For small business owners, securing adequate funding is often the critical determinant of success, growth, and even survival. While traditional bank loans can be challenging to obtain, particularly for startups or businesses without extensive collateral, Small Business Administration (SBA) loans offer a lifeline. Backed by the U.S. government, SBA loans mitigate risk for lenders, making it easier for small businesses to access capital with more favorable terms. Navigating the application process, however, requires a clear understanding of the requirements, types of loans available, and the steps involved. This comprehensive guide will demystify the process, providing a roadmap to successfully acquiring an SBA loan and unlocking your business’s full potential.

Understanding SBA Loans: A Gateway to Business Growth

Before embarking on the application journey, it’s crucial to grasp what an SBA loan entails, its various forms, and the distinct advantages it offers over conventional financing options.

What is an SBA Loan?

An SBA loan is a small business loan partially guaranteed by the U.S. Small Business Administration. The SBA itself does not directly lend money to businesses (with the exception of disaster loans). Instead, it sets guidelines for loans, which are then made by its network of participating lenders, including banks, credit unions, and non-profit organizations. The government guarantee reduces the risk for these lenders, encouraging them to provide financing to small businesses that might not otherwise qualify for a traditional loan. This structure allows for more flexible terms, lower down payments, and often more competitive interest rates than other commercial loans.

The Different Types of SBA Loans

The SBA offers a suite of loan programs tailored to various business needs, each with its own specific criteria and maximum loan amounts. Understanding these distinctions is key to choosing the right fit for your business:

- SBA 7(a) Loan Program: This is the SBA’s most popular and versatile loan program. It can be used for a wide range of purposes, including working capital, purchasing inventory or equipment, real estate acquisition, business acquisition, or refinancing existing debt. Loan amounts can go up to $5 million, with flexible terms stretching up to 25 years for real estate.

- SBA 504 CDC/Express Loan Program: Designed for fixed asset financing, the 504 program provides long-term, fixed-rate financing for major fixed assets like land and buildings, new construction, or renovating existing facilities. It’s ideal for businesses looking to expand and create jobs. Loans can go up to $5 million (with potential for more for energy-efficient projects), typically structured with three parties: the borrower, a Certified Development Company (CDC), and a third-party lender.

- SBA Microloan Program: These smaller loans, typically up to $50,000, are provided through intermediary lenders to help small businesses and certain non-profit childcare centers start or expand. Funds can be used for working capital, inventory, supplies, furniture, fixtures, machinery, and equipment. The program also provides business counseling and technical assistance to borrowers.

- Disaster Loans: While not part of the standard business financing suite, the SBA also offers low-interest disaster loans to businesses and homeowners located in declared disaster areas. These loans help repair or replace damaged property and can provide working capital to offset economic injury caused by a disaster.

Key Benefits of SBA Financing

SBA loans present several compelling advantages that make them a preferred financing option for many small businesses:

- Lower Down Payments: Compared to conventional loans, SBA loans often require a smaller upfront capital contribution from the borrower, freeing up cash for other operational needs.

- Longer Repayment Terms: Extended repayment periods translate to lower monthly payments, improving cash flow and reducing the financial burden on the business.

- Competitive Interest Rates: The government guarantee allows lenders to offer more attractive interest rates, often pegged to the prime rate plus a modest spread.

- Flexible Use of Funds: Particularly with the 7(a) program, funds can be utilized for a broad spectrum of business needs, offering versatility to the borrower.

- Accessibility for Startups and Growing Businesses: SBA loans bridge the gap for businesses that might not meet the stringent criteria of traditional lenders due to limited operating history or collateral.

Eligibility and Preparation: Laying the Groundwork

Once you’ve identified the most suitable SBA loan program, the next critical step is to assess your eligibility and meticulously prepare all necessary documentation. This foundational work significantly streamlines the application process and enhances your chances of approval.

General Eligibility Requirements

While specific requirements vary by loan program, several universal criteria apply to most SBA loans:

- Small Business Definition: Your business must meet the SBA’s definition of a small business, which is primarily based on industry-specific size standards related to average annual revenue or number of employees.

- For-Profit Status: The business must be operating for profit.

- U.S. Operations: It must conduct business in the U.S. or its possessions.

- Owner Equity: The owner(s) must have invested their own equity into the business.

