Securing a business loan is often a pivotal step for entrepreneurs, whether they’re launching a nascent startup, orchestrating a significant expansion, or simply managing the day-to-day ebb and flow of working capital. In the dynamic world of commerce, access to capital can be the decisive factor between stagnation and growth. However, navigating the labyrinthine landscape of business financing can feel overwhelming, with a myriad of options, stringent requirements, and complex terminologies. This comprehensive guide aims to demystify the process, providing a clear roadmap for business owners to successfully acquire the funding they need to thrive. We’ll delve into understanding your financial requirements, exploring the diverse range of loan products available, meticulously preparing your application, and expertly navigating the approval process.

Understanding Your Business Loan Needs

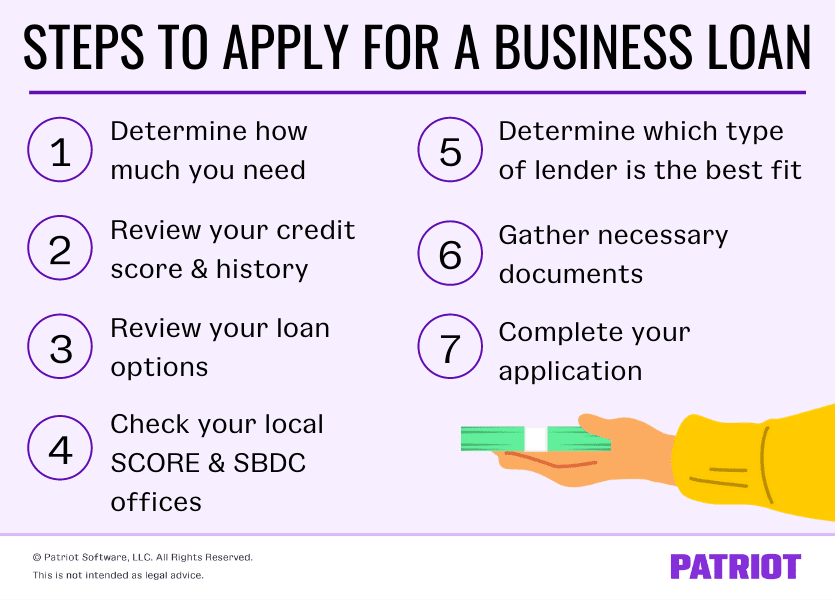

Before you even begin to explore potential lenders, the most critical first step is to gain absolute clarity on your own business’s financial standing and, more importantly, the specific purpose and scope of the loan you seek. A well-defined need will guide your search, influencing the type of loan, the amount, and the terms you should pursue.

Why Do You Need a Loan?

The motivation behind seeking a business loan can be incredibly diverse, each requiring a tailored financial solution. Are you looking to:

- Launch a Startup? New businesses often require seed capital for initial operations, inventory, marketing, and essential equipment before revenue streams stabilize. Lenders will focus heavily on your business plan and personal credit.

- Fund Business Expansion? Growing businesses might need capital to open new locations, hire additional staff, invest in larger production facilities, or penetrate new markets. Here, track record and projected growth are key.

- Purchase Equipment or Machinery? Specialized equipment, from industrial machinery to state-of-the-art office technology, can be a significant upfront cost. Equipment loans or leases are designed for this specific purpose, often using the equipment itself as collateral.

- Manage Working Capital? Businesses often face periods of uneven cash flow. A working capital loan can bridge gaps, ensuring you can cover operational expenses, payroll, or inventory purchases during slower seasons or before large invoices are paid.

- Buy Inventory? For retail or manufacturing businesses, maintaining adequate inventory levels is crucial. An inventory loan can help stock up without tying up existing cash flow.

- Consolidate Debt? If your business has multiple high-interest debts, a consolidation loan can simplify repayment and potentially reduce overall interest costs.

Clearly defining the “why” will help you articulate your case to lenders and narrow down your financing options.

How Much Capital Do You Require?

Once you’ve identified the purpose, the next logical step is to quantify the exact amount of capital needed. This isn’t a figure to pluck from thin air; it requires meticulous financial forecasting. Overestimating can lead to unnecessary interest payments, while underestimating can leave you short-changed and necessitate another funding round soon after.

- Detailed Cost Analysis: Break down all the expenses related to your loan’s purpose. For expansion, include property costs, renovation, new equipment, hiring, training, and increased operational overhead for a specific period (e.g., 6-12 months).

- Contingency Planning: Always factor in a buffer for unforeseen expenses, typically 10-20% of your total estimated costs.

- Financial Projections: Develop realistic financial projections, including cash flow statements, profit and loss forecasts, and balance sheets for the next 3-5 years. These projections should demonstrate how the loan will generate sufficient revenue to cover its repayment.

