In the world of personal finance, few numbers carry as much weight as the interest rate. Whether you are eyeing a new car, managing a credit card balance, or projecting the growth of your high-yield savings account, the interest rate is the primary driver of your financial momentum. However, a common point of confusion for many consumers is the discrepancy between the Annual Percentage Rate (APR) quoted by lenders and the actual amount of interest that accrues on a monthly basis.

Understanding how to figure out your interest rate per month is more than just an academic exercise; it is a vital skill for effective budgeting and debt management. By breaking down annual figures into monthly increments, you gain a granular view of your cash flow, allowing you to make more informed decisions about borrowing and investing. This guide explores the mathematical foundations, practical applications, and digital tools necessary to master your monthly interest calculations.

The Fundamental Math Behind Monthly Interest Rates

To calculate a monthly interest rate, one must first understand the “nominal” rate versus the “periodic” rate. Most financial institutions advertise their rates in annual terms (APR) because it is the industry standard for comparison. However, interest is rarely charged or paid in a single annual lump sum. Instead, it is usually calculated over shorter periods—most commonly, every month.

Understanding Annual Percentage Rate (APR)

The Annual Percentage Rate (APR) represents the yearly cost of borrowing money, including interest and certain fees. While the APR provides a snapshot of the annual cost, it does not reflect the monthly billing cycle. To find the monthly rate, you must perform a “periodic rate” calculation. For example, if a credit card has an APR of 24%, that 24% is spread across the 12 months of the year. It is the starting point for all subsequent calculations.

The Basic Conversion Formula

The simplest way to determine your monthly interest rate is to divide the annual interest rate by the number of periods in a year. Since there are 12 months in a year, the formula is:

Monthly Interest Rate = Annual Interest Rate / 12

If you have a loan with a 6% annual interest rate, your calculation would be:

- 0.06 (6%) / 12 = 0.005

- 0.005 * 100 = 0.5% per month.

This “periodic rate” of 0.5% is what is applied to your principal balance each month. While this formula works for simple interest, it is important to remember that many financial products utilize daily compounding, which adds a layer of complexity.

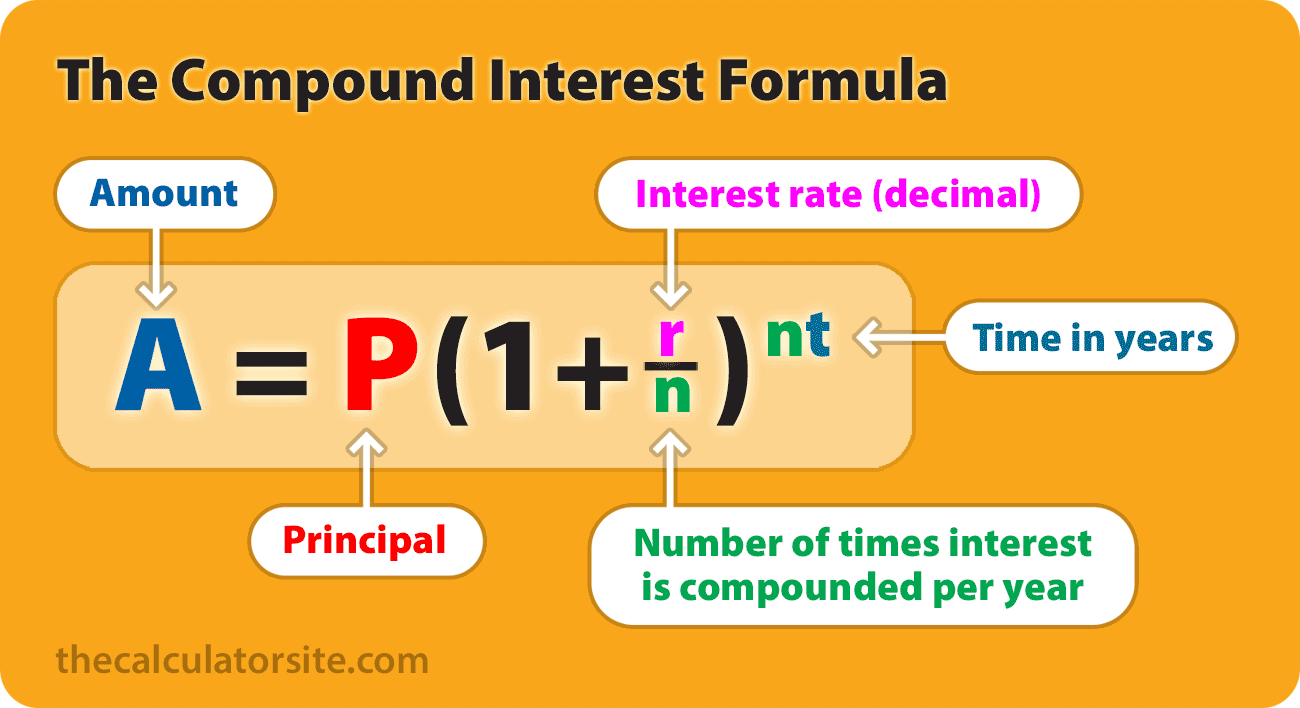

Dealing with Compounding Periods

Compounding is the process where interest is calculated on the initial principal and also on the accumulated interest of previous periods. If your interest compounds monthly, the simple division formula works well. However, if your interest compounds daily (as is common with credit cards), the lender divides the APR by 365 to find the Daily Periodic Rate (DPR). They then apply this rate to your balance every day of the billing cycle. Even though the calculation happens daily, the result is summarized on your monthly statement. Understanding this distinction is crucial for realizing why a 20% APR can feel more expensive than it looks on paper.

