For decades, the S&P 500 has been heralded as the “gold standard” of the American stock market. Comprising 500 of the largest, most successful companies listed on U.S. exchanges, it serves as a barometer for the health of the global economy. For the individual investor, the S&P 500 represents one of the most effective tools for long-term wealth creation. Legendary investor Warren Buffett has famously recommended that the average person should simply buy a low-cost S&P 500 index fund and hold it for decades.

However, “investing in the S&P 500” isn’t as simple as clicking a single button without understanding the underlying mechanics. To maximize returns and minimize risk, an investor must understand what the index is, the different vehicles available for investment, and the strategic approaches to managing a portfolio. This guide provides a deep dive into the “Money” niche, focusing on the tactical and philosophical aspects of S&P 500 investing.

1. Understanding the S&P 500 Index

Before putting your hard-earned capital at risk, it is essential to understand exactly what you are buying. The S&P 500, or Standard & Poor’s 500, is a stock market index that tracks the performance of approximately 500 large-cap companies in the United States.

The Selection Process and Criteria

Unlike some indices that are strictly based on size, the S&P 500 is curated by a committee. To be included, a company must meet specific liquidity and size requirements, and importantly, it must be profitable. This “quality filter” ensures that the index isn’t just a list of the largest companies, but a list of the most robust ones. It covers approximately 80% of the available market capitalization in the U.S., making it a comprehensive representation of the corporate landscape.

Market Capitalization Weighting

The S&P 500 is a float-adjusted market-capitalization-weighted index. This means that larger companies like Apple, Microsoft, and Amazon have a more significant impact on the index’s performance than smaller members. When you invest in the S&P 500, you are essentially betting on the continued dominance of America’s corporate giants while still maintaining exposure to hundreds of other firms across various sectors like healthcare, energy, and consumer staples.

Historical Performance and Expectations

Historically, the S&P 500 has provided an average annual return of approximately 10% before inflation. While past performance is never a guarantee of future results, this consistent growth over the last century has made it the cornerstone of retirement planning. Understanding that the index can fluctuate—sometimes dropping 20% or more in a single year—is crucial for maintaining the emotional discipline required for long-term investing.

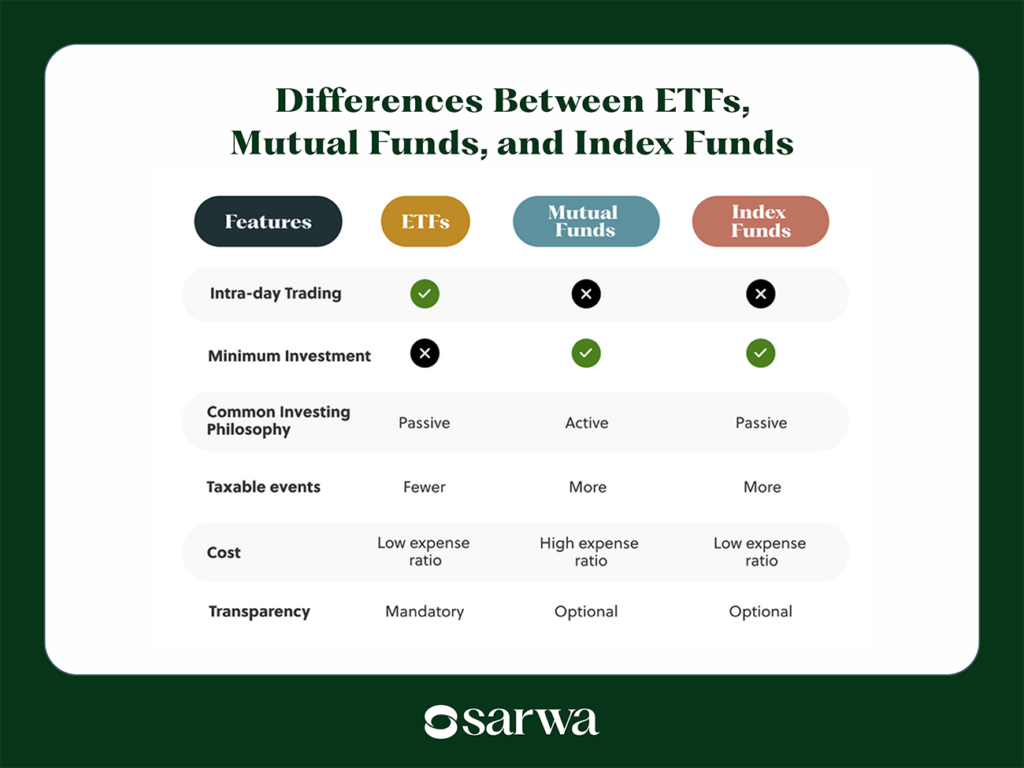

2. Choosing Your Investment Vehicle: ETFs vs. Index Funds

You cannot “buy” the S&P 500 directly because it is an index, not a stock. Instead, you must invest in a fund that tracks the index. The two primary ways to do this are through Exchange-Traded Funds (ETFs) and Mutual Funds (Index Funds).

The Rise of the S&P 500 ETF

ETFs are the most popular choice for modern investors. They trade like individual stocks on an exchange, meaning their prices fluctuate throughout the trading day. Popular examples include the SPDR S&P 500 ETF Trust (SPY), the iShares Core S&P 500 ETF (IVV), and the Vanguard S&P 500 ETF (VOO).

- Liquidity: ETFs can be bought and sold instantly during market hours.

