Securing capital is often the most significant hurdle for entrepreneurs and small business owners. Whether you are looking to launch a startup, manage seasonal cash flow fluctuations, or scale an existing operation, understanding the mechanics of business finance is essential. A small business loan is more than just an injection of cash; it is a strategic tool that, when used correctly, can accelerate growth and fortify a company’s market position. However, the path to funding is often paved with complex requirements, diverse lending products, and rigorous scrutiny.

To successfully navigate this landscape, business owners must approach the lending process with the same precision they apply to their core operations. This guide provides a deep dive into the financial prerequisites, the variety of loan types available in today’s market, and the tactical steps required to secure the funding your business deserves.

Understanding the Prerequisites for Business Funding

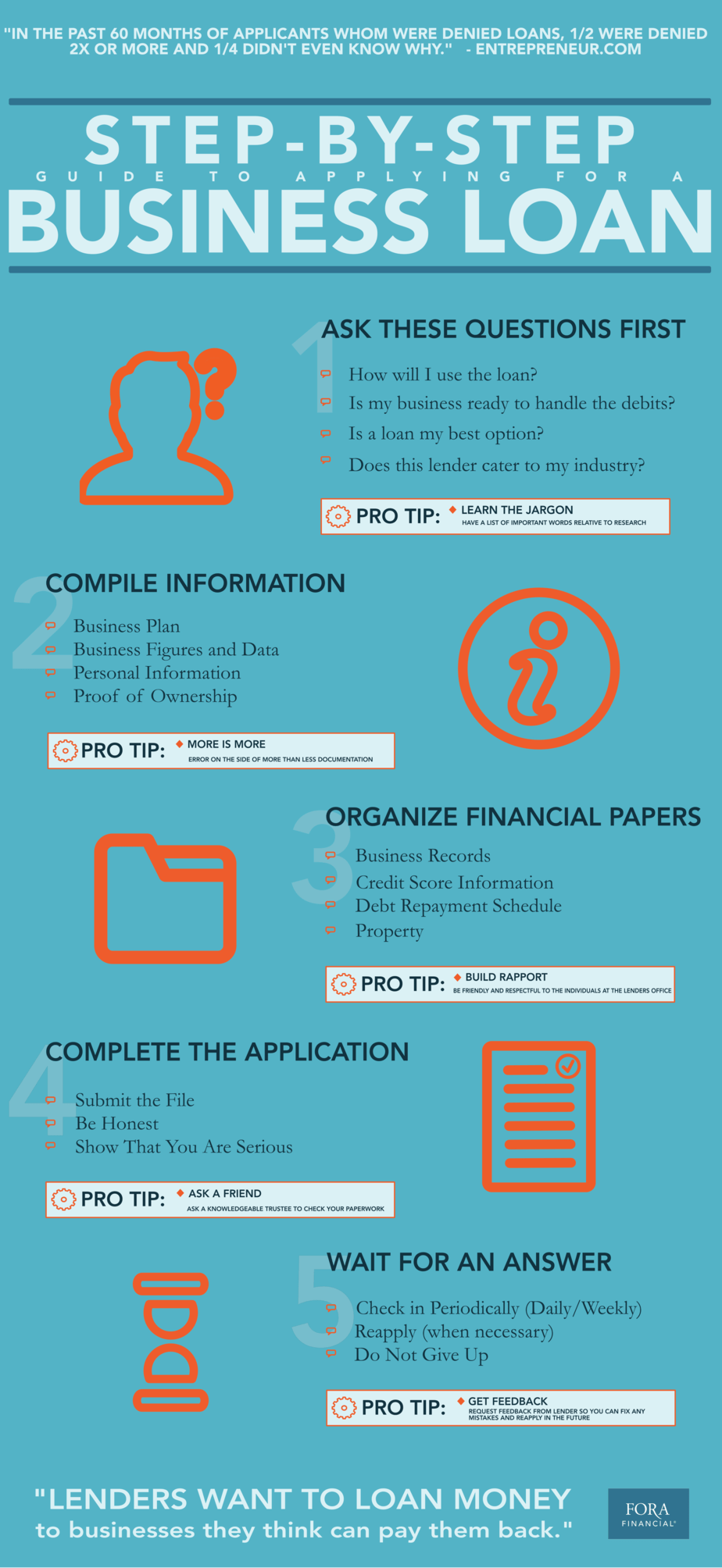

Before approaching a lender, it is imperative to conduct a thorough internal audit of your financial standing. Lenders do not simply look at your current revenue; they analyze your historical performance, your personal financial habits, and the viability of your business model.

Assessing Your Creditworthiness and Financial Health

The first thing a lender will evaluate is risk. In the world of small business finance, your personal credit score is often as important as your business credit score, especially for sole proprietorships or young companies. A personal FICO score above 680 is generally the baseline for traditional bank loans, while alternative lenders may be more flexible.

