Understanding the Consumer Price Index (CPI) is often viewed as the domain of academic economists and central bankers. However, for anyone serious about personal finance, wealth preservation, and long-term investing, mastering the mechanics of the CPI is essential. At its core, the CPI is the most widely used measure of inflation, serving as a pulse check on the purchasing power of your money. When you hear that the cost of living has risen or that the dollar doesn’t go as far as it used to, you are hearing the real-world implications of CPI fluctuations.

To figure out the Consumer Price Index is to understand the invisible force that erodes or enhances your financial security. This guide will break down the calculation methods, the components that drive the index, and how you can apply this knowledge to build a more resilient financial portfolio.

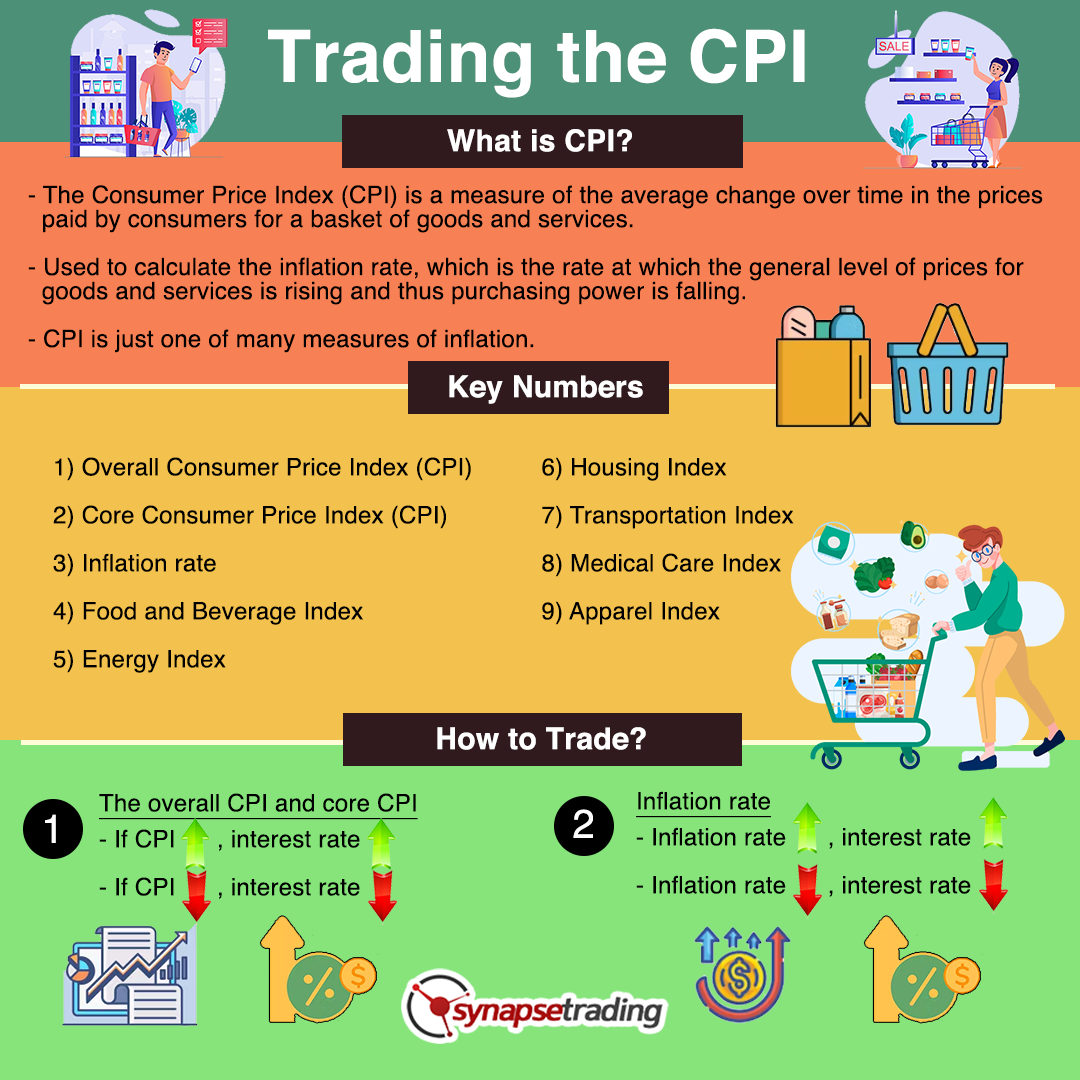

Decoding the Consumer Price Index: Definition and Core Components

Before diving into the mathematics, it is vital to understand what the CPI represents. The Consumer Price Index measures the average change over time in the prices paid by urban consumers for a representative “market basket” of consumer goods and services. In the United States, the Bureau of Labor Statistics (BLS) is responsible for tracking these prices and reporting the findings monthly.

The “Market Basket” Concept

The “market basket” is the foundation of the CPI. It isn’t a literal basket, but a curated list of over 80,000 items that the average household consumes. These items are categorized into eight major groups:

- Housing: Including rent, owners’ equivalent rent, and fuel oil.

- Food and Beverages: Grocery items, dining out, and alcoholic beverages.

- Transportation: New and used vehicles, gasoline, and public transit.

- Medical Care: Prescription drugs, hospital services, and insurance.

- Apparel: Men’s, women’s, and children’s clothing and footwear.

- Recreation: Televisions, pets, and sports equipment.

- Education and Communication: Tuition, postage, and telephone services.

- Other Goods and Services: Personal care products and tobacco.

How Data is Collected

The BLS employs data collectors who visit or call thousands of retail stores, service establishments, and rental units across the country. They track the prices of specific items month after month. To ensure accuracy, the weights of these items are adjusted based on consumer spending habits. For example, if the average household spends more on housing than on apparel, the price changes in housing will have a more significant impact on the final CPI figure.