Practical Applications: Credit Cards and Personal Loans

Applying the monthly interest formula to real-world debt is where financial literacy turns into financial power. Most people look at their monthly statements and see a “minimum payment,” but they rarely look at the “interest charged” line item. By calculating this yourself, you can predict exactly how much of your payment is going toward the principal and how much is disappearing into the lender’s pockets.

Calculating Credit Card Interest

Credit cards are unique because they often use the “Average Daily Balance” method. To figure out your monthly interest cost here, you don’t just look at your balance on the last day of the month. You must:

- Find your Daily Periodic Rate (APR / 365).

- Add up your balance for every single day in the billing cycle.

- Divide that total by the number of days in the cycle to find the Average Daily Balance.

- Multiply the Average Daily Balance by the Daily Periodic Rate, then multiply that by the number of days in the month.

This process highlights why making a payment early in the month—even if it is weeks before the due date—can actually save you money by lowering your average daily balance.

Personal Loan Amortization

Unlike credit cards, personal loans and mortgages usually have a fixed monthly payment. However, the ratio of interest to principal changes every month. In the early stages of a loan, your monthly interest rate is applied to a large principal balance, meaning a significant portion of your payment goes toward interest. As you pay down the principal, the 1/12th of the annual rate is applied to a smaller number, causing the interest portion to shrink and the principal portion to grow. This is known as amortization. Calculating the monthly interest manually helps you see exactly when you will reach the “tipping point” where most of your money starts building equity rather than servicing debt.

How Small Rate Changes Impact Long-term Debt

When you understand the monthly rate, you begin to see the massive impact of even a 1% difference in APR. For a $30,000 car loan, a 1% decrease in the annual rate might only seem like a 0.083% difference per month. However, when applied to a large balance over 60 months, that tiny monthly fraction saves you hundreds, if not thousands, of dollars. Seeing the math at a monthly level makes the stakes of “shopping for the best rate” much more tangible.

Investment Growth: Figuring Out Monthly Returns

The math of monthly interest isn’t just for debt; it is also the engine of wealth creation. When you are the one earning interest—such as in a High-Yield Savings Account (HYSA) or a Certificate of Deposit (CD)—figuring out the monthly rate helps you track your progress toward financial goals.

Simple Interest vs. Compound Interest in Savings

Most savings accounts pay compound interest. This means that in Month 1, you earn interest on your deposit. In Month 2, you earn interest on your deposit plus the interest from Month 1. To calculate your monthly earnings, you can use the same 1/12th formula for a rough estimate, but the “Annual Percentage Yield” (APY) is a more accurate figure to look at. The APY accounts for the effect of compounding over the year, whereas the APR does not. If a bank offers a 5% APY, they are essentially saying that after 12 months of monthly compounding, your total growth will equal 5%.

The Rule of 72 and Monthly Projections

Once you have determined your monthly interest rate, you can use it to project future wealth. While the “Rule of 72” is typically used with annual rates (divide 72 by the annual rate to see how many years it takes to double your money), you can adapt this mindset for monthly goals. If you know your monthly investment return is approximately 0.8% (common in some index fund averages), you can better estimate how much you need to contribute each month to reach a specific milestone, like a down payment on a home or a retirement target.

Digital Tools and Financial Literacy

While manual calculations are essential for understanding the “why” behind the numbers, digital tools are the most efficient way to handle the “how.” In a professional financial context, spreadsheets and specialized apps are the gold standard for accuracy.

Using Spreadsheet Formulas

Excel and Google Sheets are powerhouse tools for anyone serious about their finances. You don’t need to be a math genius to use them; you just need to know the right functions.

- The

=RATEFunction: This helps you find the interest rate per period if you know the loan amount, the payment, and the duration. - Simple Division: You can create a tracking sheet where one column is your “Annual Rate” and the next is

=A1/12. - Amortization Tables: Most spreadsheet software offers templates that automatically break down your monthly interest versus principal for the life of a loan.

Financial Calculators and Apps

Beyond spreadsheets, there are countless financial calculators available online that can handle specific scenarios, such as “Credit Card Payoff Calculators” or “Mortgage Monthly Breakdowns.” These tools often allow you to input “extra payments,” showing you how a small increase in your monthly outflow can drastically reduce the total interest paid over the life of the loan.

Conclusion: Empowerment Through Financial Knowledge

Figuring out your interest rate per month is a fundamental pillar of financial literacy. It bridges the gap between the abstract percentages advertised by banks and the concrete reality of your monthly bank statement. By mastering the simple division of the APR and understanding the nuances of compounding and average daily balances, you move from a passive consumer to an active manager of your wealth.

Whether you are trying to escape the cycle of high-interest debt or looking to maximize the growth of your investments, the ability to calculate interest at the monthly level provides clarity. It allows you to see exactly where your money is going, how much it is costing you to wait, and how much you stand to gain by acting now. In the end, the math is simple, but the impact of that knowledge on your financial future is profound.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.