digitize their physical currency. For a personal finance enthusiast, this convenience reduces the “friction” of managing cash, allowing for better tracking of expenses once the money is within the digital system.

Understanding Service Fees and Limits

While digital transfers from a bank account are typically free, adding physical paper money often incurs a small service fee (usually around $1 per transaction). Additionally, there are limits on how much cash can be deposited—typically $500 per transaction and $1,000 to $4,000 per month depending on the user’s verification status. From a financial planning standpoint, it is important to factor these fees into your budget and ensure your account is “Verified” to unlock higher deposit limits, providing greater flexibility for your capital.

Maximizing the Utility of Your Funded Cash App Account

Putting money on Cash App is only the beginning. The real value lies in how that capital is deployed. Once the account is funded, the platform offers several avenues for wealth building and savvy spending that go beyond simple transactions.

Investing in Stocks and Bitcoin

Cash App has democratized investing by allowing users to purchase fractional shares of stocks and Bitcoin with as little as $1. Because the funds are already in the “Cash Balance,” the barrier to entry is significantly lowered. Instead of waiting several days for a brokerage transfer, a user can see a market opportunity and execute a trade in seconds. This allows for “dollar-cost averaging”—a popular personal finance strategy where a user invests a fixed amount of money at regular intervals—to be performed effortlessly within the same app used for daily coffee purchases.

Leveraging Cash Card Boosts for Instant Savings

The Cash Card is a free Visa debit card that uses the funds in your Cash App balance. The “Boost” feature is one of the most effective personal finance tools available on the platform. By selecting a specific “Boost” (such as 5% off at a grocery store or $1 off at a coffee shop), the discount is applied instantly at the point of sale. Unlike traditional credit card rewards that require users to accumulate points over months, Boosts provide immediate savings. To maximize this, users should ensure their Cash App balance is always sufficiently funded to cover daily expenses, allowing them to capture these micro-savings consistently.

Security and Best Practices for Managing Digital Funds

As with any financial tool, the security of your funds is paramount. As you put more money into the Cash App ecosystem, you must treat it with the same level of caution as a traditional bank account. Digital security is an integral part of personal finance in the 21st century.

Protecting Your Balance with Security Features

Cash App provides several layers of protection to ensure your funded balance remains secure. Users should enable the “Security Lock,” which requires a PIN or biometric ID (like FaceID) for every payment. Furthermore, enabling notification alerts for every transaction allows for real-time monitoring of account activity. If an unauthorized transaction occurs, having these alerts enabled allows the user to react immediately, potentially freezing the Cash Card to prevent further loss.

Verifying Your Identity for Higher Limits

To fully integrate Cash App into your financial life, identity verification is essential. By providing your full name, date of birth, and the last four digits of your Social Security Number, you move from a “basic” user to a “verified” user. This process is standard for financial institutions to comply with “Know Your Customer” (KYC) regulations. Verification not only increases your limits for adding and sending money but also adds a layer of institutional trust to your account. In the world of personal finance, being verified is the key to unlocking the full potential of digital banking tools, ensuring that your capital is both mobile and secure.

By mastering the various ways to put money on Cash App—from digital bank links and direct deposits to retail cash inputs—you position yourself to take full advantage of a versatile financial ecosystem. Whether your goal is seamless peer-to-peer payments, instant cash-back savings, or building a portfolio of Bitcoin and stocks, a well-funded Cash App account is a powerful asset in any modern personal finance toolkit.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.