Filing tax returns is an annual ritual for individuals and businesses alike, a fundamental aspect of civic responsibility and a critical component of sound financial management. Far from being a mere bureaucratic chore, understanding and accurately fulfilling your tax obligations is paramount to your financial health, ensuring compliance, preventing penalties, and potentially uncovering opportunities for savings. For many, the process can seem daunting, a labyrinth of forms, regulations, and deadlines. However, with a structured approach and a clear understanding of the fundamentals, navigating the tax landscape can become a manageable and even empowering aspect of your personal and business finance strategy.

This comprehensive guide is designed to demystify the tax filing process, providing you with the knowledge and tools necessary to approach tax season with confidence. We’ll delve into the essentials, from understanding your obligations and gathering the right documents to choosing the most suitable filing method and leveraging tax-smart strategies for your financial future. Embracing your tax responsibilities isn’t just about avoiding trouble; it’s about optimizing your financial position and contributing to a well-functioning economy.

Understanding Your Tax Obligations and Preparations

Before you can even begin filling out forms, a foundational understanding of who needs to file, what information is required, and the core concepts that govern taxation is essential. This preparatory phase is crucial for ensuring accuracy and efficiency throughout the entire process.

Who Needs to File and Why It Matters

Not everyone is required to file a tax return every year. Your filing requirement typically depends on your gross income, filing status (single, married filing jointly, head of household, etc.), age, and whether you are claimed as a dependent. For instance, if your income falls below a certain threshold, you might not be legally obligated to file. However, even if you’re not required, filing can still be beneficial, particularly if you had federal income tax withheld from your paychecks or if you qualify for refundable tax credits, such as the Earned Income Tax Credit (EITC) or the Child Tax Credit (CTC), which could result in a refund.

For the self-employed, gig economy workers, and small business owners, the rules are often different. If you had net earnings from self-employment of $400 or more, you generally must file a tax return and pay self-employment tax, which covers Social Security and Medicare taxes. Understanding these thresholds and requirements is the first step toward compliance and avoiding potential penalties for non-filing. Ignoring your tax obligations can lead to significant financial repercussions, including late filing penalties, interest charges, and even legal action from tax authorities.

Gathering Essential Documents and Information

The cornerstone of accurate tax filing is meticulous record-keeping. Tax season isn’t the time to scramble for documents; ideally, you should maintain an organized system throughout the year. As the filing deadline approaches, you’ll need to consolidate a variety of financial records. Key documents typically include:

- Income Statements: W-2s (from employers), 1099-NEC (nonemployee compensation), 1099-MISC (miscellaneous income), 1099-INT (interest income), 1099-DIV (dividend income), 1099-B (stock sales), K-1s (from partnerships/S-corps), Social Security benefits statements, etc.

- Deduction & Credit Information: Mortgage interest statements (Form 1098), student loan interest statements (Form 1098-E), tuition statements (Form 1098-T), records of medical expenses, charitable contributions, childcare expenses, property taxes, state/local income taxes paid, retirement contributions (IRA, 401k), and receipts for business expenses if self-employed.

- Personal Information: Social Security numbers for yourself, your spouse, and all dependents.

- Prior Year’s Tax Return: Often useful for reference, especially for carrying forward losses or estimating deductions.

Having these documents readily available not only streamlines the filing process but also helps ensure you don’t miss out on any eligible deductions or credits that could reduce your tax liability or increase your refund.

Key Tax Concepts: Income, Deductions, and Credits

To effectively navigate your tax return, a basic grasp of core tax terminology is invaluable.

- Gross Income refers to all income you receive from any source, before any deductions.

- Taxable Income is the portion of your gross income that is subject to taxation after permissible deductions and exemptions.

- Deductions reduce your taxable income. They come in two main forms: the Standard Deduction (a fixed dollar amount based on your filing status) and Itemized Deductions (specific expenses like mortgage interest, state and local taxes, medical expenses, and charitable contributions). You choose whichever results in a lower taxable income.

- Tax Credits are even more powerful. Unlike deductions that reduce taxable income, credits directly reduce the amount of tax you owe, dollar for dollar. Some credits are non-refundable (they can reduce your tax liability to zero but won’t result in a refund beyond that), while others are refundable (they can result in a refund even if your tax liability is zero). Examples include the Child Tax Credit, Earned Income Tax Credit, and education credits.

Understanding how these elements interact is key to accurately calculating your tax liability and optimizing your financial outcome.

Choosing Your Filing Method: DIY vs. Professional Assistance

Once you’ve gathered your documents and familiarized yourself with basic tax concepts, the next decision is how you will actually prepare and submit your return. The choice typically boils down to two main avenues: preparing it yourself using software or engaging a qualified tax professional.

