In the contemporary financial ecosystem, obtaining a loan is no longer a simple transaction between a local banker and a lifelong customer. It has evolved into a sophisticated process influenced by global economic shifts, algorithmic credit scoring, and a diverse array of lending instruments. Whether you are looking to consolidate high-interest debt, fund a major life milestone, or inject capital into a burgeoning business, understanding the mechanics of borrowing is essential. Securing a loan is a significant financial commitment that requires meticulous preparation, a clear understanding of the marketplace, and a strategic approach to repayment. This guide serves as a comprehensive roadmap for navigating the complexities of the lending world, ensuring you obtain the best possible terms while safeguarding your long-term financial health.

Understanding the Prerequisites: Preparing Your Financial Profile

Before submitting a single application, a borrower must view their financial health through the lens of a lender. Lenders are essentially risk managers; their primary goal is to determine the probability of a borrower defaulting on their obligations. To secure a loan with favorable interest rates, you must present a profile that minimizes this perceived risk.

The Role of Credit Scores and Credit History

The cornerstone of any loan application is your credit score. In the United States, the FICO score is the standard, ranging from 300 to 850. This numerical representation of your creditworthiness is derived from several factors: payment history, amounts owed, length of credit history, new credit inquiries, and the mix of credit types.

A score above 740 is generally considered excellent and will unlock the most competitive interest rates. If your score is lower, it is often prudent to delay your application by six months to a year to focus on credit repair. This involves paying down existing revolving balances to lower your credit utilization ratio and ensuring every payment is made on time. Even a small bump in your score can save you thousands of dollars in interest over the life of a loan.

Debt-to-Income Ratio (DTI) and Financial Stability

While the credit score tells a lender how you have handled debt in the past, the Debt-to-Income (DTI) ratio tells them if you can afford new debt in the present. DTI is calculated by dividing your total monthly debt payments by your gross monthly income.

Most lenders prefer a DTI ratio of 36% or lower, though some personal loan providers and mortgage programs may allow for higher ratios depending on other compensating factors. To optimize this ratio, consider paying off small balance loans or increasing your verifiable income. Stability also plays a role; lenders typically look for at least two years of steady employment in the same field or a consistent history of self-employment income verified through tax returns.

Documentation: Gathering the Necessary Proof of Income

Modern lending requires an audit trail. To streamline the application process, you should preemptively gather a comprehensive “loan file.” For traditional employees, this includes the last two years of W-2 forms and at least 30 days of pay stubs. For entrepreneurs or freelance professionals, the requirements are more stringent, often necessitating two years of full federal tax returns (including Schedules C or K-1) and several months of business bank statements. Providing clear, organized documentation not only speeds up the approval process but also builds trust with the underwriter reviewing your file.

Evaluating Your Options: Types of Loans and Their Purposes

Not all loans are created equal. The “best” loan is the one that aligns most closely with your specific financial objective and offers the lowest total cost of capital. Selecting the wrong instrument can result in unnecessary fees or interest charges that hinder your financial progress.

