Securing adequate car insurance is not merely a legal requirement in most places; it’s a fundamental pillar of sound personal finance. It acts as a financial safeguard against unforeseen events, protecting your assets and ensuring peace of mind on the road. Navigating the world of car insurance can seem complex, laden with jargon and numerous choices. However, by understanding the core principles, the acquisition process, and strategic cost-optimization techniques, you can effectively secure the right coverage without overextending your budget. This comprehensive guide aims to demystify the process, empowering you to make informed financial decisions when it comes to insuring your vehicle.

Understanding Car Insurance Fundamentals

Before diving into the specifics of how to purchase a policy, it’s crucial to grasp the foundational concepts of car insurance. This understanding forms the bedrock of making financially sound choices that align with your individual risk profile and budget.

Why Car Insurance is Essential (and Often Mandatory)

At its heart, car insurance is a contract between you and an insurance provider. In exchange for regular payments (premiums), the insurer agrees to cover financial losses stemming from specific events like accidents, theft, or damage. Its primary purpose is to protect you from potentially crippling financial liabilities that could arise from such incidents. Without insurance, a single accident could lead to thousands, if not tens of thousands, of dollars in medical bills, vehicle repairs, and potential legal fees, severely impacting your financial stability. From a societal perspective, mandatory insurance laws ensure that victims of accidents receive compensation, preventing a ripple effect of financial distress. From a personal finance standpoint, it’s an indispensable risk management tool, transferring significant potential financial burdens from your shoulders to that of the insurer.

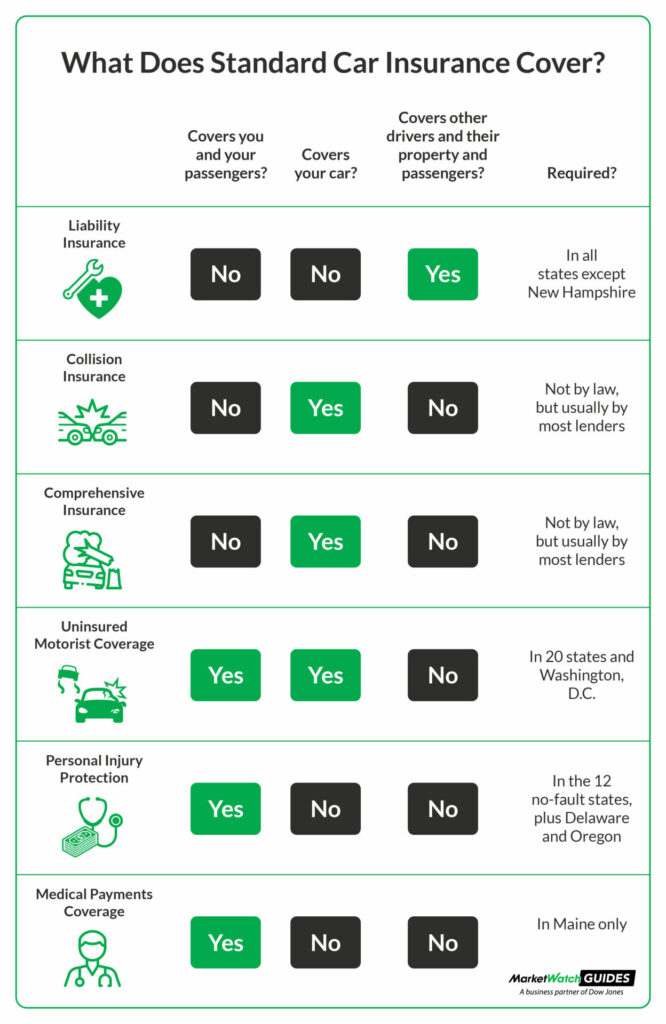

Key Types of Car Insurance Coverage

Understanding the various types of coverage is paramount for constructing a policy that offers robust financial protection. Each component serves a distinct purpose, and knowing these allows you to tailor your policy to your specific needs and local regulations.

- Liability Coverage: This is the most common and often legally required type. It covers damages and injuries you cause to other drivers, their passengers, or their property in an at-fault accident. It typically has two components: Bodily Injury Liability (for medical expenses, lost wages, and pain and suffering of others) and Property Damage Liability (for repairs or replacement of another person’s property). Financially, adequate liability coverage is critical; skimping here could expose your personal assets to lawsuits.

- Collision Coverage: This pays for damage to your vehicle resulting from a collision with another car or object, regardless of who is at fault. It’s particularly important for newer or more valuable cars, as repair or replacement costs can be substantial. Opting for collision coverage is a financial decision based on the value of your car versus the cost of the premium and your deductible.

