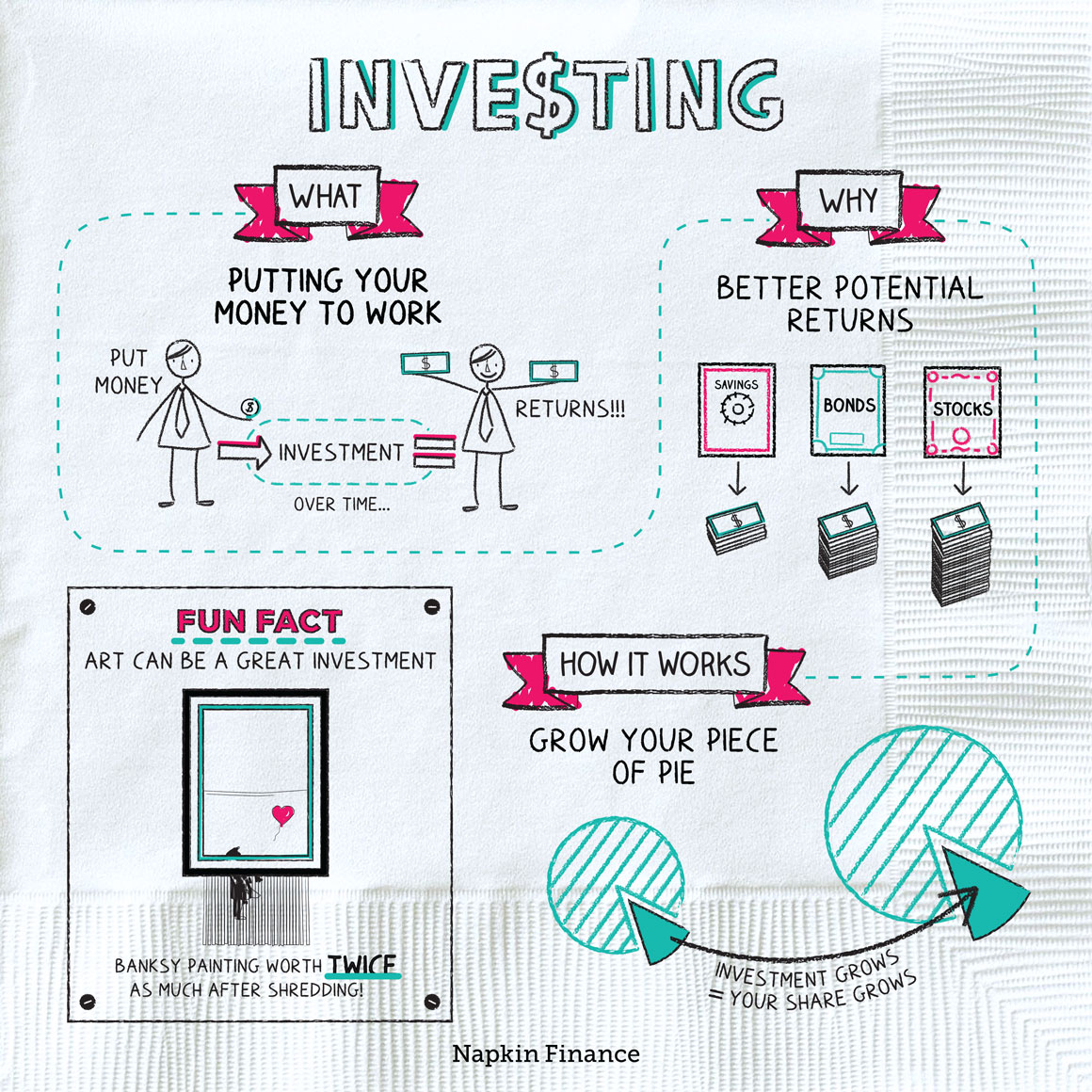

Investing is often perceived as a complex pursuit reserved for Wall Street professionals or those with substantial capital. However, the reality is far more democratic. At its core, investing is the act of allocating resources—usually money—with the expectation of generating an income or profit. In the modern financial landscape, learning how to invest money is no longer a luxury; it is a fundamental skill required to outpace inflation, build long-term security, and achieve financial independence.