Beyond credit scores, lenders look at your Debt-to-Income (DTI) ratio and your Debt Service Coverage Ratio (DSCR). The DSCR is particularly vital; it measures your business’s ability to pay its current debt obligations with its operating income. A ratio of 1.25 or higher indicates that you have enough cushion to handle loan payments comfortably. Ensuring these metrics are optimized before applying can drastically increase your approval odds.

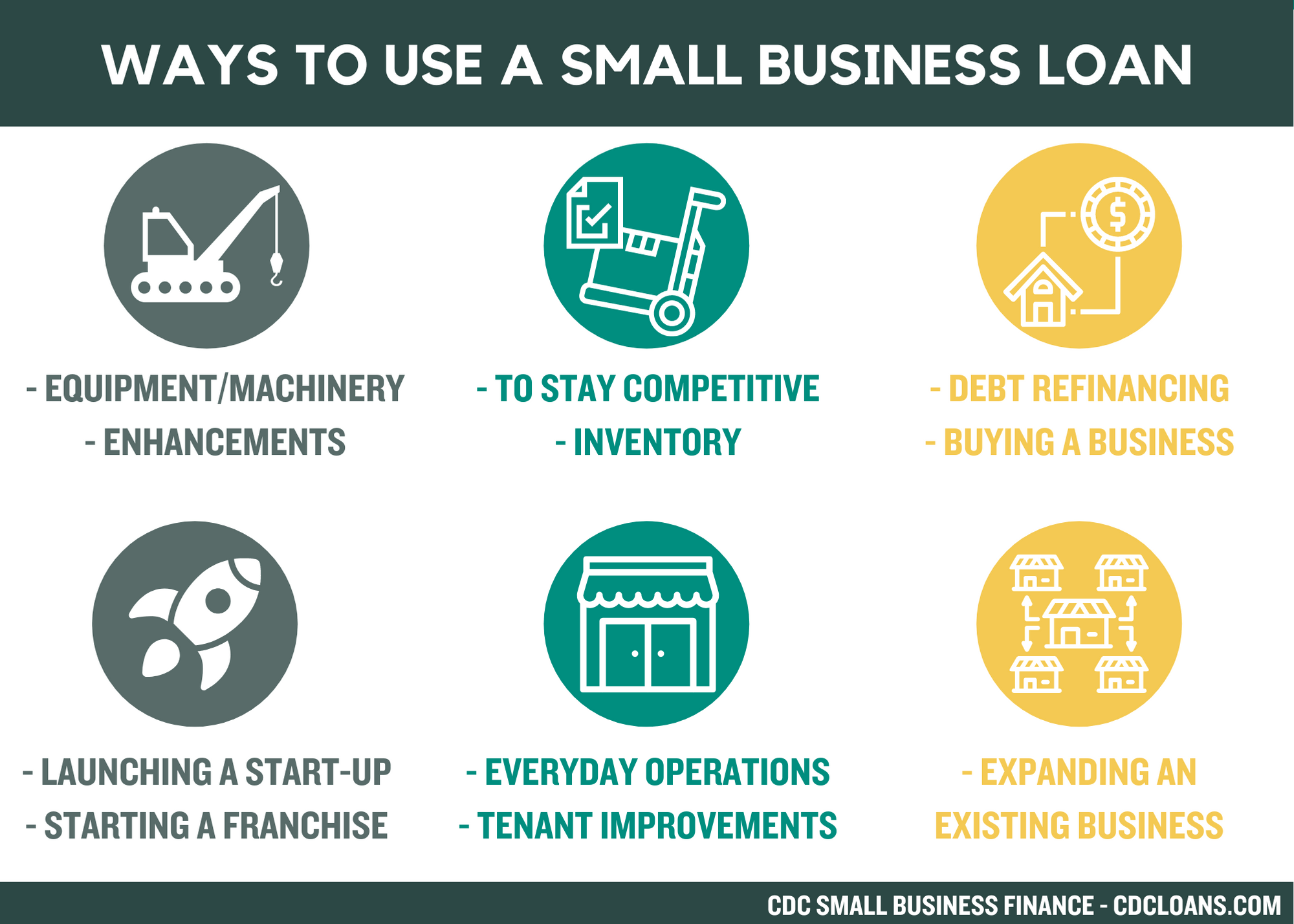

Defining Your Loan Purpose and Capital Needs

One of the most common mistakes entrepreneurs make is asking for “as much as possible” without a specific plan. Lenders want to see a clear “Use of Funds” statement. Are you purchasing inventory to meet a holiday rush? Are you investing in heavy machinery that will increase production capacity by 40%? Or are you refinancing high-interest debt to improve monthly cash flow?

By quantifying your needs, you avoid the trap of over-borrowing, which leads to unnecessary interest expenses, or under-borrowing, which leaves you undercapitalized. A precise financial request signals to the lender that you are a disciplined manager of capital.

Exploring the Diverse Landscape of Small Business Loans

The financial market has evolved significantly over the last decade. While traditional banks remain a primary source of capital, a variety of alternative and government-backed programs have emerged to fill the gaps for businesses that may not meet the strictest institutional criteria.