Navigating Online Tax Software (DIY Approach)

For many taxpayers, especially those with straightforward financial situations, online tax software offers a cost-effective and convenient solution. Programs like TurboTax, H&R Block, TaxAct, and FreeTaxUSA guide you step-by-step through the process, asking questions and populating forms based on your answers. Many even offer options for e-filing directly from the software.

Pros of DIY Software:

- Cost-Effective: Often significantly cheaper than professional preparation, with some free options available for basic returns or lower-income taxpayers (e.g., IRS Free File program).

- Convenience: File from anywhere with an internet connection, at your own pace.

- Guidance: The software walks you through complex sections, provides explanations, and often flags potential errors.

- Accuracy Checks: Built-in calculators and error-checking mechanisms help reduce mathematical mistakes.

Cons of DIY Software:

- Time Commitment: Requires you to dedicate time and attention to inputting data and understanding the questions.

- Complexity Challenges: While helpful, complex tax situations (e.g., multiple investments, significant self-employment income, international income, unique business structures) can still be overwhelming or prone to errors if you lack expertise.

- No Personalized Advice: Software can’t offer tailored tax planning advice for future financial decisions.

The DIY approach is excellent for individuals with W-2 income, standard deductions, and a few basic investment or interest statements. If your situation is relatively simple, online software provides a robust and accessible path to compliance.

The Benefits of Professional Tax Preparers

For those with more complex financial lives, or simply a desire for expert reassurance, hiring a professional tax preparer is often the wisest investment. This includes Certified Public Accountants (CPAs), Enrolled Agents (EAs), and tax attorneys.

Pros of Professional Assistance:

- Expertise for Complex Situations: Professionals excel at handling intricate scenarios like business taxes, real estate investments, stock options, trusts, significant capital gains/losses, or multi-state income.

- Error Reduction: Their experience minimizes the risk of errors, which can save you from audits, penalties, and missed opportunities.

- Tax Planning & Strategy: A good professional doesn’t just prepare your taxes; they offer valuable insights and strategies for future tax optimization, helping you make informed financial decisions throughout the year.

- Audit Support: Many professionals offer audit assistance or representation, providing peace of mind should the IRS come calling.

- Time Savings: Offload the burden of tax preparation, freeing up your valuable time.

Cons of Professional Assistance:

- Cost: Professional services are more expensive than software, with fees varying based on complexity and location.

- Finding the Right Fit: It’s crucial to research and choose a reputable, qualified professional who understands your specific financial needs.

Consider a professional if you own a business, have significant investments, experienced major life changes (marriage, divorce, birth of a child, home purchase), or simply feel overwhelmed by the tax code. The financial peace of mind and potential long-term savings from expert advice can often outweigh the upfront cost.

Step-by-Step Filing Process and Post-Filing Considerations

Whether you choose the DIY route or professional assistance, the core steps of completing and submitting your return remain similar. However, the process doesn’t end once you hit ‘submit’—there are important post-filing actions to take as well.

Completing Your Tax Forms Accurately

The actual process involves systematically inputting all your gathered income, deduction, and credit information into the appropriate fields on your tax forms (or into the software that generates these forms).

- Income First: Start by entering all sources of income. This typically involves matching figures from your W-2s, 1099s, and other statements to the relevant lines on Form 1040.

- Deductions and Credits: Next, carefully input your deductions and credits. If using software, it will prompt you for these; if doing it manually, you’ll need to know which schedules and forms apply (e.g., Schedule A for itemized deductions, Schedule C for self-employment income and expenses, Schedule E for rental income).

- Review and Verify: This is perhaps the most critical step. Before submitting, review your entire return meticulously. Double-check all Social Security numbers, addresses, income figures, and calculations. Many software programs include a final review section that highlights potential issues. Errors, even minor ones, can lead to processing delays or unwanted correspondence with tax authorities. Ensure your tax liability (or refund) calculation makes sense given your income and financial situation.

Submitting Your Return and Payment

Once you’re confident in the accuracy of your return, it’s time to submit it.

