Navigating the landscape of personal finance requires a mix of strategic planning and tactical knowledge. One of the most basic, yet essential, pieces of information any bank account holder needs is their account number. Whether you are setting up a direct deposit for a new job, authorizing an automated bill payment, or initiating an international wire transfer, your Chase Bank account number is the unique identifier that ensures your capital moves safely to its intended destination.

While modern banking has become increasingly streamlined, finding these specific digits can sometimes feel like a hurdle, especially with the enhanced security protocols designed to keep your financial data private. In this comprehensive guide, we will explore the various methods to locate your Chase account number, the financial significance of this identifier, and the security measures you must employ to protect your assets.

Navigating Digital Banking: Finding Your Account Number via Chase Mobile and Online Portals

In the current era of fintech, the majority of banking interactions occur through digital interfaces. Chase has invested heavily in its digital infrastructure, providing users with robust tools to manage their wealth from their smartphones or computers. Understanding how to navigate these platforms is the most efficient way to access your account details.

Using the Chase Mobile® App for Quick Access

The Chase Mobile® app is perhaps the most convenient tool for modern consumers. To find your account number here, start by logging into the app using your biometric data or passcode. Once you are on the main dashboard, tap on the specific account (e.g., Total Checking or Savings) for which you need the number.

Initially, you will only see the last four digits of your account number for security reasons. To view the full sequence, look for the “Account details” link or a small arrow near the top of the screen. Tapping “Show details” will reveal the full account number and the routing number. This digital accessibility allows you to manage your financial logistics on the go without needing physical documentation.

Accessing Details Through Chase Online℠ Banking

For those who prefer a desktop experience for more complex financial tasks, Chase Online℠ Banking offers a comprehensive overview. After logging into the Chase website, your accounts will be listed on the home screen. Click on the account name to open the activity page.

Under the account title, you will find a link labeled “See full account number.” Upon clicking this, a secure pop-up or dropdown will display the full string of digits. This interface is particularly useful when you are simultaneously managing spreadsheets or accounting software, as it allows for easy copy-pasting into secure financial management tools.

Security Protocols for Digital Financial Information

It is important to note that Chase employs “masked” numbers as a default setting. This is a deliberate financial security feature. By hiding the full account number behind a layer of authentication, the bank minimizes the risk of “shoulder surfing”—where unauthorized individuals glimpse sensitive data in public spaces. Always ensure you are on a private, secure Wi-Fi connection when accessing these details, as public networks are often vulnerable to data interception.

Traditional Methods: Utilizing Statements and Physical Documents

Despite the shift toward paperless banking, physical documents remain a reliable “source of truth” in the financial world. There are several instances where a digital screen might not be sufficient—such as when a title company requires a physical voided check or a formal bank statement for a mortgage application.

Decoding Your Monthly Paper or Electronic Statements

Your monthly statement is a legal record of your financial standing. Whether you receive a paper copy in the mail or download a PDF version via the “Statements & Documents” tab on the Chase website, your account number is always prominently displayed.

Typically, you can find the account number in the top right or left corner of the first page, often labeled clearly as “Account Number.” For those focused on long-term financial organization, keeping a digital archive of these statements is a best practice. It not only provides a quick reference for your account number but also serves as an audit trail for your spending and saving habits.