What’s Your Repayment Capacity?

Lenders are primarily concerned with one thing: your ability to repay the loan. They will scrutinize your business’s current and projected cash flow to assess its capacity to meet monthly loan obligations.

- Cash Flow Analysis: Provide historical cash flow statements that demonstrate a consistent ability to generate positive cash flow. For startups, robust projections will be crucial.

- Debt-Service Coverage Ratio (DSCR): Lenders use this metric to evaluate your ability to cover debt payments. It’s calculated by dividing your net operating income by your total debt service (principal and interest payments). A DSCR of 1.25 or higher is generally considered favorable, indicating you have 1.25 times the income needed to cover your debt payments.

- Personal Financials: For smaller businesses, especially startups, lenders will often evaluate the owner’s personal financial health, including personal credit score, assets, and liabilities, as a backup repayment source.

Exploring Different Types of Business Loans

The financial market offers a diverse ecosystem of loan products, each designed to serve different business needs and risk profiles. Understanding these categories is crucial for selecting the most appropriate funding source.

Traditional Bank Loans

Banks remain a cornerstone of business financing, offering a range of structured products. They are often perceived as more stable and typically offer lower interest rates than alternative lenders, but their approval processes can be more rigorous and time-consuming.

- Term Loans: These are perhaps the most common type, providing a lump sum of capital that is repaid over a fixed period (e.g., 1-5 years for short-term, 5-25 years for long-term) with regular, fixed-rate payments. They are suitable for significant capital expenditures like equipment purchases or major expansions.

- Lines of Credit: Similar to a credit card for your business, a line of credit offers flexible access to funds up to a set limit. You only pay interest on the amount you draw, making it ideal for managing working capital fluctuations or unforeseen expenses. It’s revolving, meaning as you repay, the funds become available again.

- SBA Loans (Small Business Administration): In the United States, the SBA guarantees a portion of loans made by traditional lenders, reducing risk for banks and making it easier for small businesses to qualify. These loans (like the 7(a) loan or CDC/504 loan for real estate and equipment) often feature lower down payments, longer repayment terms, and competitive interest rates, making them highly desirable but also competitive to secure.

Alternative Lenders and Online Platforms

The rise of financial technology (FinTech) has revolutionized the lending landscape, introducing a plethora of alternative options, often characterized by faster application processes and more flexible eligibility criteria, albeit sometimes at a higher cost.

- Online Lenders: These platforms leverage technology to streamline the application and approval process, often providing funding within days. They are a good option for businesses that need quick access to capital or those who might not qualify for traditional bank loans due to shorter operating histories or lower credit scores. Examples include Kabbage, OnDeck, and Funding Circle.

- Merchant Cash Advances (MCAs): Instead of a traditional loan, an MCA provides an upfront sum in exchange for a percentage of future credit card sales. While fast and accessible even to businesses with poor credit, MCAs can be very expensive, with effective APRs often reaching triple digits. They are generally considered a last resort.

- Peer-to-Peer (P2P) Lending: Platforms like Prosper or LendingClub connect borrowers directly with individual investors willing to fund their loans. These can offer more competitive rates than MCAs for businesses with good credit, but the funding process can vary.

Niche Funding Options

Beyond the broad categories, specialized financing options cater to specific business needs.

- Equipment Financing: These loans are specifically for purchasing machinery or equipment. The equipment itself typically serves as collateral, making it easier to qualify and often offering favorable terms.

- Invoice Factoring/Financing: If your business has a lot of outstanding invoices, factoring allows you to sell them to a third party (a factor) at a discount in exchange for immediate cash. Invoice financing, a variation, allows you to borrow against your invoices while still managing collections. This is excellent for businesses with long payment cycles.

- Microloans: Offered by non-profit organizations or specialized lenders, microloans are small loans (typically under $50,000) designed for startups and small businesses, often in underserved communities. They may come with business support and mentorship.

