Tax season often brings a mix of anticipation and anxiety. For many, the primary concern isn’t just filing the paperwork, but the lingering uncertainty of whether a balance remains due. Understanding your standing with the Internal Revenue Service (IRS) is a cornerstone of sound personal finance. Ignorance is rarely bliss when it comes to federal debt; penalties and interest accrue daily, transforming a manageable balance into a significant financial burden.

In the modern financial landscape, checking your tax status has become more streamlined, yet the complexity of tax law remains high. Whether you are a salaried employee, a freelancer in the gig economy, or a small business owner, knowing exactly where you stand with the federal government is essential for maintaining your financial health and peace of mind.

The Paper Trail: Identifying Official IRS Notifications

The most traditional—and still the primary—way the IRS communicates tax debt is through the United States Postal Service. Despite the digital revolution, the IRS does not initiate contact via email, text message, or social media to request personal or financial information.

Understanding the CP2000 Notice

The CP2000, also known as an underreporting notice, is one of the most common documents a taxpayer might receive. This isn’t a bill in the traditional sense, but a proposal. It indicates that the information the IRS received from third parties (like your bank or employer via 1099s and W-2s) does not match the information you reported on your tax return. If you receive this, it is a clear signal that the IRS believes you owe more than you originally calculated.

Decoding Statutory Notices of Deficiency

If a discrepancy is not resolved through initial correspondence, the IRS may issue a “Statutory Notice of Deficiency,” often referred to as a “90-day letter.” This is a formal legal notice stating the IRS’s intent to assess a tax deficiency. Receiving this letter is a critical juncture; you have exactly 90 days to either pay the amount or petition the U.S. Tax Court. Ignoring this document effectively forfeits your right to challenge the amount in court before paying it.

Distinguishing Official Mail from Scams

In the realm of personal finance, security is paramount. Scammers often mimic IRS branding to defraud individuals. A legitimate IRS notice will always be sent via the USPS, will contain a specific notice or letter number (usually in the top right corner), and will provide clear instructions on how to appeal. If you receive a phone call threatening immediate arrest or demanding payment via wire transfer or gift cards, it is a scam. Knowing the official paper trail protects both your wallet and your identity.

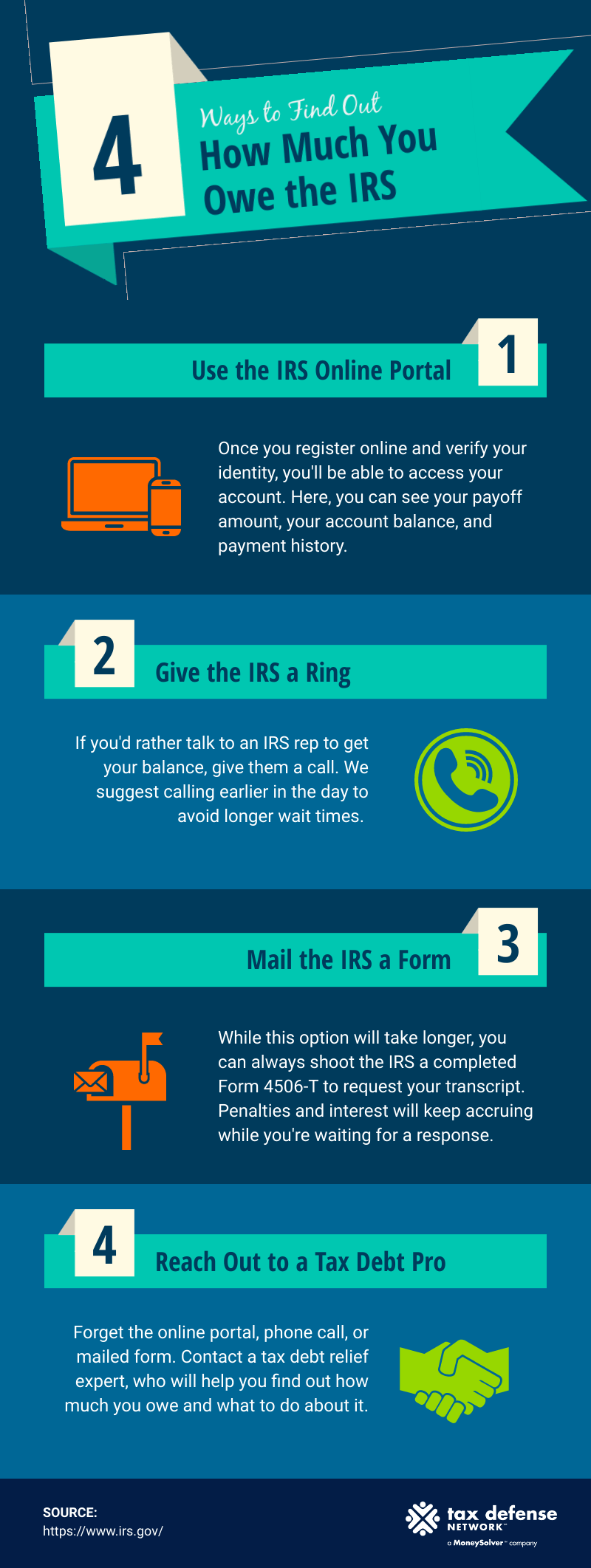

Leveraging Digital Tools: The IRS Online Account Portal

For those who prefer a proactive approach rather than waiting for the mail, the IRS has significantly upgraded its digital infrastructure. The “Your Online Account” feature is the most efficient way to check your balance in real-time.

