Navigating the complexities of the Internal Revenue Service (IRS) is often viewed as a daunting task for many taxpayers. However, the modern financial landscape has significantly streamlined the process of fulfilling tax obligations. Whether you are a salaried employee, a freelancer navigating the world of self-employment, or a business owner managing corporate finances, understanding how to make payments efficiently is a cornerstone of sound financial management. Failing to pay on time or using the wrong channel can lead to unnecessary penalties, accrued interest, and administrative headaches. This guide provides an in-depth exploration of the various payment methods available today, the strategic considerations for choosing each, and the best practices to ensure your financial standing remains secure.

Digital First: Navigating IRS Online Payment Portals

In an era defined by digital transformation, the IRS has moved aggressively toward online solutions to reduce paperwork and increase processing speeds. For most taxpayers, digital portals offer the highest degree of security and the most immediate confirmation of payment.

IRS Direct Pay for Individuals

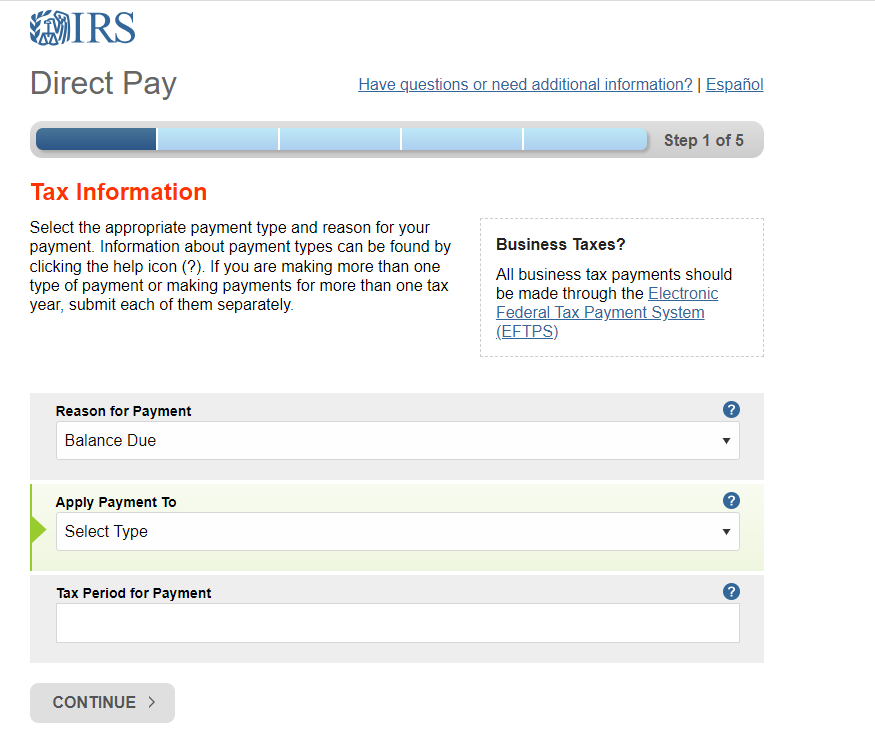

IRS Direct Pay is the most popular choice for individual taxpayers filing Form 1040 series. This service allows you to pay your income tax directly from your checking or savings account without any additional fees. The primary advantage of Direct Pay is its simplicity; it does not require registration or a username. You simply verify your identity using information from a prior year’s tax return and schedule the payment. This tool is ideal for making estimated tax payments, paying a balance due on a filed return, or requesting an extension. From a personal finance perspective, using Direct Pay is the most cost-effective method because it avoids the processing fees associated with credit cards.

The Electronic Federal Tax Payment System (EFTPS)

While Direct Pay is tailored for individuals, the Electronic Federal Tax Payment System (EFTPS) is the workhorse for businesses and high-net-worth individuals with complex requirements. EFTPS is a free service provided by the U.S. Department of the Treasury. Unlike Direct Pay, EFTPS requires an enrollment process, which involves receiving a PIN via physical mail—a process that can take up to 15 days. Once enrolled, however, users can schedule payments up to 365 days in advance, view a comprehensive 16-month payment history, and manage multiple types of taxes (including payroll and corporate taxes). For business owners, EFTPS is an essential financial tool for maintaining compliance and ensuring that large-scale liabilities are handled with professional rigor.

Using the IRS2Go Mobile App

For the mobile-first generation, the IRS2Go app provides a streamlined interface for making payments on the go. Available for both iOS and Android, the app acts as a portal to Direct Pay and credit card processors. While it doesn’t host the payment processing itself, it offers a secure, user-friendly gateway. Beyond payments, the app allows users to check their refund status and receive tax tips, making it a valuable addition to any taxpayer’s financial toolkit.

Alternative Payment Methods and Traditional Channels

While direct bank transfers are preferred for their lack of fees, there are several other ways to settle a tax debt. These methods are often chosen based on the taxpayer’s liquidity needs or desire for convenience.