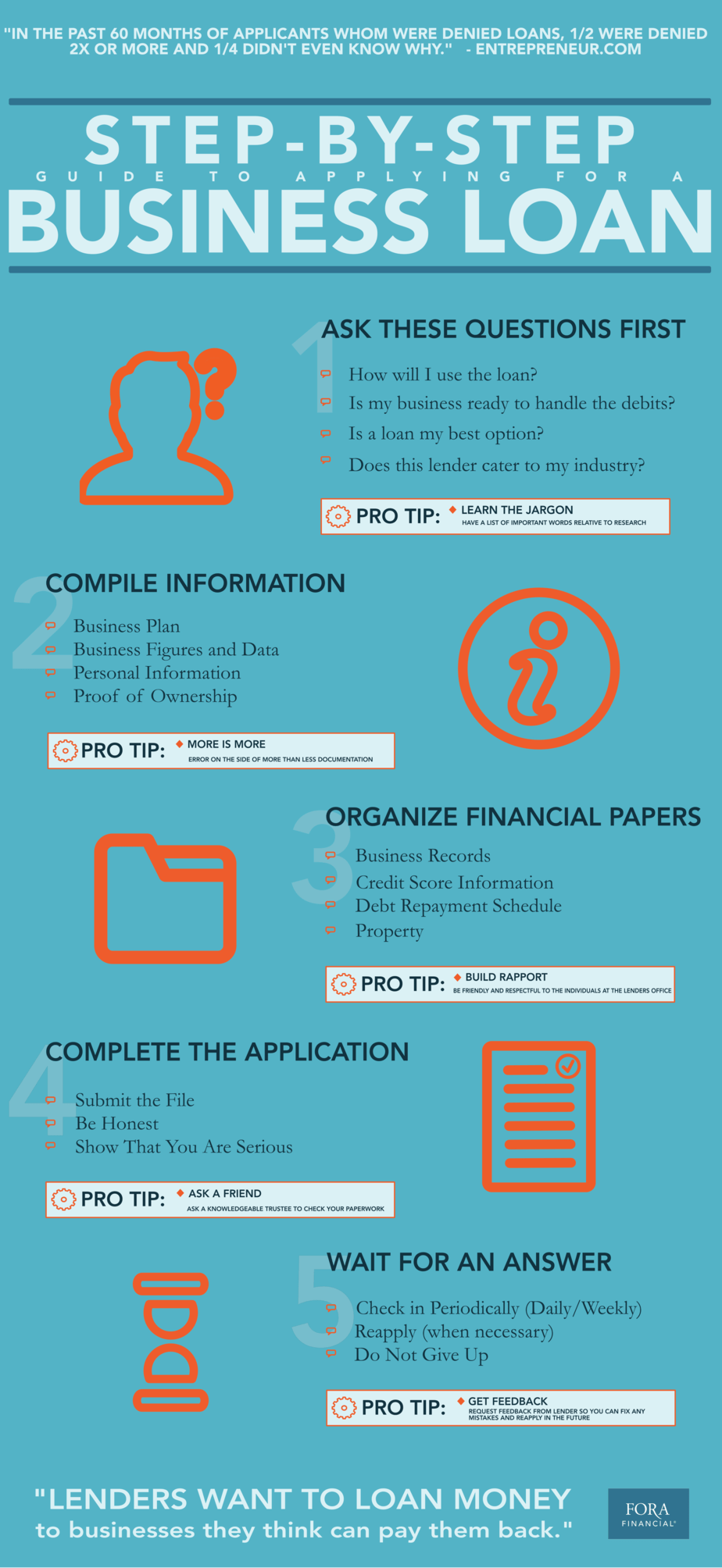

Preparing Your Loan Application: The Essentials

Regardless of the lender or loan type, thorough preparation is paramount. A well-organized, comprehensive application significantly increases your chances of approval. Lenders are looking for signs of stability, trustworthiness, and a clear repayment strategy.

Develop a Robust Business Plan

A compelling business plan is your opportunity to tell your story and demonstrate your vision. It convinces lenders that your business is viable and capable of sustained growth and repayment. Key components include:

- Executive Summary: A concise overview of your entire plan, highlighting key points.

- Company Description: What your business does, its mission, legal structure, and competitive advantages.

- Market Analysis: In-depth research on your target market, industry trends, competition, and how your business fits in.

- Organization and Management: Who runs the business, their experience, and the organizational structure.

- Service or Product Line: Detailed description of what you sell, its unique value proposition, and intellectual property (if any).

- Marketing and Sales Strategy: How you plan to reach customers and generate sales.

- Financial Projections: Crucial for lenders, including historical financial data (if applicable), profit and loss statements, balance sheets, cash flow projections, and a clear breakdown of how the loan funds will be used and repaid.

- Funding Request: Exactly how much you’re asking for and for what purpose.

Organize Your Financial Documents

Lenders require a clear snapshot of your business’s financial health. Prepare a well-organized portfolio of documents:

- Business Bank Statements: Typically for the last 6-12 months.

- Business Tax Returns: For the past 2-3 years.

- Profit & Loss (P&L) Statements: Also known as Income Statements, for the last 2-3 years and year-to-date.

- Balance Sheets: Detailing assets, liabilities, and owner’s equity for the last 2-3 years and year-to-date.

- Cash Flow Statements: Showing the movement of cash in and out of your business.

- Accounts Receivable and Payable Aging Reports: If applicable, to show outstanding invoices and bills.