Successfully navigating the markets requires more than just picking a “hot stock.” It demands a strategic approach, an understanding of risk, and the discipline to remain committed to a long-term vision. This guide explores the essential pillars of investing, from psychological preparation to asset allocation and tax efficiency.

1. Laying the Groundwork: The Psychology and Preparation of Investing

Before committing a single dollar to the markets, an investor must establish a solid financial foundation. Investing without a plan is akin to sailing without a compass; you may move, but you are unlikely to reach your desired destination.

Defining Your Financial Goals

The first step in any investment journey is identifying “the why.” Are you investing for a comfortable retirement thirty years from now? Are you saving for a down payment on a home in five years? Or are you looking to create a passive income stream to supplement your current salary? Your goals dictate your strategy. Long-term goals allow for more aggressive, growth-oriented investments, while short-term goals necessitate capital preservation and liquidity.

Building an Emergency Fund and Managing Debt

It is a cardinal rule of personal finance: do not invest money that you might need next month. Before entering the market, ensure you have an emergency fund covering three to six months of living expenses. This “liquidity cushion” prevents you from being forced to sell your investments during a market downturn to cover unexpected costs. Additionally, it is generally wise to pay down high-interest debt, such as credit card balances, before investing. The “return” on paying off a 20% interest credit card is a guaranteed 20%, which is significantly higher than the average historical return of the stock market.

Understanding Risk Tolerance and Time Horizons

Every investment carries some degree of risk. Your risk tolerance is a combination of your financial ability to withstand a loss and your emotional temperament during market volatility. Generally, the longer your time horizon, the more risk you can afford to take. A 25-year-old can weather a 30% market correction because they have decades for the market to recover. A 60-year-old approaching retirement, however, must prioritize stability to ensure their capital is available when they stop working.

2. Diversification and Asset Classes: Where to Put Your Capital

Once your foundation is set, the next step is understanding the “building blocks” of a portfolio. Asset allocation—the process of dividing your investment portfolio among different asset categories—is one of the most significant factors in determining your long-term returns.

The Stock Market: Growth and Dividends

Equities, or stocks, represent ownership in a company. When you buy a share, you are betting on the future success of that business. Stocks are traditionally the primary engine of growth in an investment portfolio. They offer two ways to earn money: capital appreciation (the stock price goes up) and dividends (a portion of the company’s profits paid out to shareholders). While stocks offer the highest potential for long-term returns, they also come with higher volatility.

Bonds and Fixed Income: Stability and Income

Bonds are essentially loans you make to an entity, such as a government or a corporation, for a set period at a fixed interest rate. Bonds are generally considered safer than stocks because they provide a predictable stream of income and the return of principal upon maturity. In a balanced portfolio, bonds act as a stabilizer, cushioning the blow when the stock market experiences a downturn.

Real Estate and Alternative Investments

Beyond stocks and bonds, many investors look to real estate as a way to build wealth. This can be done through direct ownership of property or through Real Estate Investment Trusts (REITs), which allow you to invest in large-scale income-producing real estate without having to manage physical buildings. Other alternative investments include commodities (like gold or oil), private equity, and venture capital. These assets often have a low correlation with the stock market, providing further diversification.

3. Strategic Approaches: Passive vs. Active Management

How you manage your investments is just as important as what you invest in. In the modern era, the debate between active management (trying to beat the market) and passive management (matching the market) has largely been won by the latter for the average individual investor.