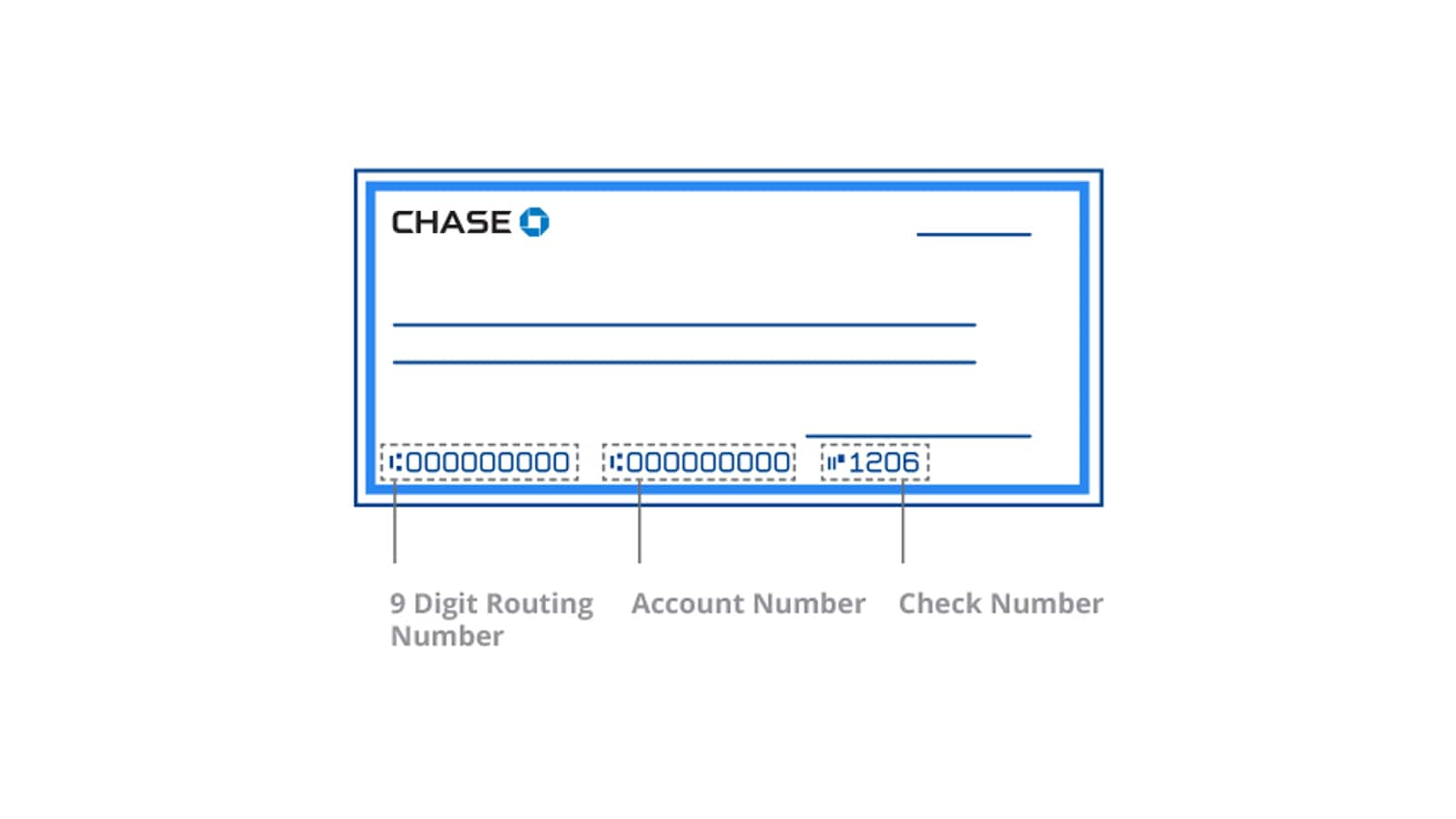

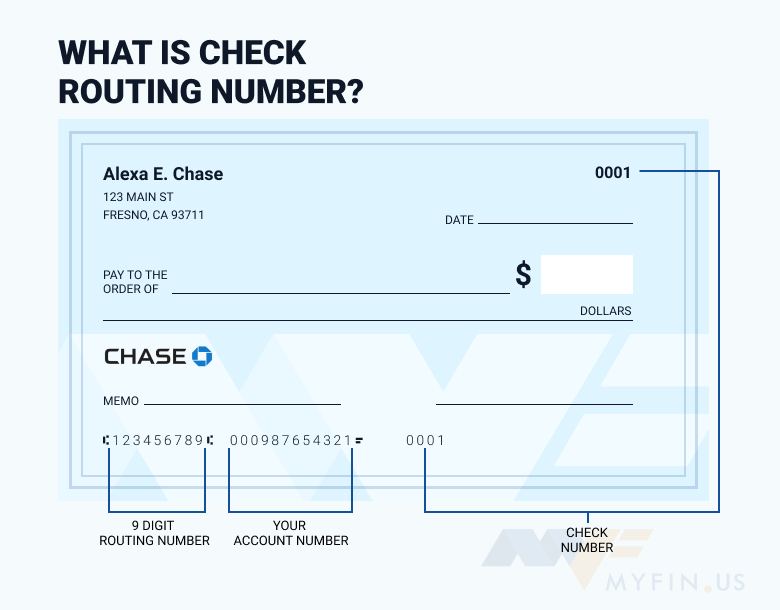

Reading a Personal Check: Account vs. Routing Numbers

For users who still utilize a physical checkbook, your account number is literally at your fingertips. At the bottom of every Chase check, there