Traditional Bank Loans and SBA-Backed Options

For businesses with a solid track record and strong collateral, traditional term loans from commercial banks offer some of the lowest interest rates and longest repayment terms. These are ideal for long-term investments like real estate or major acquisitions.

However, for those who might fall just short of traditional bank standards, the U.S. Small Business Administration (SBA) offers guarantee programs. The SBA does not lend money directly; instead, it guarantees a portion of the loan made by a private lender, reducing the lender’s risk. The SBA 7(a) program is the most popular, providing versatile funding for working capital, equipment, and debt refinancing. The SBA 504 loan is specifically geared toward major fixed assets like land and buildings. While the application process for SBA loans is notoriously document-intensive and slow, the favorable terms make them a gold standard for small business finance.

Alternative Lending and Fintech Solutions

For businesses that need capital quickly or have less-than-perfect credit, the rise of Financial Technology (Fintech) has been a game-changer. Alternative lenders use advanced algorithms to assess “real-time” data—such as daily credit card sales or accounting software snapshots—rather than relying solely on legacy credit scores.

Common alternative products include:

- Lines of Credit: Similar to a credit card, you are approved for a maximum amount and only pay interest on what you draw. This is the ultimate tool for managing short-term cash flow gaps.

- Equipment Financing: The equipment itself serves as collateral for the loan. This is often easier to obtain because the lender can repossess the asset if the borrower defaults.

- Invoice Factoring: This allows you to sell your outstanding B2B invoices to a lender at a discount. It is an excellent way to unlock capital tied up in accounts receivable without taking on traditional debt.

The Documentation Powerhouse: Building Your Application

The difference between an approval and a rejection often lies in the quality of the documentation. A disorganized application suggests a disorganized business. To win over a loan officer, you must present a professional, data-driven narrative of your company.

Crafting a Compelling Business Plan

Even if you have been in business for years, many lenders require a formal business plan for significant loan amounts. This document should go beyond marketing fluff and focus on financial projections. It must include a market analysis, a description of the management team, and, most importantly, three to five years of projected financial statements (Balance Sheets, Income Statements, and Cash Flow Statements). Your projections should be “stress-tested”—meaning you should show how the business would handle a 10% or 20% dip in revenue while still servicing the debt.

Compiling Essential Financial and Legal Paperwork

Lenders will require a “loan package” that typically includes:

- Tax Returns: Usually the last three years of both personal and business federal returns.

- Profit and Loss (P&L) Statements: An up-to-date P&L, typically within the last 90 days.

- Bank Statements: Usually the last six to twelve months of business bank statements to verify cash flow.

- Legal Documents: This includes your articles of incorporation, business licenses, and any existing lease agreements or contracts with major suppliers.

Having these documents digitized and organized in a secure cloud folder allows you to respond to “additional information requests” (AIRs) from underwriters instantly, keeping the momentum of your application alive.

Navigating the Approval Process and Managing Repayment

Once you submit your application, it enters the underwriting phase. This is where the lender’s team verifies every claim made in your documentation. Understanding this phase can help you manage expectations and prepare for the final steps.

The Underwriting Process and Common Hurdles

During underwriting, the lender evaluates the “5 Cs of Credit”: Character, Capacity, Capital, Collateral, and Conditions.

- Character is your reputation and credit history.

- Capacity is your ability to repay.

- Capital is how much of your own money you have invested in the business (lenders don’t like to be the only ones taking a risk).

- Collateral is the assets you can pledge.

- Conditions refer to the external economic environment or industry-specific trends.

Expect follow-up questions. A lender might ask why revenue dipped in a specific month or request clarification on a large expense. Transparency is your best policy here. If there was a one-time setback, explain it clearly and show how you have corrected the course.

Strategic Debt Management Post-Funding

Getting the loan is only half the battle; managing it is where the real financial expertise comes in. Once the funds hit your account, it is vital to stick to your “Use of Funds” plan.

To maintain a healthy relationship with your lender and protect your financial future, consider these strategies:

- Automate Payments: Never miss a payment date. In the digital age, a single late payment can tank your credit score and trigger “default” interest rates.

- Monitor Your ROI: Track the revenue generated by the loan. If you borrowed $100,000 to buy inventory, that inventory should ideally generate enough profit to cover the interest and principal while adding to your bottom line.

- Communicate Early: If you foresee a cash flow crunch that might make a payment difficult, contact your lender before you miss the payment. Many lenders are willing to offer temporary interest-only periods or restructured terms for proactive borrowers.

Conclusion

Securing a small business loan is a transformative milestone for any enterprise. While the process may seem daunting, it is essentially a test of your business’s financial maturity. By meticulously preparing your credit profile, choosing the right lending product for your specific needs, and presenting a professional, data-backed application, you position your business as a low-risk, high-reward opportunity for lenders.

In the realm of money and business finance, capital is the fuel for the engine of innovation. Whether you are partnering with a local credit union or a cutting-edge Fintech platform, the key to success lies in preparation, transparency, and strategic management. With the right funding in place, your small business is no longer just surviving—it is positioned to thrive in an increasingly competitive marketplace.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.