- Lower Minimums: You can often start with the price of just one share, or even less if your broker offers fractional shares.

- Tax Efficiency: Due to their structure, ETFs typically generate fewer capital gains distributions than mutual funds.

Traditional Index Mutual Funds

Index mutual funds, such as the Vanguard 500 Index Fund (VFIAX), are priced only once at the end of the trading day. They are ideal for investors who prefer a “set it and forget it” approach.

- Automated Investing: Mutual funds make it very easy to set up recurring monthly contributions of a specific dollar amount (e.g., $500 every month), regardless of the share price.

- Minimum Investment: Some mutual funds require a minimum initial investment (often $3,000), which can be a barrier for beginners.

Evaluating Expense Ratios

In the world of “Money” and finance, fees are the enemy of growth. The “expense ratio” is the annual fee you pay the fund manager to run the fund. For S&P 500 funds, these should be extremely low—often between 0.03% and 0.09%. Over thirty years, the difference between a 0.03% fee and a 1.00% fee can amount to hundreds of thousands of dollars in lost gains.

3. A Step-by-Step Roadmap to Getting Started

Once you understand the “what” and the “how,” it is time to execute the “where.” Following a structured process ensures that you don’t fall victim to analysis paralysis.

Selecting the Right Brokerage

To buy an S&P 500 fund, you need a brokerage account. In the modern era, most major brokerages have eliminated trading commissions.

- Discount Brokerages: Platforms like Fidelity, Charles Schwab, and Vanguard are excellent for long-term investors.

- FinTech Apps: Apps like Robinhood or Betterment offer user-friendly interfaces, though they may lack some of the deep research tools provided by traditional firms.

- Account Types: Consider whether you should invest through a taxable brokerage account or a tax-advantaged account like a 401(k) or an Individual Retirement Account (IRA). Investing via a Roth IRA, for example, allows your S&P 500 gains to grow completely tax-free.

Executing the Trade

Once your account is funded, you search for the ticker symbol of your chosen fund (e.g., VOO). You then decide how many shares to buy or how much money to invest. For beginners, a “Market Order” is the simplest way to buy immediately at the current price. For those more concerned about price volatility, a “Limit Order” allows you to set a maximum price you are willing to pay.

Setting Up a Contribution Schedule

Wealth is built through consistency rather than timing. The most successful S&P 500 investors are those who contribute every month, regardless of whether the market is at an all-time high or in a temporary slump. Setting up an automatic transfer from your bank account to your brokerage account removes the emotional burden of “deciding” when to invest.

4. Advanced Strategies for Long-Term Success

Investing in the S&P 500 is not just about buying; it is about managing your position over decades. To truly master this niche of personal finance, one must employ specific strategies to optimize returns.

Dollar-Cost Averaging (DCA)

Dollar-cost averaging is the practice of investing a fixed amount of money at regular intervals. When the market is high, your dollar buys fewer shares; when the market is low, your dollar buys more shares. This mathematically lowers your average cost per share over time and eliminates the risk of “buying at the top.” In the volatile world of finance, DCA is a psychological safety net that keeps you invested during downturns.

Dividend Reinvestment Plans (DRIP)

Most companies in the S&P 500 pay dividends—a portion of their earnings distributed to shareholders. While you can take this as cash, the real power of the S&P 500 comes from “compounding.” By enabling a Dividend Reinvestment Plan (DRIP) through your broker, your dividends are automatically used to buy more shares of the fund. Over decades, these reinvested dividends can account for nearly half of your total portfolio growth.

Portfolio Rebalancing and Diversification

While the S&P 500 is diversified across 500 companies, it is 100% concentrated in U.S. large-cap stocks. A sophisticated financial strategy might involve pairing your S&P 500 investment with international stocks or bonds to reduce volatility. As you age and move closer to retirement, you may choose to “rebalance”—selling some of your S&P 500 holdings to buy more stable assets like Treasury bonds.

5. Navigating Risks and Market Volatility

No investment is without risk. To be a successful investor in the S&P 500, you must prepare for the inevitability of market cycles.

Understanding Market Corrections and Bear Markets

The S&P 500 does not move in a straight line. “Corrections” (a 10% drop) and “Bear Markets” (a 20% or more drop) are natural parts of the economic cycle. Historically, the S&P 500 has recovered from every single downturn it has ever faced. The greatest risk to an investor is not the market dropping, but the investor panicking and selling at the bottom.

Concentration Risk in the Tech Sector

In recent years, the S&P 500 has become increasingly concentrated in the technology sector. The “Magnificent Seven” (companies like Nvidia, Microsoft, and Apple) now make up a significant portion of the index’s weight. Investors should be aware that if the tech sector faces a specific downturn, the entire S&P 500 will feel the impact, even if other sectors like energy or utilities are doing well.

The Impact of Inflation and Economic Policy

Because the S&P 500 represents the “real economy,” it is sensitive to interest rate changes by the Federal Reserve and fluctuations in inflation. High inflation can erode corporate profits, while high interest rates make it more expensive for companies to borrow and grow. However, because these companies have “pricing power”—the ability to raise prices for consumers—the S&P 500 has historically been an excellent hedge against inflation over long periods.

In conclusion, investing in the S&P 500 is perhaps the most reliable path to financial independence available to the general public. By choosing low-cost funds, maintaining a consistent contribution schedule, and reinvesting dividends, you harness the collective growth of the most powerful companies in the world. While the market will always have its seasons of volatility, the disciplined investor treats the S&P 500 not as a gamble, but as a long-term partnership with the future of global commerce.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.