- Comprehensive Coverage: This protects your car from damages not caused by a collision. This includes events like theft, vandalism, fire, natural disasters (hail, floods), and hitting an animal. For older cars with lower market value, the financial benefit of comprehensive coverage might diminish over time, making it a point of consideration during policy review.

- Personal Injury Protection (PIP) or Medical Payments (MedPay): These cover medical expenses for you and your passengers after an accident, regardless of fault. PIP can also cover lost wages and essential services. The necessity of these depends on your existing health insurance coverage and the laws in your state (“no-fault” states often require PIP).

- Uninsured/Underinsured Motorist (UM/UIM) Coverage: This protects you if you’re hit by a driver who has no insurance or insufficient insurance to cover your damages. Given the prevalence of uninsured drivers, this is a financially prudent addition to safeguard your own recovery costs.

Factors Influencing Your Insurance Premiums

Insurance premiums are not arbitrary; they are meticulously calculated based on a multitude of factors that assess your risk profile. Understanding these influences can help you anticipate costs and potentially make financially savvy adjustments.

- Driving Record: A clean driving history with no accidents or violations is the most significant factor in keeping premiums low. Insurers view a history of safe driving as a strong indicator of future low risk. Conversely, speeding tickets, DUIs, and at-fault accidents will dramatically increase your rates, reflecting a higher perceived risk.

- Vehicle Type: The make, model, year, safety features, and even the color of your car can affect premiums. High-performance, luxury, or frequently stolen vehicles typically command higher rates due to higher repair costs, greater theft risk, or increased likelihood of severe accidents. Cars with advanced safety features, on the other hand, might qualify for discounts.

- Location: Where you live and primarily drive influences your rates. Urban areas with higher traffic density, crime rates, and greater incidence of accidents or theft often lead to higher premiums than rural areas.

- Age and Gender: Younger, less experienced drivers, particularly males, generally face higher premiums due to statistical data indicating a greater propensity for accidents. As drivers age and gain experience, rates typically decrease until a certain point in older age where rates may begin to climb again.

- Credit Score (in some states): In many states, insurers use a credit-based insurance score as a predictor of how likely you are to file a claim. A higher credit score often correlates with lower premiums, highlighting the interconnectedness of overall financial health with insurance costs.

- Annual Mileage: The more you drive, the higher your chances of being in an accident. Low-mileage drivers may qualify for discounts.

The Step-by-Step Process to Secure Car Insurance

Obtaining car insurance involves a systematic approach, moving from information gathering to policy selection and final purchase. Approaching this process methodically ensures you receive competitive quotes and the right coverage.

Gathering Necessary Information

Before you even begin comparing quotes, compile all the pertinent data that insurers will require. This preparatory step streamlines the process and ensures accurate quotes. You’ll need:

- Personal Information: Your full name, date of birth, address, driver’s license number, and marital status. Details for all drivers who will be on the policy (e.g., family members).

- Vehicle Information: Make, model, year, Vehicle Identification Number (VIN), current odometer reading, anti-theft devices, and safety features. If you are financing or leasing the vehicle, the lender’s information will also be needed, as they often have specific coverage requirements.

- Driving History: Details of any accidents (at-fault or not-at-fault), moving violations (speeding tickets, DUIs), and claims filed in the past three to five years.

- Current Insurance Details: If you currently have insurance, having your policy number and current insurer’s name can be helpful, especially if you’re looking to switch providers.

Shopping Around and Comparing Quotes

This is perhaps the most financially impactful step. Never settle for the first quote you receive. The market is competitive, and prices for identical coverage can vary significantly between insurers.

- Online Aggregators: Websites like Policygenius, Compare.com, or TheZebra allow you to enter your information once and receive multiple quotes from various insurers simultaneously. This is an efficient way to get a broad overview of the market.

- Direct Insurers: Visit the websites of major insurance companies directly (e.g., Geico, Progressive, State Farm, Allstate, USAA). Sometimes, they offer exclusive online discounts or promotions not available through aggregators.

- Independent Agents: An independent insurance agent works with multiple insurance companies and can shop around on your behalf. They can provide personalized advice and often find competitive rates, especially for complex situations or specific niche coverage. Their expertise can be invaluable in understanding the financial implications of different policy structures.

- Captive Agents: Agents who work for a single insurance company (e.g., a State Farm agent). While they can only offer policies from their company, they often have deep knowledge of their products and can sometimes bundle policies for discounts.

When comparing quotes, ensure you are comparing apples to apples. The coverage limits, deductibles, and types of coverage must be identical across all quotes for a meaningful comparison. Pay close attention to the total annual or semi-annual premium.

Understanding Policy Details and Terms

Once you’ve received several quotes, don’t just look at the bottom line. Take the time to understand what you’re actually paying for.