Headline CPI vs. Core CPI

When figuring out the CPI, investors often distinguish between “Headline CPI” and “Core CPI.” Headline CPI includes all items in the basket. Core CPI, however, excludes the volatile categories of food and energy. Economists prefer Core CPI for long-term planning because food and energy prices can swing wildly due to geopolitical events or weather, which might obscure the underlying trend of inflation.

Step-by-Step Guide: How to Calculate the Consumer Price Index

While the BLS handles the massive data collection, understanding the formula allows you to grasp how inflation is quantified. The calculation is essentially a comparison of the cost of a fixed set of goods between a “base period” and the “current period.”

The Fundamental CPI Formula

The formula to calculate the CPI for a given period is:

CPI = (Cost of Market Basket in Current Year / Cost of Market Basket in Base Year) × 100

To illustrate, let’s assume the base year is 2020. If the market basket cost $5,000 in 2020 and the same basket costs $5,500 in 2024, the calculation would be:

($5,500 / $5,000) × 100 = 110.

An index of 110 means there has been a 10% increase in the price level since the base year.

Calculating the Inflation Rate

The CPI itself is an index number, but what most people care about is the “inflation rate”—the percentage change in the index over a specific timeframe (usually a year). To calculate the annual inflation rate, use the following formula:

Inflation Rate = [(CPI in Year 2 – CPI in Year 1) / CPI in Year 1] × 100

If the CPI was 240 last year and is 252 this year, the inflation rate is 5%. This 5% represents the rate at which your purchasing power is diminishing.

The Importance of the Base Year

The base year serves as the benchmark. Currently, the BLS uses a reference base of 1982–1984, setting that average to 100. This allows for a consistent long-term comparison of how prices have evolved over decades. For a personal finance enthusiast, choosing your own “base year” (such as the year you started your career) can be a powerful way to track how your personal expenses have scaled against national averages.

Why CPI Matters for Your Personal Finances

Understanding how to figure out the CPI is only the first step; the second is recognizing its profound impact on your wallet. Inflation is often called the “hidden tax” because it reduces what you can buy without changing the numbers in your bank account.