is a string of numbers printed in a specialized font known as MICR (Magnetic Ink Character Recognition).

There are three distinct sets of numbers:

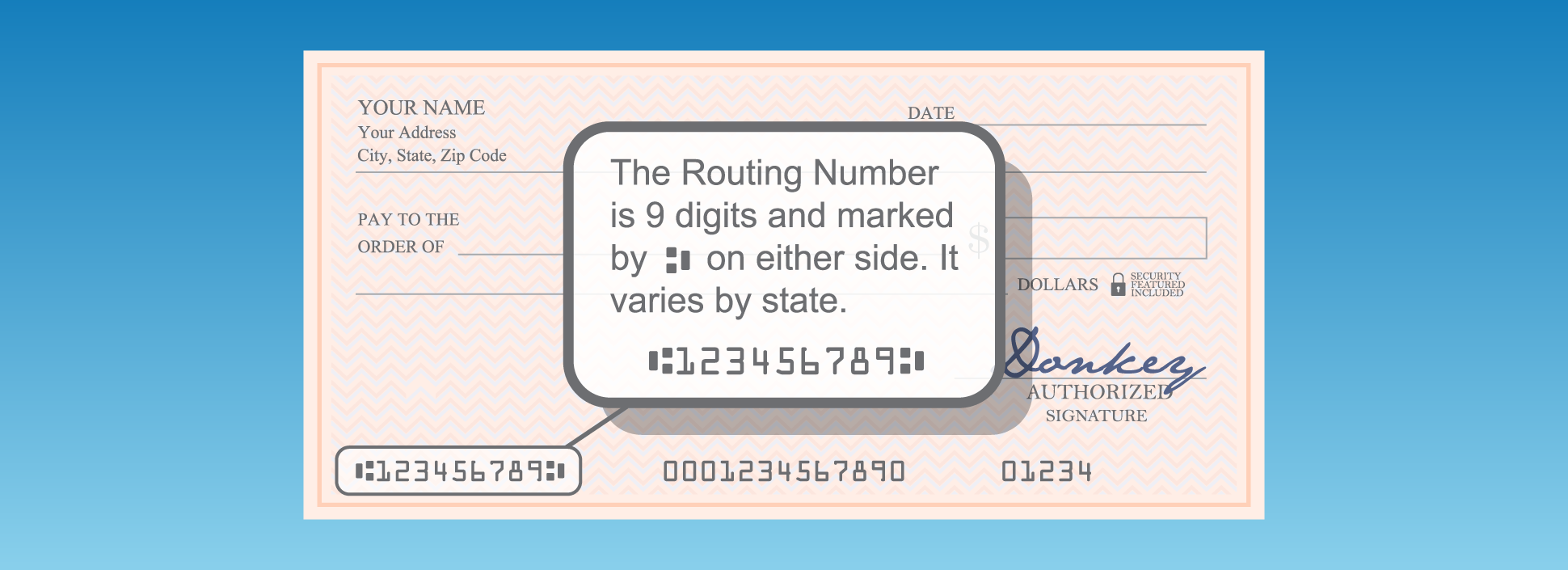

- The Routing Number: A nine-digit code that identifies the financial institution (Chase).

