In the lifecycle of almost every burgeoning enterprise, there comes a moment where organic growth is no longer sufficient to reach the next level. Whether it is expanding into a new market, purchasing inventory for a peak season, or investing in specialized equipment, external capital becomes the bridge between current operations and future potential. However, the process of securing a business loan is often perceived as a daunting labyrinth of paperwork, credit checks, and high-stakes negotiations.

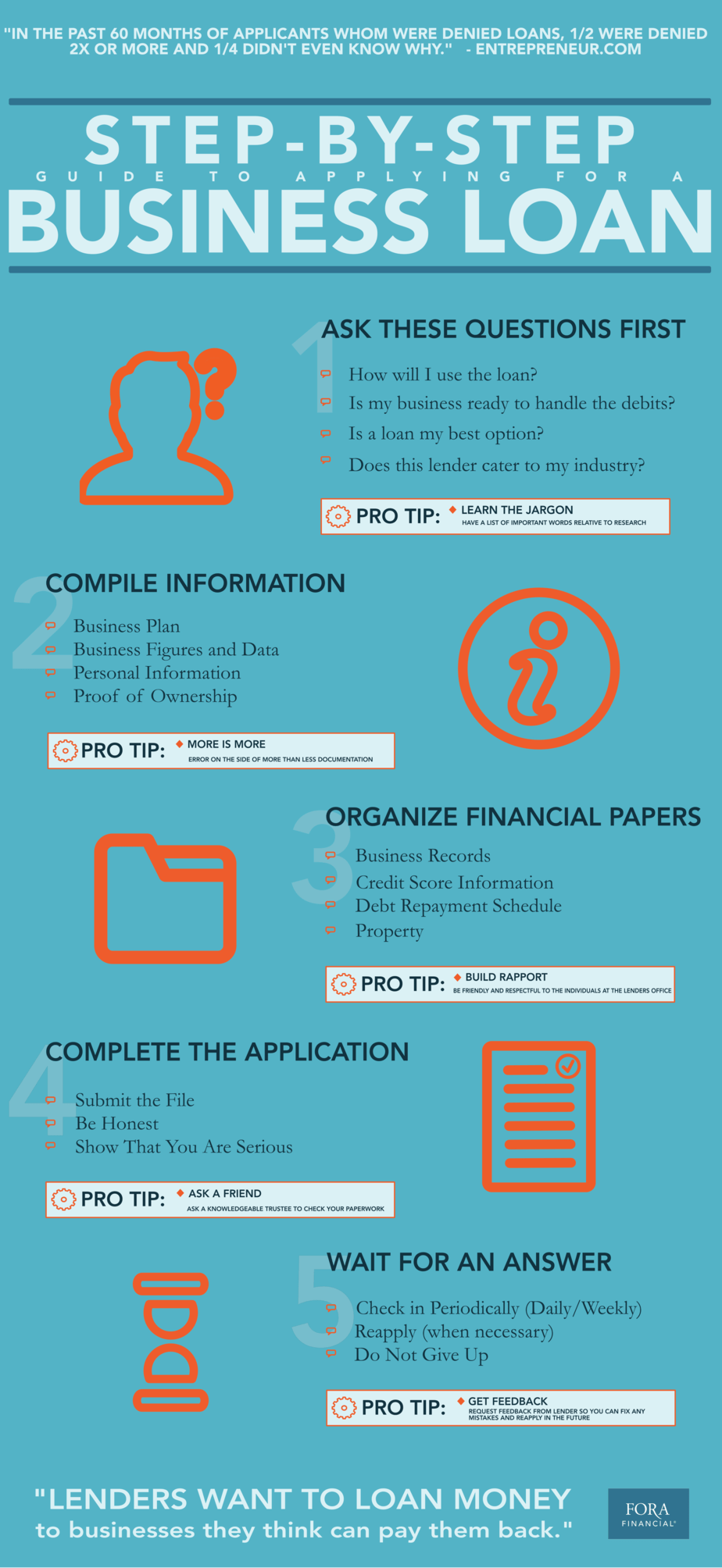

Securing a business loan is not merely a transaction; it is a rigorous test of your business’s financial health and your strategic foresight. To successfully navigate this process, entrepreneurs must move beyond the “need” for money and embrace the “readiness” for investment. This guide explores the comprehensive steps required to prepare, apply for, and secure the financing necessary to scale your business operations effectively.