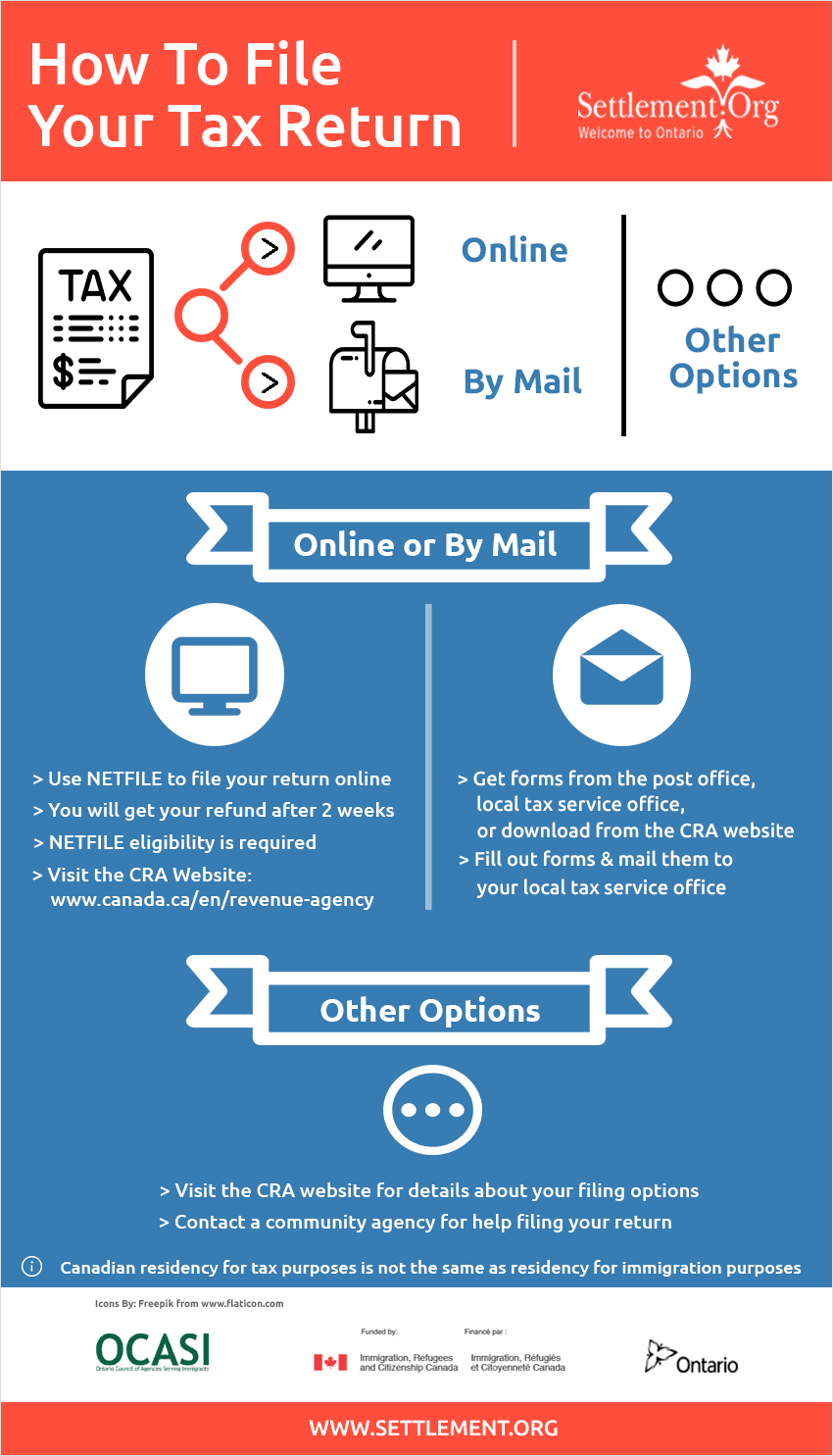

- E-filing: The vast majority of taxpayers now e-file (electronically file) their returns. It’s generally faster, more secure, and provides immediate confirmation of receipt. Refunds are typically processed much quicker via e-file and direct deposit. Most tax software allows you to e-file directly.

- Mail-in: If you prefer, you can print and mail your paper return. This method is slower and carries a higher risk of loss or delays. Always mail your return via certified mail with a return receipt requested for proof of timely submission.

- Payment: If you owe taxes, you have several options:

- Direct Debit: Many e-filing systems allow you to authorize a direct debit from your bank account.

- Credit Card: You can pay your taxes using a credit card through third-party processors, though a convenience fee usually applies.

- Check/Money Order: Mail a check or money order along with Form 1040-V (Payment Voucher) to the IRS.

- Payment Plan: If you cannot pay the full amount by the deadline, contact the IRS (or state tax authority) to inquire about installment agreements or offers in compromise to avoid additional penalties.

Regardless of your chosen method, ensure your return is submitted, and any payment is made, by the annual tax deadline (typically April 15th, unless it falls on a weekend or holiday, or is extended for specific reasons).

What to Do After Filing: Record Keeping and Future Planning

Filing your tax return is not the end of your tax responsibilities. Prudent post-filing actions are essential for long-term financial security.

- Retain Copies: Always keep copies of your filed tax return, along with all supporting documentation (W-2s, 1099s, receipts for deductions, etc.). The IRS generally has three years from the date you filed your return to audit it, so a good rule of thumb is to keep these records for at least three to seven years. For certain complex situations (e.g., unfiled returns, fraudulent returns), the statute of limitations is longer or non-existent.