Personal Loans: Versatility and Interest Rates

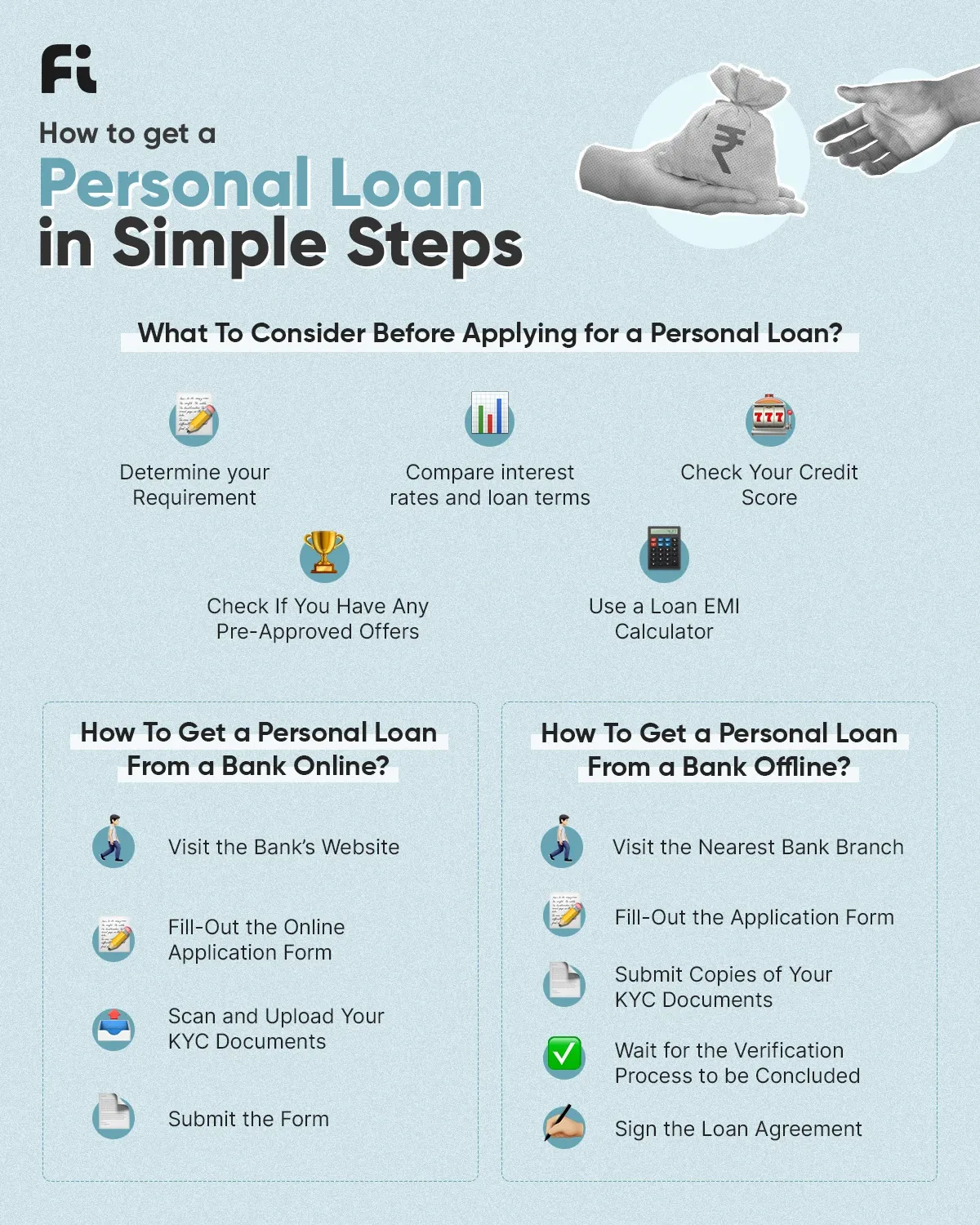

Personal loans are typically unsecured, meaning they do not require collateral like a house or a car. They are popular for debt consolidation, home improvements, or emergency expenses. Because they are unsecured, the interest rates are generally higher than those of a mortgage or auto loan but significantly lower than the average credit card.

The fixed-rate nature of most personal loans provides predictability—you know exactly what your monthly payment will be and when the debt will be fully retired. However, it is vital to watch for “origination fees,” which are one-time charges deducted from the loan proceeds, effectively increasing the Annual Percentage Rate (APR).

Secured vs. Unsecured Loans

The distinction between secured and unsecured lending is fundamental to managing financial risk. A secured loan is backed by an asset. For example, a Home Equity Line of Credit (HELOC) uses your home as collateral. Because the lender can seize the asset in the event of default, these loans offer much lower interest rates.

The risk, however, falls squarely on the borrower. If you cannot make payments on an unsecured personal loan, your credit score will suffer, and you may face legal action; if you cannot make payments on a secured loan, you could lose your home or vehicle. Understanding this balance of risk is crucial when deciding how to fund a large purchase.

Specialized Lending: Mortgages, Auto Loans, and Business Financing

When borrowing for a specific purpose, specialized loans are almost always superior to general-purpose ones. Mortgages, for instance, are structured over 15 to 30 years and offer tax advantages in many jurisdictions. Auto loans are tailored to the depreciation schedule of a vehicle.

