In the landscape of personal finance, mastery over small calculations can lead to significant long-term wealth. While “percent off” signs are ubiquitous in retail environments, truly understanding how to find out the percent off—and more importantly, how that percentage impacts your overall financial health—is a cornerstone of savvy consumerism. Navigating discounts is not merely about snagging a bargain; it is about protecting your purchasing power and ensuring that your budget remains intact in the face of aggressive marketing.

This guide will break down the essential mathematics of discounts, the psychological traps of promotional pricing, and how to integrate these savings into a broader wealth-building strategy.

1. The Fundamentals of Discount Mathematics

To manage money effectively, one must be able to perform quick mental calculations. Understanding how to find out a percentage off allows you to make real-time decisions without always relying on a smartphone calculator.

The Mental Math Shortcut: The 10% Method

The easiest way to calculate any discount is to start with 10%. To find 10% of any number, simply move the decimal point one place to the left. For example, 10% of $85.00 is $8.50. Once you have this baseline, you can calculate almost any other percentage:

- For 20% off: Double the 10% figure ($8.50 × 2 = $17.00).

- For 5% off: Halve the 10% figure ($8.50 ÷ 2 = $4.25).

- For 15% off: Add the 10% and 5% figures together ($8.50 + $4.25 = $12.75).

Calculating the Final Price Directly

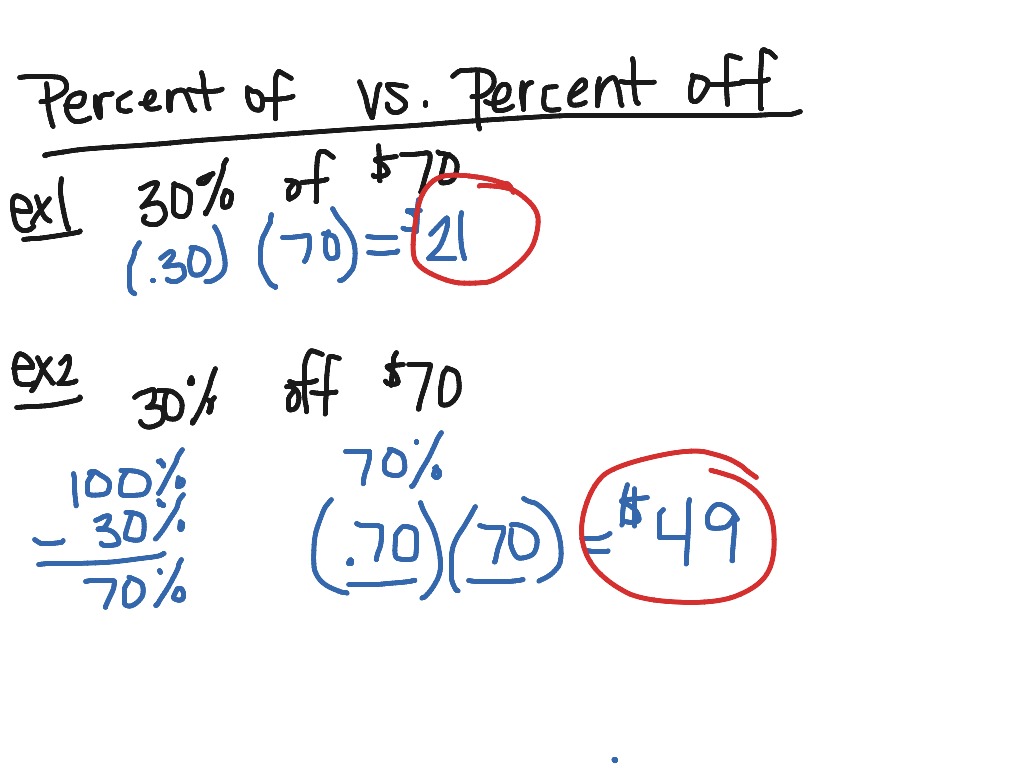

When you are focused on your cash outflow, it is often more efficient to calculate the “percentage paid” rather than the “percentage off.” If an item is 30% off, you are paying 70% of the original price.

- Formula: Original Price × (1 – Discount Rate) = Final Price.

- Example: For a $120 jacket at 30% off, calculate $120 × 0.70 = $84.00. This method streamlines your budgeting process by giving you the final impact on your bank account immediately.

Working Backward: Finding the Original Value

In financial auditing or personal expense tracking, you may need to find the original price of an item based on the discounted price you paid. This is crucial for insurance valuations or understanding the true “MSRP” (Manufacturer’s Suggested Retail Price) of your assets.

- Formula: Sale Price / (1 – Discount Rate) = Original Price.

- Example: If you paid $60 for a pair of shoes that were 40% off, you calculate $60 / 0.60 = $100.00. This reveals that you saved $40, which can then be recorded in your savings ledger.