- Declarations Page: This summary document outlines your coverage limits, deductibles, premium, policy period, and insured vehicles/drivers. It’s the most important part of your policy from a financial standpoint.

- Coverage Limits: These are the maximum amounts the insurer will pay for a covered loss. For liability, these are often expressed as three numbers (e.g., 100/300/50), representing $100,000 for bodily injury per person, $300,000 for bodily injury per accident, and $50,000 for property damage. Understand if these limits are sufficient to protect your assets in a worst-case scenario.

- Deductibles: This is the amount you must pay out-of-pocket before your insurance kicks in for collision and comprehensive claims. A higher deductible typically means a lower premium, but it also means a greater financial outlay if you need to file a claim. Choose a deductible that you can comfortably afford in an emergency.

- Exclusions: Be aware of what your policy doesn’t cover. For example, some policies exclude intentional damage or use of your personal vehicle for commercial purposes.

- Endorsements/Riders: These are optional additions that can enhance your coverage, such as roadside assistance, rental car reimbursement, or new car replacement. Evaluate their financial benefit versus their added cost.

Making the Purchase and Setting Up Payments

Once you’ve selected the policy that offers the best financial value and coverage for your needs, the final steps are straightforward.

- Confirm Details: Double-check all personal and vehicle information to avoid any discrepancies that could invalidate your policy later.

- Payment: You’ll typically have options for payment plans: monthly, quarterly, semi-annually, or annually. Paying annually or semi-annually often comes with a slight discount, offering a small but consistent financial saving. Set up automatic payments if possible to avoid lapses in coverage.

- Proof of Insurance: Upon purchase, you’ll receive proof of insurance (an ID card and policy documents). Keep this readily accessible in your vehicle, as it’s legally required when driving.

Strategies to Optimize Your Car Insurance Costs

Managing your car insurance costs effectively is an ongoing aspect of prudent personal finance. Several strategies can help you reduce your premiums without compromising essential coverage.

Maximizing Discounts

Insurance companies offer a plethora of discounts, and leveraging them is a direct path to lower premiums. Always inquire about all available discounts.

- Multi-Policy/Bundling Discount: Insurers often provide significant savings if you bundle your car insurance with other policies, such as home, renter’s, or life insurance. This is often one of the largest discounts available.

- Good Driver Discount: A history of safe driving over several years (e.g., 3-5 years without accidents or violations) can earn you a substantial discount.

- Defensive Driving Course Discount: Completing an approved defensive driving course can sometimes lead to a discount, especially for younger or older drivers.

- Good Student Discount: Students who maintain a certain GPA often qualify for discounts, recognizing their perceived lower risk.

- Low Mileage Discount: If you drive fewer miles than the average driver, you may be eligible for a discount.

- Vehicle Safety Features Discount: Cars equipped with anti-lock brakes, airbags, anti-theft devices, automatic seatbelts, or other advanced safety features often qualify for lower rates.

- Paid-in-Full Discount: Paying your entire premium upfront, rather than in installments, can sometimes lead to a small discount.

- Automatic Payment/Paperless Billing Discount: Signing up for automatic payments or choosing paperless billing can also result in minor savings.

Adjusting Deductibles and Coverage Limits

Strategic adjustments to your deductibles and coverage limits can significantly impact your premium.

- Increase Deductibles: Choosing a higher deductible for collision and comprehensive coverage means you’re taking on more financial risk if you file a claim, but it almost always results in a lower premium. Ensure your emergency fund can comfortably cover the chosen deductible.

- Review Coverage Limits: While it’s crucial to have adequate liability coverage, you might re-evaluate the need for maximum limits on collision and comprehensive coverage for older vehicles. If your car’s market value is low, the cost of these coverages might outweigh the potential payout after factoring in your deductible. A general rule of thumb is that if your annual premium for collision/comprehensive approaches 10% of your car’s market value, it might be financially prudent to drop it, especially if you have sufficient funds to replace the car yourself.

Improving Your Driving Record and Credit Score

These are long-term financial strategies that have a direct positive impact on your insurance premiums.

- Maintain a Clean Driving Record: This is the most effective way to keep your premiums low over time. Drive defensively, avoid speeding, and always adhere to traffic laws. Points on your license and accident records stay with you for several years, affecting rates.

- Improve Your Credit Score: As mentioned, credit-based insurance scores are used in many states. A healthy credit score (achieved through timely payments, low debt utilization, and a long credit history) can lead to lower insurance rates, underscoring the holistic nature of personal financial management.

Regular Policy Reviews and Re-shopping

Your insurance needs and the market itself are not static. Regular reviews are essential.