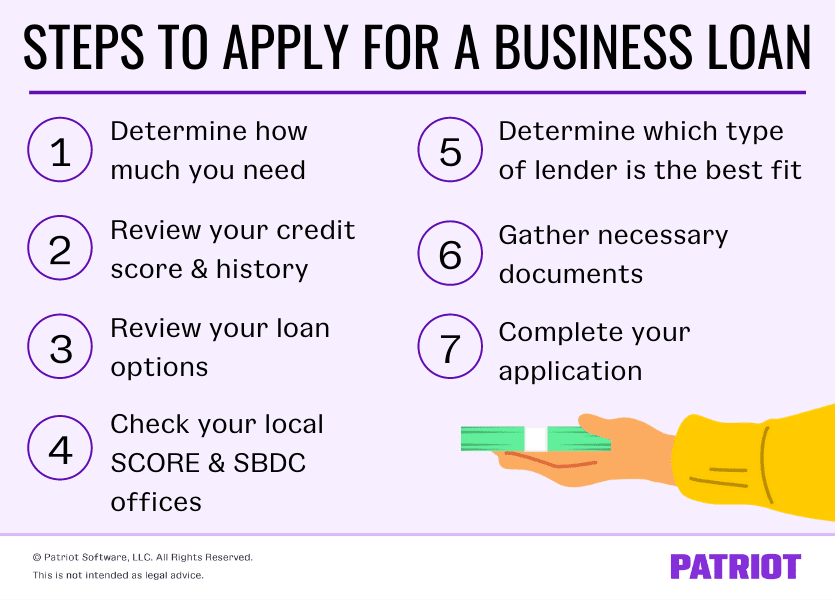

1. Preparing Your Financial Foundation

Before you ever step foot in a bank or open an online application, you must audit your own financial standing. Lenders do not provide capital based on potential alone; they provide it based on documented reliability. Preparation is the most critical phase of the loan process, as it dictates the interest rates you will receive and the amount of leverage you hold in negotiations.

Evaluating Your Credit Worthiness

For many small to mid-sized business owners, the line between personal and business credit is often blurred. Lenders will typically scrutinize your personal credit score (FICO) alongside your business credit report (Dun & Bradstreet, Experian Business). A personal credit score above 700 is generally considered the threshold for favorable terms. If your score is lower, you may need to spend several months paying down existing debt or correcting reporting errors before applying. A strong credit profile signals to the lender that you have a historical commitment to meeting financial obligations.

Defining the Purpose of the Loan

One of the most common reasons for loan rejection is a vague “use of proceeds.” Lenders want to know exactly how their capital will be deployed. Are you seeking working capital to manage cash flow gaps? Is this an expansion loan for a second location? Or is it equipment financing? Each of these purposes carries a different risk profile. Defining the “why” allows you to match your needs with the right type of financial product, ensuring you aren’t over-borrowing or choosing a high-interest short-term solution for a long-term project.

Organizing Essential Documentation

The documentation phase is where most applications stall. To maintain momentum, you should have a “loan-ready” digital folder containing the last three years of federal business and personal tax returns, year-to-date profit and loss (P&L) statements, and a current balance sheet. Additionally, you will likely need business licenses, articles of incorporation, and a debt schedule that lists any current outstanding liabilities. Having these ready demonstrates a level of professional organization that instills confidence in a loan officer.

2. Selecting the Right Lending Vehicle

Not all business loans are created equal. The financial landscape has evolved significantly over the last decade, moving from a bank-centric model to a diverse ecosystem of traditional, government-backed, and digital lenders. Choosing the right vehicle depends on your business’s age, your urgency, and your financial strength.

Traditional Commercial Banks

Traditional banks remain the gold standard for business financing due to their low interest rates and long repayment terms. However, they also have the strictest requirements. They typically look for businesses with at least two years of profitable history and significant collateral. If you have a long-standing relationship with a local community bank, this is often the best place to start, as they may be more willing to look at the “character” of the borrower rather than just the raw data.