- Inability to Obtain Credit Elsewhere: Generally, businesses must demonstrate that they have tried and failed to obtain financing on reasonable terms through other conventional lenders without an SBA guarantee.

- Sound Business Purpose: The loan proceeds must be used for a sound business purpose.

- Good Character: Owners and key management must demonstrate good character, often assessed through personal credit scores and criminal background checks.

Essential Documents for Your Application

A complete and well-organized application package is paramount. While specific lender requests may vary, be prepared to provide:

- Business Plan: A comprehensive plan detailing your business operations, market analysis, management team, financial projections, and how the loan will be used. This is often the most critical document.

- Financial Statements: This includes personal financial statements for all owners (typically those owning 20% or more), and business financial statements (balance sheets, income statements for the past three years, and year-to-date statements).

- Personal and Business Tax Returns: Usually, three years of federal tax returns for both the business and its principals.

- Credit Reports: Personal and business credit reports will be pulled by the lender.

- Business Legal Documents: Articles of incorporation, partnership agreements, business licenses, and registrations.

- Resumes: For all principal owners and key management, highlighting relevant experience.

- Use of Proceeds Statement: A detailed breakdown of exactly how the loan funds will be utilized.

- Collateral: Documentation of any assets available as collateral (e.g., real estate, equipment, accounts receivable).

Crafting a Compelling Business Plan

Your business plan is more than just a formality; it’s your pitch to the lender. A robust plan demonstrates your understanding of your market, your operational strategy, and your financial viability. Ensure it includes:

- Executive Summary: A concise overview of your entire plan.

- Company Description: What your business does, its mission, and its structure.

- Market Analysis: Industry overview, target market, and competitive analysis.

- Organization & Management: Who runs the business and their qualifications.

- Service or Product Line: Detailed description of what you offer.

- Marketing & Sales Strategy: How you will reach and sell to customers.

- Funding Request: How much you need, how you’ll use it, and repayment projections.

- Financial Projections: Forecasts of income statements, balance sheets, and cash flow for at least three to five years. Clearly articulate how the loan will improve these projections.