- Annual Policy Review: At least once a year, preferably before your policy renewal, review your coverage. Have your driving habits changed? Did you add safety features to your car? Has your car’s value depreciated significantly? Update your policy accordingly.

- Re-shop for Quotes: Don’t be afraid to get new quotes from other providers every year or two, even if you’re happy with your current insurer. Market rates fluctuate, and a competitor might offer a better deal, especially if your personal circumstances (e.g., age, marital status, credit score) have changed.

Common Pitfalls and Smart Financial Practices

Navigating car insurance also involves understanding potential traps and adopting financially smart behaviors.

Avoiding Underinsurance and Overinsurance

Striking the right balance is key.

- Underinsurance: Not having enough coverage, particularly liability, can leave your personal assets vulnerable in a major accident. The minimal legal requirements are often insufficient to cover severe damages or injuries. From a financial planning perspective, underinsurance is a significant risk.

- Overinsurance: Paying for coverage you don’t necessarily need, such as full collision and comprehensive on a very old car with low market value, is a waste of financial resources. Regularly assess if your coverage still makes financial sense relative to your car’s depreciation and your personal financial buffer.

Understanding Claims Processes and Their Financial Impact

Knowing how claims work is vital for managing your finances post-accident.

- Filing a Claim: Understand the steps involved and what information you’ll need. Prompt reporting is crucial.

- Impact on Premiums: Be aware that filing an at-fault claim will almost certainly lead to higher premiums at renewal. Consider if a small claim (below your deductible or just slightly above) might be better paid out-of-pocket to preserve your claims-free discount and keep future premiums low. This is a clear financial calculation.

- Diminished Value: In some cases, a repaired car may be worth less than it was pre-accident. Some policies or states allow for “diminished value” claims, which can be a financial recovery, but often requires legal guidance.

The Importance of Continuous Coverage

Lapses in car insurance coverage are financially detrimental.

- Legal Consequences: Driving without insurance carries severe penalties, including fines, license suspension, and vehicle impoundment.

- Higher Future Premiums: Insurers view a lapse in coverage as a higher risk indicator, leading to significantly higher premiums when you try to get insured again. Maintain continuous coverage to safeguard your financial profile with insurers.

Future Trends and Financial Planning for Car Insurance

The landscape of car insurance is continually evolving, with new technologies and societal shifts impacting how policies are priced and utilized. Integrating these trends into your long-term financial planning is increasingly important.

Impact of Telematics and Usage-Based Insurance

Telematics, devices or apps that monitor your driving behavior (speed, braking, mileage, time of day), are becoming more prevalent.

- Financial Incentive: Usage-Based Insurance (UBI) programs can offer significant discounts for safe drivers, sometimes up to 30% or more. If you are a consistently safe driver, opting into a UBI program can be a smart financial move.

- Privacy vs. Savings: This involves a trade-off between personal data privacy and potential financial savings. Evaluate if the discount outweighs your privacy concerns.

- Future Pricing Model: As technology advances, UBI could become a standard pricing model, making individual driving habits a direct and immediate factor in premiums.

Considering Electric Vehicles and Their Insurance Implications

The rise of Electric Vehicles (EVs) introduces new considerations for insurance.

- Repair Costs: EVs often have higher repair costs due to specialized components (e.g., battery packs) and the need for specialized technicians, which can initially translate to higher premiums.

- Theft Risk: Some EV models may have different theft profiles.

- Potential Discounts: As EVs become more mainstream and data accrues, insurers may offer specific discounts for EVs, recognizing their environmental benefits or certain safety aspects. Factor these potential costs and savings into your financial calculations when considering an EV purchase.

Integrating Car Insurance into Your Broader Financial Plan

Car insurance should not be viewed in isolation but as an integral part of your overall financial strategy.

- Budgeting: Allocate a consistent portion of your monthly budget for insurance premiums, alongside other fixed costs like housing and utilities.

- Emergency Fund: Ensure your emergency fund is robust enough to cover your deductibles in case of a claim, preventing a financial shock.

- Asset Protection: Understand that adequate car insurance, especially liability, is a critical component of protecting your overall net worth from potential lawsuits.

- Regular Review: Periodically assess all your insurance policies (car, home, life, health) to ensure they are still aligned with your current life stage, financial goals, and risk tolerance. As your assets grow, so too should your protective measures.

In conclusion, acquiring car insurance is more than just fulfilling a legal obligation; it’s a vital financial decision that safeguards your assets, manages risk, and provides peace of mind. By understanding the fundamentals, diligently comparing options, optimizing costs through strategic discounts and deductible choices, and integrating insurance into your broader financial plan, you can navigate the complexities effectively. Proactive management of your car insurance policy ensures that you are adequately protected while maintaining a healthy financial outlook.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.