SBA Loans (Small Business Administration)

The U.S. Small Business Administration does not lend money directly to entrepreneurs. Instead, it guarantees a portion of the loan made by partner lenders, reducing the risk for the bank. The SBA 7(a) and 504 loan programs are incredibly popular because they offer competitive rates and longer terms than most conventional loans. The trade-off is the bureaucratic nature of the application; SBA loans can take anywhere from 45 to 90 days to close and require exhaustive documentation.

Online Lenders and Fintech Solutions

For businesses that need capital quickly—sometimes within 24 to 48 hours—online lenders are a viable alternative. These institutions use proprietary algorithms to assess risk, often focusing more on real-time cash flow and social signals than traditional credit scores. While they offer speed and convenience, the “cost of capital” (interest rates and fees) is significantly higher. These are best used for short-term needs or for businesses that do not yet meet the rigorous criteria of traditional banks.

3. Developing a Compelling Business Case

When you apply for a loan, you are essentially selling the future of your company to a skeptic. The loan application is your pitch deck. To move from “pending” to “approved,” you must present a narrative that proves the loan will generate enough revenue to pay itself back with interest.

The Role of a Robust Business Plan

While you may have launched your business without a formal 50-page plan, many lenders—especially for larger loan amounts—require a written document. This plan should detail your market analysis, competitive advantage, management team experience, and marketing strategy. It proves that you aren’t just reacting to a cash shortage, but are proactively executing a strategy that requires capital as fuel.

Financial Projections and Cash Flow Analysis

Lenders are obsessed with “Debt Service Coverage Ratio” (DSCR). This is a measurement of the cash flow available to pay current debt obligations. You must provide forward-looking projections (pro-forma) that show how the loan will impact your bottom line. If you are borrowing $100,000 to buy a machine, show exactly how much more revenue that machine will produce monthly and how that revenue covers the new loan payment while leaving a safety margin.

Collateral and Personal Guarantees

In the world of business finance, “unsecured” loans are rare and expensive. Most lenders will require collateral—tangible assets like real estate, inventory, or accounts receivable—that can be seized if the loan defaults. Furthermore, most small business loans require a personal guarantee. This means you are personally liable for the debt if the business cannot pay. Understanding the implications of these requirements is essential for managing your personal risk.

4. Navigating the Underwriting and Closing Process

Once your application is submitted, it enters the “black box” of underwriting. This is the period where the lender’s risk department verifies every claim you have made. Understanding this phase can help you manage your expectations and respond effectively to “conditions” set by the lender.

The Five Cs of Credit

Underwriters generally use a framework known as the Five Cs to evaluate your application:

- Character: Your credit history and reputation.

- Capacity: Your ability to repay the loan based on cash flow.

- Capital: How much of your own money you have invested in the business.

- Collateral: The assets backing the loan.

- Conditions: The state of the economy and your specific industry.

Being aware of these allows you to address potential weaknesses in your application before the underwriter finds them.

Reviewing the Term Sheet

If the underwriter approves your loan, you will receive a term sheet or a commitment letter. This is not the final contract, but it outlines the “deal.” Pay close attention to more than just the interest rate. Look for “origination fees,” “prepayment penalties” (which charge you for paying off the loan early), and “covenants” (rules you must follow, such as maintaining a certain debt-to-equity ratio). Professionalism in this stage involves having your accountant or a legal professional review these terms to ensure they don’t stifle your future operational flexibility.

Managing the Funds and Relationship

Securing the loan is only the beginning. Once the funds are deposited, the focus shifts to stewardship. Maintaining a good relationship with your lender is vital for future financing needs. This means making payments on time, providing annual financial updates if required, and being transparent if the business hits a rough patch. A lender who trusts you is your greatest ally when you decide it’s time for the next round of growth capital.

Conclusion

Getting a business loan is a transformative milestone that requires a blend of financial literacy, meticulous preparation, and strategic storytelling. By treating the application process as an opportunity to tighten your internal financial controls and clarify your business goals, you do more than just secure a check—you build a foundation for sustainable, long-term success.

In the modern financial landscape, capital is available for those who can prove they know how to use it. Whether you opt for a traditional bank, an SBA-guaranteed loan, or a fast-paced fintech solution, the principles remain the same: know your numbers, understand your risks, and present a clear path to profitability. With the right approach, a business loan becomes the powerful catalyst that turns your entrepreneurial vision into a market-leading reality.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.