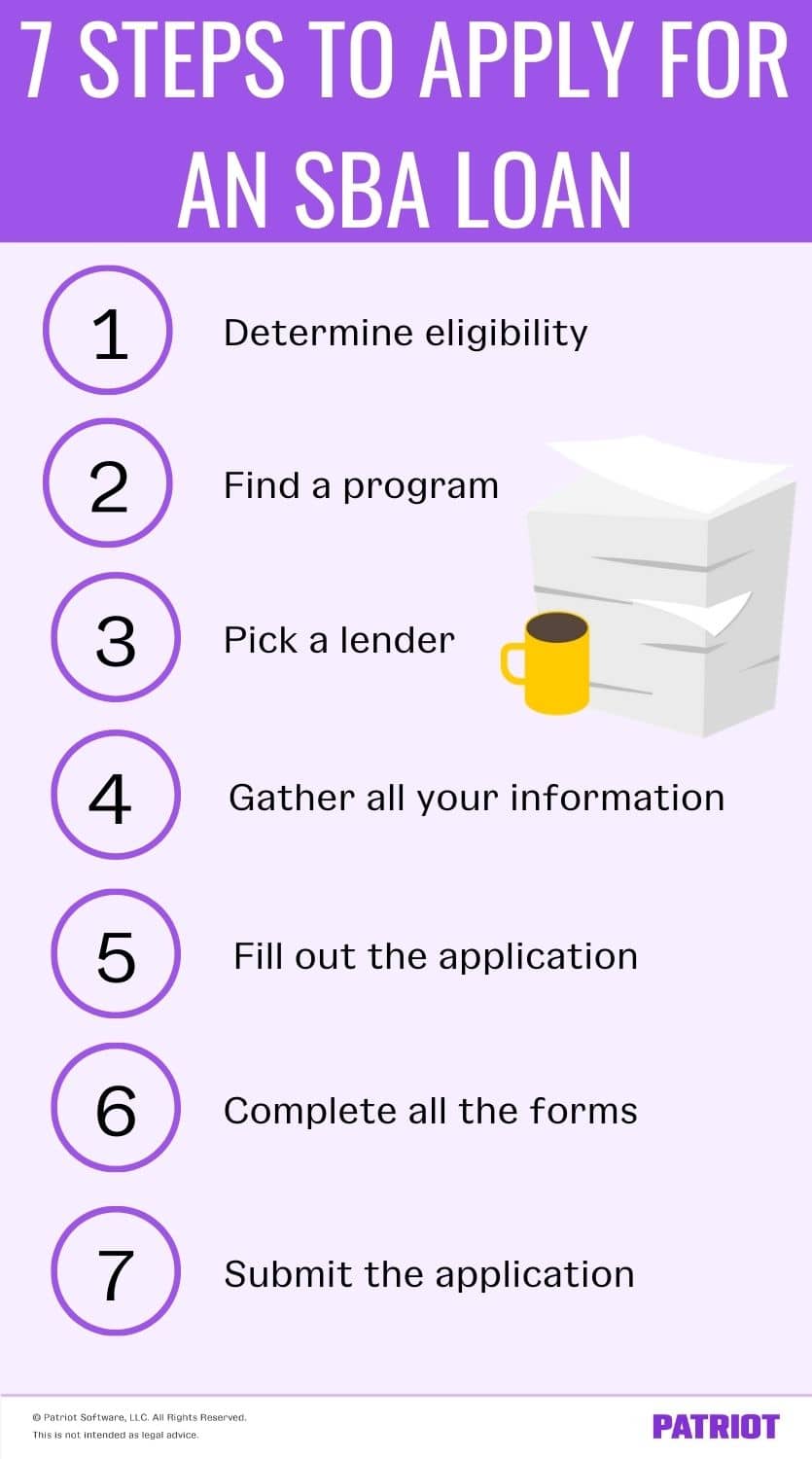

The Application Process: Step-by-Step Guidance

With your eligibility confirmed and documents in order, you are ready to formally apply. The process involves identifying a suitable lender, submitting your comprehensive package, and navigating the underwriting phase.

Finding the Right Lender

Unlike traditional loans where you approach a bank directly, with SBA loans, you’re looking for a bank that participates in SBA lending programs. Not all banks are equally versed or aggressive in SBA lending.

- Utilize the SBA’s Lender Match Tool: The SBA offers an online tool to connect businesses with participating lenders.

- Research Experienced Lenders: Look for banks, credit unions, or non-bank lenders that have a strong track record and expertise in specific SBA loan programs (e.g., a bank specializing in 7(a) loans for real estate).

- Consider Local vs. National Banks: Local banks might offer more personalized service, while larger national banks often have dedicated SBA departments and streamlined processes.

- Interview Prospective Lenders: Don’t hesitate to speak with multiple lenders to compare their terms, fees, and their understanding of your business needs.

Submitting Your Application Package

Once you’ve selected a lender, they will guide you through their specific application forms. This will involve submitting all the prepared documentation. Be prepared for potential follow-up questions or requests for additional information.

- Be Thorough and Accurate: Double-check all information for accuracy and completeness. Errors or omissions can cause significant delays or even rejection.

- Maintain Open Communication: Respond promptly to any requests from your lender. Proactive communication demonstrates your commitment and organization.

- Stay Organized: Keep copies of everything you submit. Create a system to track documents and communications.

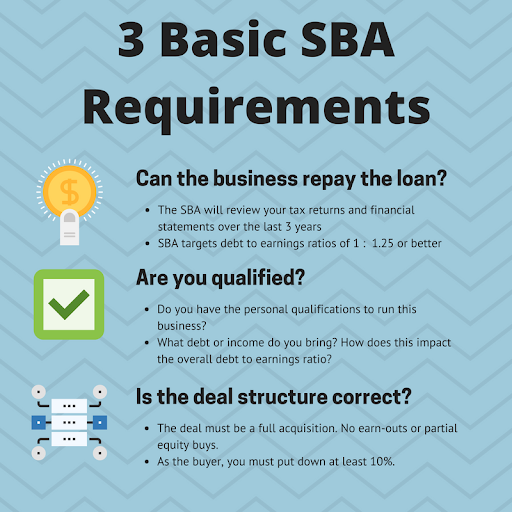

The Underwriting Process and Approval

After submission, your application enters the underwriting phase. The lender will meticulously review your business plan, financial statements, credit history, and personal background. They are assessing:

- Creditworthiness: Both personal and business credit scores are crucial.

- Capacity to Repay: Your projected cash flow and historical financial performance will be scrutinized to ensure you can comfortably service the debt.

- Collateral: While SBA loans are government-guaranteed, lenders still prefer to secure loans with available collateral.