Purchasing Power and the Value of the Dollar

The most direct effect of a rising CPI is the erosion of purchasing power. If the CPI rises by 4% but your salary remains stagnant, you have effectively taken a 4% pay cut. Your ability to afford the same quality of life diminishes. Financial planning must account for this by ensuring that income growth—through raises, side hustles, or investment returns—outpaces the CPI.

Impact on Savings and Interest Rates

The CPI is a primary driver of the Federal Reserve’s monetary policy. When the CPI rises too quickly, the Fed often raises interest rates to cool the economy. For the individual, this is a double-edged sword. High inflation hurts savers if the interest rate on their savings account is lower than the inflation rate (resulting in a negative “real” return). Conversely, when the Fed raises rates in response to CPI, high-yield savings accounts and CDs become more attractive, offering a better way to hedge against rising prices.

Cost-of-Living Adjustments (COLAs)

Many financial instruments and government programs are tied directly to the CPI. Social Security benefits, for example, receive an annual Cost-of-Living Adjustment (COLA) based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Similarly, some employment contracts and rental agreements include “inflation clauses” that adjust payments based on the CPI. Knowing how to track the index ensures you are receiving the adjustments you are entitled to.

Strategic Investing in an Inflationary Environment

For investors, the CPI is a compass. It tells you whether your “nominal” returns (the percentage gain on paper) are translating into “real” returns (the gain in actual purchasing power). If your stock portfolio gains 7% in a year where the CPI rises by 8%, you have actually lost 1% of your wealth in real terms.

Treasury Inflation-Protected Securities (TIPS)

One of the most direct ways to use CPI knowledge in investing is through TIPS. These are government bonds where the principal increases with inflation and decreases with deflation, as measured by the CPI. When the bond matures, you are paid the adjusted principal or the original principal, whichever is greater. This makes TIPS an essential tool for conservative investors looking to protect their “money” from being eaten away by a rising CPI.

Real Estate and Tangible Assets

Historically, real estate has served as a strong hedge against a rising CPI. As the cost of materials and labor increases (reflected in the CPI), the value of existing structures tends to rise. Furthermore, landlords can often increase rents in line with inflation, providing a dividend-like stream of income that maintains its value. Other tangible assets, such as commodities or precious metals, often see price appreciation when the CPI signals that the currency is devaluing.

The Role of Equities

While high inflation can be challenging for some companies, many businesses have “pricing power”—the ability to pass increased costs on to consumers without losing volume. Investing in high-quality companies with strong brands and essential products can be a winning strategy. When these companies raise prices, their revenues and often their stock prices rise alongside the CPI, protecting the investor’s capital.

Limitations of CPI: Understanding What the Numbers Don’t Tell You

While the CPI is a robust tool, it is not perfect. To manage your money effectively, you must understand where the CPI might fail to reflect your personal reality.

Substitution Bias and Quality Changes

The CPI is often criticized for “substitution bias.” If the price of beef skyrockets, consumers might switch to chicken. The official CPI calculation attempts to account for this, but it may understate the “pain” felt by consumers who can no longer afford their preferred goods. Additionally, the BLS uses “hedonic adjustments” to account for quality improvements. If a new smartphone costs the same as last year’s model but has a better camera, the CPI may record this as a price decrease, even though the consumer is still out of pocket the same amount of money.

Personal Inflation vs. National Averages

Perhaps the most important takeaway for personal finance is that the national CPI is an average. Your “personal CPI” depends entirely on your spending habits. If you live in a city with soaring rents but don’t own a car, your personal inflation rate may be much higher than the national average if the national CPI is being pulled down by falling gasoline prices.

By learning how to figure out the Consumer Price Index and monitoring the specific categories that impact your budget, you can move beyond generalities. You can adjust your savings rate, pivot your investment strategy, and negotiate your salary with the confidence that comes from understanding the true value of your money. In an era of economic volatility, this technical knowledge is the ultimate financial safeguard.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.