Navigating the ID.me Verification Process

To access your federal tax information online, you must first verify your identity through ID.me, a third-party technology provider. This process involves uploading government-issued photo identification and performing a live selfie scan. While it may seem cumbersome, this level of security is necessary to protect sensitive financial data from unauthorized access. Once registered, you gain immediate access to your “Account Home,” which displays your total balance due, including a breakdown by tax year.

Reviewing Tax Transcripts for Deep Insights

An account balance tells you how much you owe, but a transcript tells you why. Within your online portal, you can request various types of transcripts. The “Account Transcript” is particularly useful for identifying debt; it lists all “transactions” on your account, including assessments, credits, and any penalties or interest that have been applied. By reviewing these transcripts, you can trace the history of your debt and identify if a specific filing error led to the current balance.

Tracking Payment History and Pending Actions

The online portal also allows you to view your payment history from the last 24 months. This is vital for taxpayers who make quarterly estimated payments or those who have set up automated installment agreements. If you believe you paid an amount that isn’t reflected in your balance, the “Payment History” tab allows you to cross-reference your bank statements with IRS records to find discrepancies.

Common Catalysts for Unexpected Tax Debt

Many taxpayers are blindsided by tax debt because they aren’t aware of how certain life changes or financial moves impact their liability. Identifying these catalysts can help you anticipate debt before the IRS sends a notice.

The Impact of Side Hustles and 1099 Income

In the “Money” niche, side hustles are a popular way to increase wealth. However, they often lead to “sticker shock” during tax season. If you earn more than $400 from self-employment, you are responsible for both the employer and employee portions of Social Security and Medicare taxes (Self-Employment Tax). If you haven’t been setting aside approximately 25-30% of your gross side-income for taxes, you will likely find yourself owing the IRS when you file your annual return.

Capital Gains and Investment Income

Profits from the sale of stocks, cryptocurrencies, or real estate are taxable events. Many retail investors fail to account for capital gains taxes, especially short-term gains which are taxed at ordinary income rates. If you had a successful year in the markets but didn’t adjust your withholdings or make estimated payments, the IRS will expect their share of those profits, often resulting in an unexpected balance due.

Errors in Deductions and Credits

The IRS uses automated systems to flag returns that claim “unusually high” deductions relative to income levels. If you claimed the Earned Income Tax Credit (EITC) or Child Tax Credit incorrectly, or if you over-inflated business expenses on a Schedule C, the IRS may disallow these claims upon review. This reversal creates an immediate debt, often coupled with accuracy-related penalties.

Strategic Resolution: What to Do If You Owe

Discovering that you owe the IRS can be stressful, but the federal government offers several paths for resolution. The key is to act quickly to minimize interest and penalties.

Setting Up a Federal Installment Agreement

If you cannot pay your balance in full immediately, an installment agreement is often the best financial move. For balances under $50,000, you can usually apply for a streamlined installment agreement online. This allows you to pay off the debt over a period of up to 72 months. While interest still accrues, the “failure to pay” penalty is often reduced, making the debt more manageable within your monthly budget.

The Offer in Compromise (OIC)

For those in genuine financial distress, an Offer in Compromise allows you to settle your tax debt for less than the full amount you owe. This is a rigorous process where the IRS evaluates your “Reasonable Collection Potential” based on your assets, income, and necessary living expenses. While difficult to qualify for, an OIC can provide a fresh start for taxpayers whose debt significantly exceeds their ability to pay.

Requesting “Currently Not Collectible” Status

If paying any amount toward your tax debt would prevent you from meeting basic living expenses (rent, food, utilities), you can request that the IRS place your account in “Currently Not Collectible” (CNC) status. While this does not wipe away the debt—and interest continues to accrue—it stops the IRS from engaging in active collection efforts like wage garnishments or bank levies until your financial situation improves.

Proactive Financial Planning to Avoid Future Debt

The ultimate goal of managing your “Money” profile is to move from a defensive posture to a proactive one. Once you have identified and addressed your current debt, you must implement systems to prevent a recurrence.

Adjusting Your W-4 Withholdings

If you are an employee and consistently find yourself owing money at the end of the year, your W-4 form is likely outdated. Life events like marriage, the birth of a child, or a spouse starting a new job can change your tax bracket. Using the IRS Tax Withholding Estimator tool can help you determine the exact amount to have withheld from your paycheck so that you break even—or receive a small refund—each April.

Mastering Estimated Quarterly Payments

For the self-employed and those with significant investment income, waiting until April to pay taxes is a recipe for debt. The US tax system is a “pay-as-you-go” system. By making quarterly estimated payments (due in April, June, September, and January), you stay current with your obligations. This not only avoids a large year-end bill but also prevents “underpayment penalties” that the IRS charges for not paying enough throughout the year.

![]()

Consulting with Financial Professionals

Tax laws are subject to frequent changes through legislative acts. Engaging with a Certified Public Accountant (CPA) or a tax strategist can provide a layer of protection. These professionals can identify tax-saving opportunities—such as contributing to a SEP-IRA or a Health Savings Account (HSA)—that reduce your taxable income and, consequently, the likelihood that you will owe the IRS in the future.

Managing your relationship with the IRS is a fundamental aspect of comprehensive financial planning. By staying vigilant with notices, utilizing online tools, and understanding the mechanics of your tax liability, you can ensure that you are never caught off guard by federal debt. Knowledge is the most effective tool for maintaining financial stability and ensuring your money works for you, rather than being drained by avoidable penalties.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.