- Personal Tax Returns: For the past 2-3 years, especially for small businesses.

- Personal Financial Statement: An overview of the owner’s assets, liabilities, and net worth.

- Legal Documents: Business licenses, registrations, articles of incorporation, and any relevant contracts or leases.

Understand Your Credit Score(s)

Both your personal and business credit scores play a significant role in loan approval and the interest rate you receive.

- Personal Credit Score: Lenders, especially for small businesses and startups, will evaluate your FICO score. A score of 680+ is generally considered good, while 720+ is excellent. Ensure your personal credit is in good standing by checking for errors and paying bills on time.

- Business Credit Score: Established businesses will have a separate business credit score (e.g., from Dun & Bradstreet, Experian Business, Equifax Business). This score reflects your business’s payment history with vendors, suppliers, and other creditors. Actively building good business credit by establishing trade lines and paying on time is crucial.

Have Collateral or a Personal Guarantee Ready

Many business loans, particularly traditional ones, require some form of security.

- Collateral: This refers to assets you pledge to the lender that they can seize if you default on the loan. Common forms include real estate, equipment, inventory, or accounts receivable. The presence of valuable collateral significantly reduces the lender’s risk.

- Personal Guarantee: For many small business loans, particularly when collateral is scarce or insufficient, lenders will require a personal guarantee from the business owner. This means you are personally liable for the loan if your business cannot repay it, putting your personal assets at risk.

Navigating the Application Process and Beyond

With your preparations complete, it’s time to engage with lenders and manage the application process through to fruition. This stage demands careful comparison, clear communication, and diligent follow-up.

Research and Compare Lenders

Don’t settle for the first offer. Different lenders specialize in different areas, and their terms, rates, and eligibility requirements can vary significantly.

- Interest Rates and Fees: Compare the Annual Percentage Rate (APR), which includes all interest and fees, to get a true cost of the loan. Look out for origination fees, closing costs, and prepayment penalties.

- Loan Terms: Understand the repayment schedule, the length of the loan, and whether the interest rate is fixed or variable.

- Eligibility Requirements: Ensure your business meets the lender’s criteria for revenue, time in business, and credit scores.

- Lender Reputation and Customer Service: Read reviews and speak to other business owners about their experiences. A responsive and helpful lender can be invaluable.

- Funding Speed: If time is of the essence, prioritize lenders known for quick turnaround times, such as online lenders, but be mindful of potential higher costs.

Submit a Comprehensive Application

Once you’ve chosen a few potential lenders, tailor your application to each one’s specific requirements.

- Accuracy and Completeness: Double-check every piece of information for accuracy. Incomplete or incorrect applications are a common reason for delays or rejections.

- Tailored Approach: While your core documents remain the same, customize your cover letter and perhaps even parts of your business plan to address specific interests or concerns of each lender.

- Professional Presentation: Ensure all documents are clearly labeled, easy to read, and presented professionally.

Be Prepared for Due Diligence

After submission, lenders will perform their due diligence. This often involves:

- Interviews: You may be asked to meet with loan officers to discuss your business plan, financial projections, and your understanding of the market. Be articulate, confident, and knowledgeable.

- Additional Document Requests: Be ready to provide further documentation or clarifications as requested. Responsiveness demonstrates your commitment and organization.

- Site Visits: For larger loans or certain industries, a lender might conduct a physical visit to your business premises to assess operations and collateral.

Understanding Loan Agreements

If your application is approved, you’ll receive a loan agreement. Do not sign anything without fully understanding every clause.

- Terms and Conditions: Review the principal amount, interest rate, repayment schedule, and any associated fees.

- Covenants: These are conditions that you must abide by throughout the loan term, such as maintaining certain financial ratios, providing regular financial statements, or restrictions on taking on additional debt. Violating covenants can lead to default.

- Default Provisions: Understand what constitutes a default and the penalties involved.

- Legal Counsel: Consider having an attorney review the agreement to ensure it protects your interests and clarifies any ambiguous language.

Building a Strong Relationship with Your Lender

A successful loan application isn’t the end of the journey; it’s the beginning of a relationship.

- Maintain Open Communication: Keep your lender informed about significant changes in your business, positive or negative.

- Consistent Repayment: Always make your payments on time. This builds trust and strengthens your business credit, paving the way for future financing needs.

- Future Opportunities: A strong relationship with a lender can open doors to more favorable terms for future loans, credit lines, or financial advice.

In conclusion, securing a business loan is a strategic process that demands diligence, foresight, and a comprehensive understanding of your business’s financial health. By meticulously preparing your application, exploring the right funding avenues, and engaging intelligently with lenders, you can successfully acquire the capital needed to fuel your business’s growth and achieve your entrepreneurial aspirations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.