- The Account Number: Usually the middle set of numbers, identifying your specific account.

- The Check Number: The final set of numbers, which matches the number in the top right corner of the check.

Understanding this layout is crucial for manual financial entries, ensuring you don’t accidentally provide your routing number in place of your account number.

The Role of Direct Deposit Forms

If you are looking for your account number specifically to set up a paycheck deposit, Chase provides a pre-filled “Direct Deposit Form” within their online portal. By navigating to “Account services” and selecting “Create a direct deposit form,” the system generates a document that already includes your full account and routing numbers. This eliminates the risk of transcription errors, which can lead to delayed payments and cash flow disruptions.

The Financial Significance of Your Account Number in Modern Banking

Your account number is more than just a random sequence of digits; it is the cornerstone of your financial identity within the banking system. Understanding how this number interacts with the broader economy is vital for sophisticated financial management.

Facilitating Seamless ACH and Wire Transfers

In the world of personal finance, moving money efficiently is key. The Automated Clearing House (ACH) network relies on your account number to route “push” and “pull” transactions. This includes everything from paying your credit card bill to receiving a tax refund from the IRS.

Wire transfers, while different from ACH in terms of speed and cost, also require the account number to ensure the funds reach the specific individual. When dealing with high-value transactions, such as a down payment on a home, double-verifying your account number is the single most important step in preventing catastrophic financial loss.

Setting Up Automated Bill Pay and Direct Deposits

Automation is a primary pillar of wealth building. By using your account number to set up automated transfers to investment accounts or high-yield savings accounts, you remove the “decision fatigue” associated with saving. Your account number acts as the bridge between your income (employer) and your financial goals (investments). Ensuring this bridge is correctly identified prevents “returned items” or late fees that can negatively impact your credit score.

Account Numbers vs. Routing Numbers: Knowing the Difference

A common point of confusion in personal finance is the distinction between routing and account numbers. Think of the routing number as the “address” of the bank building, and the account number as your specific “apartment number” within that building. You need both for the “mail” (your money) to arrive correctly. In the Money niche, precision is paramount; confusing these two can lead to failed transactions and administrative headaches with your financial service providers.

Security Best Practices: Protecting Your Chase Account Credentials

In an age where identity theft and financial fraud are on the rise, your account number must be treated as highly sensitive information. It is the “key” to your vault, and protecting it is a core component of financial literacy.

Recognizing Phishing Scams and Social Engineering

Fraudsters often use sophisticated “phishing” emails or “vishing” (voice phishing) calls, pretending to be Chase representatives. They may claim there is an “issue with your account” and ask you to verify your full account number. Chase will never ask for your full account number or password via an unsolicited phone call or email. If you receive such a request, hang up and call the number on the back of your official debit card. Protecting your account number from these social engineering tactics is your first line of defense in preserving your capital.

The Importance of Secure Document Disposal

Because your account number appears on checks and statements, physical security is just as important as digital security. Financial advisors recommend shredding any documents that contain your full account number before disposing of them. Dumpster diving remains a common tactic for identity thieves looking to gain access to bank accounts. A cross-cut shredder is a small investment that provides significant protection for your financial legacy.

How Chase Protects Your Sensitive Data

Chase employs several institutional-grade security measures to keep your account number safe. This includes 128-bit encryption for all digital transmissions and multi-factor authentication (MFA). By enabling MFA, even if a bad actor obtains your account number, they cannot gain access to your online portal without a secondary code sent to your trusted device. Utilizing these tools is a hallmark of a proactive and responsible approach to personal finance.

By mastering the various ways to find and protect your Chase Bank account number, you gain better control over your financial life. Whether you are using the app for a quick transfer or reviewing a paper statement for an audit, this knowledge ensures that your money remains exactly where it belongs: under your management and working toward your future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.