Credit and Debit Card Payments

The IRS does not collect credit or debit card fees directly; instead, it utilizes third-party payment processors like PayUSAtax, Pay1040, and ACI Payments, Inc. While this method offers the convenience of using credit lines, it comes with a cost. Processors typically charge a percentage-based fee for credit cards (usually between 1.87% and 1.98%) or a flat fee for debit cards (around $2.00 to $2.50).

From a strategic financial standpoint, paying by credit card only makes sense in two scenarios: first, if you are chasing a high-value sign-up bonus on a new credit card where the rewards outweigh the processing fee; or second, if you are facing a liquidity crisis and need to avoid immediate IRS late-payment penalties, which are often higher than credit card interest rates in the short term.

Digital Wallets: PayPal and Venmo

In a relatively recent update to its infrastructure, the IRS now allows payments via digital wallets like PayPal and Venmo through its third-party processors. This integration reflects the changing nature of online income and personal finance. For freelancers or gig economy workers who receive their income through these platforms, paying the IRS directly from their digital balance can simplify their bookkeeping and reduce the friction of transferring funds between multiple bank accounts.

The Traditional Route: Checks, Money Orders, and Cash

Despite the push for digitalization, the IRS continues to accept traditional payment forms. If you choose to pay by check or money order, it must be made payable to the “U.S. Treasury” and include your name, address, Social Security number, daytime phone number, tax year, and the related tax form.

Cash payments are also possible but require more logistical effort. The IRS partners with retail locations such as 7-Eleven, CVS, and Walgreens to accept cash payments up to $1,000 per day. This process requires a specialized “Pay Code” generated through the IRS website. While traditional methods are slower and carry a higher risk of being lost in the mail, they remain vital for the “unbanked” population or those who prefer a physical paper trail.

Managing Debt: Payment Plans and Installment Agreements

Not every taxpayer has the immediate capital to pay their tax bill in full. Recognizing this reality, the IRS offers several mechanisms to manage debt over time, preventing the catastrophic financial impact of aggressive collection actions.

Short-term vs. Long-term Payment Plans

If you cannot pay immediately, you may qualify for an Online Payment Agreement.

- Short-term plans: These allow you up to 180 days to pay the liability in full. There is typically no setup fee for this option, though interest and penalties still accrue until the balance is zero.

- Long-term plans (Installment Agreements): These are for balances that will take more than 180 days to pay. These require monthly payments, often via direct debit. While there is a setup fee (which is significantly reduced for those who choose direct debit and apply online), it provides a structured pathway to clearing debt without the fear of levies or liens.

Offers in Compromise (OIC)

The Offer in Compromise is a specialized financial tool that allows taxpayers to settle their tax debt for less than the full amount they owe. This is generally reserved for individuals facing extreme financial hardship. To qualify, the IRS conducts an exhaustive review of the taxpayer’s “Reasonable Collection Potential,” including assets, income, and necessary expenses. While difficult to obtain, an OIC can provide a “fresh start” for those whose tax liabilities have become mathematically impossible to satisfy.

Understanding Penalties and Interest

A critical part of managing tax payments is understanding the cost of delay. The “Failure to Pay” penalty is 0.5% of the unpaid taxes for each month or part of a month the tax remains unpaid, up to 25%. Additionally, the IRS charges underpayment interest that is adjusted quarterly. Financially savvy taxpayers prioritize paying at least something toward their balance, as even partial payments reduce the base amount upon which these penalties and interest are calculated.

Best Practices for Financial Organization and Security

Making a payment is the final step in a much larger cycle of financial management. Implementing high-level organizational strategies can prevent the stress typically associated with tax season.

Keeping Meticulous Records

Every time a payment is made—whether through Direct Pay, EFTPS, or a check—save a digital and physical copy of the confirmation. The IRS systems are robust, but errors can occur. Having a “Payment Voucher” or a transaction ID is your primary defense if a payment is not properly credited to your account. For business owners, these records are also essential for accurate balance sheets and profit-and-loss statements.

Avoiding Scams and Phishing Attempts

As digital payments become the norm, so do digital scams. The IRS will never initiate contact with taxpayers via email, text messages, or social media to request personal or financial information. They will also never demand immediate payment via gift cards or wire transfers. Always ensure you are on the official “.gov” website before entering sensitive banking information. If you receive a suspicious call, the safest course of action is to hang up and check your account status directly through the official IRS “View Your Account” portal.

Planning for Estimated Quarterly Payments

For those with income not subject to withholding (self-employed individuals, investors, and business partners), paying once a year is not enough. The U.S. tax system is a “pay-as-you-go” system. To avoid a large bill and “underpayment of estimated tax” penalties at year-end, you should calculate and pay estimated taxes quarterly. By treating these payments as a recurring business expense rather than a year-end hurdle, you maintain better cash flow and avoid the liquidity crunch that often plagues the unprepared every April.

In conclusion, paying the IRS is no longer a process of blind bureaucracy but a manageable aspect of modern financial life. By leveraging digital tools like Direct Pay and EFTPS, understanding the trade-offs of credit card usage, and utilizing installment agreements when necessary, taxpayers can maintain their financial health and focus on growth rather than debt. Professionalism in handling tax obligations is not just about compliance; it is about taking control of your broader financial narrative.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.