2. Understanding Different Types of Percent Off Offers

Not all “percent off” advertisements are created equal. In the world of business finance and retail marketing, terminology can often obscure the actual value being offered to the consumer.

Stackable Discounts and Sequential Math

A common pitfall in consumer finance is “stacking” discounts incorrectly. If a store offers 20% off and you have an additional 10% coupon, the total discount is rarely 30%. Most retailers apply discounts sequentially.

- Calculation: On a $100 item, the 20% discount brings it to $80. The additional 10% is then taken off the $80, resulting in an $8 discount ($80 – $8 = $72).

- The Reality: Your total savings is actually 28%, not 30%. Understanding this nuance prevents “budget creep” where you overspend based on an inflated expectation of savings.

BOGO vs. Straight Percentage Off

“Buy One, Get One 50% Off” (BOGO 50) is a frequent marketing tactic that sounds more lucrative than it often is. Mathematically, BOGO 50 is equivalent to a 25% discount on the total transaction, provided both items are of equal value. If the items are of different values, the discount is always applied to the cheaper item, further reducing your effective “percent off.” From a personal finance perspective, a straight 30% off one item is often superior to a BOGO 50 offer because it requires less capital outlay to achieve the savings.

Conditional and Threshold Discounts

Many high-end brands use threshold discounts, such as “$50 off every $200 spent.” To find out the percent off here, you must divide the savings by the total spent. If you spend exactly $200, you are getting 25% off. However, if your total is $350, you still only get $50 off, which drops your effective discount to roughly 14%. Knowing these numbers allows you to decide if adding an extra item to reach a threshold is a sound financial move or a marketing trap.

3. The Role of Discounts in a Personal Finance Framework

Finding out the percent off is a tactical skill, but applying that skill to your financial strategy is a master-level move. In personal finance, the goal isn’t just to spend less, but to optimize where every dollar goes.

Avoiding the “Sale Trap”

One of the most important lessons in money management is: “If you buy a $1,000 item for $700, you didn’t save $300; you spent $700.”

Finding the percent off should be a secondary step to the primary question: “Was this purchase already planned in my budget?”

Financial planners often recommend the 24-hour rule: if you see a significant percent off, wait 24 hours. If the need for the item survives the cooling-off period, then the discount is a legitimate win for your net worth.

Reinvesting Your Savings

The true power of finding out the percent off lies in what you do with the money you didn’t spend. If you save $50 on a grocery bill through strategic discounting, that $50 should not simply vanish into your checking account to be spent elsewhere.

- The Micro-Investing Strategy: Move the calculated savings immediately into a High-Yield Savings Account (HYSA) or a brokerage account.

- The Compounding Effect: Saving $50 a month through disciplined discount-seeking and investing it at a 7% annual return results in over $26,000 after 20 years. This transforms a simple retail discount into a retirement asset.

Seasonal Sales and Sinking Funds

For large purchases—like appliances, electronics, or furniture—finding the best percent off requires timing. By tracking historical discount cycles (e.g., Black Friday, End-of-Season, or Labor Day sales), you can create “Sinking Funds.” Instead of buying on credit when an item is at full price, you save monthly and execute the purchase when the “percent off” is at its historical peak. This avoids interest payments, effectively doubling your savings.

4. Advanced Tools for Price Monitoring and Comparison

In the modern digital economy, finding out the percent off involves more than just looking at a price tag. It requires verifying that the “original price” hasn’t been artificially inflated to make a discount look more attractive.

Unit Price vs. Percent Off

When shopping for consumables, the “percent off” can be misleading if the packaging size has changed (a phenomenon known as “shrinkflation”). To protect your finances, always calculate the unit price (price per ounce, gram, or sheet). A 20% off coupon on a smaller box may actually be more expensive per unit than a full-price larger container. Financial literacy means looking past the “percent off” sticker to the raw value underneath.

Historical Price Tracking

Many retailers use “dynamic pricing” algorithms. To truly find out the percent off, you need to see the price history. Tools that track price fluctuations on major e-commerce platforms can show you if a “30% off” deal is actually the standard price the item sells for 90% of the year. In personal finance, “percent off” is only a reality if the baseline price is honest.

The Opportunity Cost of the Hunt

Finally, a professional approach to money management requires valuing your time. If you spend three hours searching for a 5% discount on a $20 item, you are “earning” $1.00 an hour. This is a poor return on investment. Focus your energy on finding significant “percent off” opportunities on high-ticket items or recurring expenses (like insurance premiums or utility bills), where the mathematical impact on your net worth is most substantial.

Conclusion

Learning how to find out the percent off is the first step toward becoming a more conscious and effective manager of your personal capital. By mastering the mental math, understanding the mechanics of retail promotions, and—most importantly—repurposing those savings into an investment strategy, you turn a simple shopping habit into a powerful financial tool. Remember: the goal of calculating a discount is not just to spend less today, but to have more for tomorrow. In the mathematics of money, every percentage point you save and invest is a building block for your future financial independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.