- Character: Your personal and professional history will be evaluated.

- Conditions: The economic climate and industry-specific factors will also play a role.

If the lender approves your application, they will then submit it to the SBA for final review and approval of the guarantee. Once both the lender and the SBA give the green light, you will proceed to loan closing, where you’ll sign the necessary paperwork and the funds will be disbursed according to the agreed-upon terms.

Post-Approval and Loan Management: Maximizing Your Investment

Receiving an SBA loan is a significant milestone, but it’s just the beginning. Effective management of these funds and adherence to loan terms are crucial for long-term business health and financial credibility.

Understanding Loan Terms and Conditions

Upon approval, you will receive a loan agreement detailing all terms and conditions. It is imperative to read and understand every clause, particularly concerning:

- Interest Rate and Payment Schedule: Know your fixed or variable rate, how interest is calculated, and your exact monthly payment due dates.

- Covenants: These are promises made to the lender, such as maintaining certain financial ratios, providing regular financial reports, or refraining from taking on additional debt without permission.

- Reporting Requirements: Be aware of any ongoing financial reporting obligations to your lender or the SBA.

- Default Triggers: Understand what constitutes a default on your loan and the potential consequences.

Effective Use of Funds

SBA loans come with a defined “use of proceeds.” Diverting funds for purposes not approved in your application can lead to serious issues.

- Stick to Your Business Plan: Use the loan specifically for the purposes outlined in your successful application, whether it’s for equipment purchase, working capital, or real estate.

- Track Expenditures Meticulously: Maintain clear records of how every dollar is spent. This not only ensures compliance but also aids in financial management and future planning.

- Prioritize Investments: Focus on uses that will generate a strong return on investment for your business, driving growth and ensuring loan repayment.

Maintaining Good Standing with Your Lender

Building and maintaining a positive relationship with your lender is invaluable.

- Prompt Payments: Always make your loan payments on time. This is the simplest and most effective way to demonstrate financial responsibility.

- Proactive Communication: If you anticipate any financial challenges or changes in your business that might affect your ability to repay, communicate proactively with your lender. They may be able to offer solutions or adjustments.

- Regular Reporting: Fulfill all reporting requirements accurately and on schedule. This transparency builds trust and can lead to easier access to future financing if needed.

Common Pitfalls and Expert Tips for Success

While the path to an SBA loan is well-defined, it’s not without its challenges. Being aware of common mistakes and leveraging professional advice can significantly smooth your journey.

Avoiding Common Application Mistakes

- Incomplete or Inaccurate Applications: The most frequent reason for delays or rejections. Double-check everything.

- Weak Business Plan: A poorly constructed plan that lacks clear projections or a sound strategy will raise red flags.

- Poor Credit History: Both personal and business credit scores are critical. Address any issues before applying.

- Underestimating Collateral: While guaranteed, lenders still look for collateral. Be transparent about what you can offer.

- Lack of Equity Injection: The SBA and lenders want to see that owners have ‘skin in the game.’

- Choosing the Wrong Loan Program: Applying for a program that doesn’t align with your needs wastes time and effort.

Leveraging Professional Advice

- SBA Resource Partners: Organizations like Small Business Development Centers (SBDCs), SCORE mentors, and Women’s Business Centers offer free or low-cost counseling and assistance with business planning and loan applications.

- Financial Advisors/Accountants: These professionals can help you prepare accurate financial statements and projections, which are crucial for the application.

- SBA Loan Brokers: While they charge a fee, experienced brokers can help you navigate the process, match you with the right lender, and strengthen your application.

The Long-Term Vision with SBA Financing

Securing an SBA loan is more than just obtaining capital; it’s an investment in your business’s future. By adhering to the terms, effectively utilizing the funds, and maintaining a solid financial standing, you build a foundation for sustained growth. An SBA loan can provide the runway for expansion, new product development, increased market reach, and ultimately, greater profitability and long-term success. Treat it as a strategic partnership that empowers your entrepreneurial journey.

Securing an SBA loan can be a transformative step for any small business. While the process demands diligence and meticulous preparation, the potential benefits—access to capital, favorable terms, and a strengthened financial foundation—make the effort worthwhile. By understanding the types of loans available, meeting eligibility requirements, carefully preparing your application, and responsibly managing the funds, you can effectively leverage this powerful financial tool to achieve your business aspirations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.