- Understand Amended Returns: If you discover an error or missed information after filing, you may need to file an amended return using Form 1040-X. Be aware of the deadlines for filing amended returns (usually within three years from the date you filed the original return or two years from the date you paid the tax, whichever is later).

- Future Financial Planning: Use the insights gained from filing your current return to inform your financial decisions for the upcoming year. Did you get a large refund? You might be over-withholding from your paychecks, essentially giving the government an interest-free loan. Consider adjusting your W-4. Did you owe a lot? You might need to increase your withholdings or make estimated tax payments. Tax filing should be an annual review that feeds into your broader financial planning, identifying opportunities for savings, adjustments to investment strategies, or contributions to retirement accounts.

Common Pitfalls and How to Avoid Them

Even with careful preparation, tax filing can present challenges. Being aware of common mistakes can help you sidestep potential problems and optimize your financial outcomes.

Overlooking Deductions and Credits

One of the most frequent and costly errors taxpayers make is failing to claim all eligible deductions and credits. This often stems from a lack of knowledge about what qualifies or poor record-keeping. Many people default to the standard deduction, unaware that itemizing could save them more, especially after significant life events like buying a home, incurring substantial medical expenses, or making large charitable donations. Similarly, various tax credits for education, energy-efficient home improvements, or specific family situations are frequently missed.

To avoid this:

- Keep Detailed Records: Throughout the year, track all potential deductible expenses and credit-generating activities. Use spreadsheets, dedicated apps, or physical folders.

- Review Tax Law Changes: Tax laws can change annually. Stay informed (or consult a professional) about new deductions or credits introduced by Congress.

- Use Comprehensive Software/Professional: Tax software is designed to ask questions that uncover potential deductions. Professionals are experts in identifying all applicable tax breaks.

Mistakes Leading to Audits or Penalties

Errors on your tax return, whether accidental or intentional, can trigger audits or lead to penalties. Common red flags for the IRS include:

- Mathematical Errors: Simple addition or subtraction mistakes can be easily flagged by the IRS’s automated systems.

- Missing Information: Forgetting to include a W-2, 1099, or Social Security number.

- Underreporting Income: Failing to report all income sources, especially from the gig economy, investments, or side hustles. The IRS receives copies of 1099s and W-2s, so discrepancies are easily identified.

- Disproportionate Deductions: Claiming unusually high deductions relative to your income or profession can raise suspicion.

- Business Expenses: For self-employed individuals, improperly claiming personal expenses as business deductions is a common audit trigger.

To avoid these pitfalls:

- Double-Check Everything: Review your return multiple times, especially key figures and personal information.

- Match Third-Party Reporting: Ensure the income you report matches what the IRS receives from your employers, banks, and investment firms.

- Be Honest and Realistic: Don’t exaggerate deductions or underreport income. When in doubt, seek professional advice.

- File on Time: Late filing and late payment penalties can add up quickly. If you can’t file by the deadline, file for an extension, but remember an extension to file is not an extension to pay.

The Importance of Proactive Tax Planning

Ultimately, filing tax returns should not be a reactive annual event but an integral part of your ongoing financial strategy. Proactive tax planning involves making financial decisions throughout the year with an eye toward their tax implications.

- Year-End Tax Moves: Consider actions like contributing to retirement accounts (401k, IRA) to reduce taxable income, harvesting capital losses to offset gains, or making charitable donations before the year ends.

- Adjusting Withholdings: Periodically review your W-4 form with your employer to ensure the correct amount of tax is being withheld from your paychecks. This can help you avoid a large tax bill or a needlessly large refund.

- Consulting Financial Advisors: A financial advisor can integrate tax planning into your broader investment, retirement, and estate planning strategies, helping you minimize your lifetime tax burden and achieve your financial goals more efficiently.

By viewing tax filing as an opportunity for financial assessment and strategic planning, you transform a compliance task into a powerful tool for wealth management.

Conclusion

Filing tax returns is an unavoidable, and indeed essential, aspect of participating in the economy. While it can seem complex, approaching it with a clear understanding of your obligations, meticulous preparation, and either reliable software or professional guidance can turn it into a manageable and even beneficial process. By understanding the interplay of income, deductions, and credits, choosing the right filing method, and being diligent in your post-filing actions, you can ensure compliance, avoid penalties, and optimize your financial position.

More importantly, integrating tax considerations into your year-round financial planning empowers you to make smarter decisions, potentially reducing your tax liability and freeing up more of your hard-earned money for savings, investments, or personal enjoyment. Don’t let tax season be a source of dread; instead, embrace it as an annual opportunity to review your financial health and strategize for a more prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.