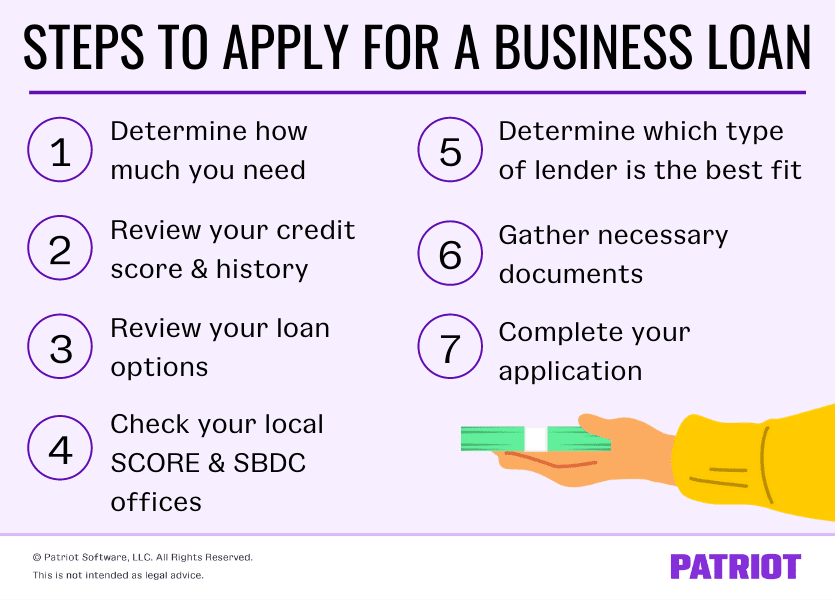

For entrepreneurs, business loans (such as SBA loans in the U.S.) offer terms that account for the unique cash flow cycles of a company. These specialized products often come with “covenants” or specific rules on how the money must be used, but in exchange, they offer terms that a general personal loan simply cannot match.

The Application Process: From Research to Approval

Once you have prepared your finances and selected the right type of loan, the execution phase begins. The goal here is to shop for the best rate without damaging your credit score through excessive inquiries.

Comparing Lenders: Banks, Credit Unions, and Online Platforms

The lending market is divided into three main sectors. Traditional banks offer stability and the potential for relationship-based discounts if you already have accounts there. Credit unions, being member-owned, often provide the most competitive rates and a more personalized underwriting process.

Online FinTech lenders have revolutionized the industry by offering rapid approval times and highly accessible digital interfaces. While online lenders are convenient, always verify their legitimacy through the Better Business Bureau or financial regulatory bodies to ensure you are not dealing with predatory “payday” lenders who charge triple-digit interest rates.

The Pre-Approval Phase and Its Benefits

Many modern lenders offer a “pre-qualification” or “pre-approval” process that uses a “soft” credit pull. Unlike a “hard” pull, a soft inquiry does not impact your credit score. This allows you to see the potential interest rates and loan amounts you qualify for across multiple lenders.

Comparison shopping is the single most effective way to lower your borrowing costs. A difference of even 1% in the interest rate on a five-year loan can result in hundreds or thousands of dollars in savings. Collect at least three different offers before committing to a final application.

Finalizing the Application and Understanding the Terms

After selecting a lender, you will move to the formal application. This is where the lender performs a hard credit pull and conducts a deep dive into your documentation. During this phase, it is critical to read the “Truth in Lending” disclosure.

Pay close attention to the APR, which includes both the interest rate and any fees, providing a true picture of the loan’s cost. Check for “prepayment penalties”—clauses that charge you a fee for paying the loan off early. In the modern market, you should generally avoid any loan that penalizes you for being financially responsible and settling your debt ahead of schedule.

Strategic Financial Management: Managing Your Loan Post-Disbursement

Securing the loan is only the beginning. True financial success lies in how you manage the debt once the funds are in your account. A loan should be viewed as a tool to leverage your current position into a better one, not as a permanent extension of your income.

Creating a Repayment Plan to Avoid Pitfalls

As soon as the loan is disbursed, automate your payments. Late fees are expensive, but the damage to your credit score from a single 30-day delinquency can take years to recover.

If the purpose of the loan was debt consolidation, it is imperative to address the habits that led to the original debt. Many borrowers consolidate their credit cards into a personal loan only to run up the balances on the cards again, resulting in a doubled debt burden. Effective loan management requires a strict budget that accounts for the new monthly obligation without relying on further borrowing.

Refinancing and Early Repayment Strategies

Financial markets are dynamic. If interest rates drop significantly or if your credit score improves substantially after a year of timely payments, consider refinancing. Refinancing involves taking out a new loan at a lower interest rate to pay off the old one, thereby reducing your monthly payment or shortening the loan term.

Furthermore, even small additional payments toward the principal can drastically reduce the total interest paid over time. Because of how amortization works, extra payments made early in the life of the loan have the greatest impact on reducing the total cost of borrowing.

Protecting Your Credit for Future Borrowing

A loan is an opportunity to build a robust credit history. By managing a loan successfully, you demonstrate to the financial world that you are a reliable steward of capital. This increases your “borrowing power” for future needs, such as buying a home or expanding a business.

Monitor your credit report regularly during the repayment period to ensure the lender is reporting your on-time payments correctly. Protecting your credit health is an ongoing process that ensures that the next time you need to get a loan, the doors of the financial world will be wide open, offering you the most favorable terms possible.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.