The Power of Index Funds and ETFs

An index fund is a type of mutual fund or Exchange-Traded Fund (ETF) with a portfolio constructed to match or track the components of a financial market index, such as the S&P 500. Instead of paying high fees to a fund manager to pick individual “winners,” index funds provide broad market exposure, low operating expenses, and low portfolio turnover. For most investors, low-cost index funds are the most efficient vehicle for long-term wealth accumulation.

Dollar-Cost Averaging: Mitigating Volatility

One of the biggest hurdles for new investors is “market timing”—the attempt to buy when prices are low and sell when they are high. This is notoriously difficult, even for professionals. A more effective strategy is dollar-cost averaging (DCA). With DCA, you invest a fixed amount of money at regular intervals, regardless of the price. When prices are high, you buy fewer shares; when prices are low, you buy more. Over time, this lowers your average cost per share and removes the emotional stress of trying to “time” the market.

Portfolio Rebalancing for Long-Term Health

Over time, different investments will grow at different rates, causing your original asset allocation to shift. For example, if your target was 60% stocks and 40% bonds, a strong year in the stock market might leave you with 70% stocks. Rebalancing is the process of selling some of your “winners” and buying more of your “underperformers” to bring your portfolio back to its target allocation. This disciplined approach forces you to “buy low and sell high” automatically.

4. Tax Efficiency and Account Selection

It is not just about how much you make; it is about how much you keep. Tax efficiency is a critical, yet often overlooked, component of investing. By using the right types of accounts, you can significantly increase your ending wealth.

Retirement Accounts: 401(k)s and IRAs

In many jurisdictions, the government provides tax-advantaged accounts to encourage retirement savings. In the United States, for example, a 401(k) or a traditional IRA allows you to invest pre-tax dollars, meaning your contributions reduce your taxable income today. Alternatively, a Roth IRA uses after-tax dollars, but the withdrawals in retirement are completely tax-free. Utilizing these accounts should be a priority, especially if an employer offers a matching contribution—which is essentially a 100% return on your investment.

Taxable Brokerage Accounts for Flexibility

While retirement accounts have great tax benefits, they often come with restrictions on when you can withdraw the money. For goals that occur before retirement, a standard taxable brokerage account is necessary. While you will owe taxes on dividends and capital gains, these accounts offer the greatest flexibility, allowing you to buy and sell assets and withdraw funds at any time.

5. Navigating the Modern Investment Landscape

The tools available to investors today are more powerful and accessible than ever before. However, this accessibility comes with the need for greater self-discipline and a clear understanding of the digital tools at your disposal.

The Role of Robo-Advisors

For those who prefer a “hands-off” approach, robo-advisors have revolutionized the industry. These digital platforms use algorithms to build and manage a diversified portfolio based on your risk tolerance and goals. They handle everything from asset allocation to automatic rebalancing and tax-loss harvesting, usually for a fraction of the cost of a human financial advisor.

Avoiding Common Pitfalls and Emotional Biases

The greatest enemy of the investor is often themselves. Behavioral finance shows that humans are prone to cognitive biases, such as “loss aversion” (feeling the pain of a loss more than the joy of a gain) and “herding” (following the crowd). Successful investing requires the ability to ignore the daily noise of the news cycle and stay the course during periods of market turbulence. High-frequency trading, chasing “meme stocks,” or reacting to sensationalist headlines are the fastest ways to erode your capital.

The Importance of Continuous Education

The financial world is dynamic. Regulations change, new investment products emerge, and global economic shifts impact asset values. While your core strategy should remain consistent, staying informed is vital. Whether it is reading financial news, listening to investment podcasts, or consulting with a fee-only financial advisor, continuous education ensures that you remain in control of your financial destiny.

In conclusion, investing is a marathon, not a sprint. By understanding your goals, diversifying your assets, minimizing fees through passive strategies, and utilizing tax-advantaged accounts, you can harness the power of compounding interest. The most important step in how to invest money is simply the act of starting. Time is the most valuable asset an investor has; the sooner you put your money to work, the more time it has to grow into the wealth required for your future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.