Purchasing a car is a significant financial decision for most individuals. Beyond the excitement of choosing a make and model, understanding the nuances of car financing is paramount to ensuring you secure a deal that aligns with your financial health. One of the most critical figures you’ll encounter during this process is the Annual Percentage Rate, or APR. Far more than just an interest rate, the APR encapsulates the true cost of borrowing and can significantly impact the total amount you repay over the life of your loan. Figuring out your car loan APR, or at least how to interpret and influence it, is an essential skill for any savvy consumer. This guide will demystify APR, explore its components, and equip you with the knowledge to navigate car loan offers with confidence.

Understanding the Basics: What is APR?

Before diving into calculations, it’s crucial to grasp what APR truly represents in the context of a car loan. It’s a percentage that reflects the annual cost of borrowing money, taking into account not just the nominal interest rate but also any additional fees or charges levied by the lender.

Differentiating APR from Interest Rate

Many people mistakenly use “interest rate” and “APR” interchangeably, but there’s a vital distinction. The interest rate is simply the percentage charged by the lender for borrowing the principal amount. It’s the core cost of the loan itself. The APR, however, provides a more comprehensive picture. It’s designed to give consumers a standardized way to compare loan offers by including the interest rate plus certain other fees associated with the loan, annualized over its term. This makes APR a more accurate indicator of the total cost of borrowing than the interest rate alone.

For instance, two lenders might offer seemingly similar interest rates. However, if one lender charges significant origination fees, application fees, or other administrative costs that are rolled into the loan, its APR will be higher than a lender with the same interest rate but fewer or no additional fees. By law, lenders are required to disclose the APR, giving you a transparent figure to compare against competing offers.

Components of APR (Interest, Fees, and Charges)

The components that contribute to your car loan’s APR can vary but typically include:

- Nominal Interest Rate: This is the primary cost of borrowing the money, expressed as a percentage of the principal.

- Loan Origination Fees: Charges for processing the loan application and setting up the loan.

- Application Fees: Fees sometimes charged simply for applying, regardless of whether the loan is approved.

- Underwriting Fees: Costs associated with the lender’s assessment of your creditworthiness.

- Documentation Fees: Charges for preparing loan documents.

- Broker Fees: If you use a loan broker, their commission might be factored into the APR.

It’s important to note that not all fees are included in the APR calculation. For example, some third-party costs, like state registration fees, title fees, or certain optional add-ons (like extended warranties purchased separately), are typically not part of the APR. Always scrutinize the loan disclosure statement, specifically the Truth in Lending Act (TILA) disclosure, which legally outlines the APR and other key terms.

Why APR Matters More Than Just the Interest Rate

The significance of APR lies in its ability to reveal the true financial burden of a loan. A seemingly small difference in APR can translate into hundreds or even thousands of dollars over the lifetime of a car loan, especially considering car loans often stretch over 5 to 7 years. A lower APR means less money paid in interest and fees, resulting in lower monthly payments and a lower total cost for your vehicle. Conversely, a higher APR can significantly inflate your monthly obligation and the overall expense of owning the car, potentially straining your budget and limiting your financial flexibility. Comparing APRs across multiple lenders is therefore a non-negotiable step in smart car buying.

The Core Elements Influencing Your Car Loan APR

Your car loan APR isn’t arbitrary; it’s a carefully calculated figure based on a combination of factors that reflect your perceived risk as a borrower and the specifics of the loan itself. Understanding these influences can empower you to take steps to secure a more favorable rate.

Your Credit Score and History

This is arguably the most significant determinant of your APR. Lenders use your credit score (e.g., FICO score) and credit history to assess your likelihood of repaying the loan. A higher credit score (typically 700+) indicates a strong history of responsible borrowing and timely payments, making you a low-risk borrower. Low-risk borrowers are rewarded with lower APRs. Conversely, a lower credit score (e.g., below 600) signals higher risk, leading lenders to charge higher APRs to compensate for the increased chance of default. Before applying for a car loan, it’s wise to obtain your credit report and score to identify any errors and understand where you stand.

Loan Term Length (Short vs. Long)

The length of your loan, also known as the loan term, plays a crucial role. Shorter loan terms (e.g., 36 or 48 months) typically come with lower APRs. This is because the lender’s risk is reduced when the money is repaid faster. While shorter terms mean higher monthly payments, the total interest paid over the life of the loan is significantly less. Longer loan terms (e.g., 60, 72, or even 84 months) often have higher APRs. Lenders face more risk over an extended period, and the car’s value depreciates over time, increasing their exposure. Although longer terms offer lower monthly payments, you’ll pay substantially more in interest over the life of the loan.

Down Payment Amount

Making a substantial down payment reduces the amount of money you need to borrow, which, in turn, reduces the lender’s risk. When you have more equity in the vehicle from the start, lenders view you as a more reliable borrower. This reduced risk often translates into a lower APR. A larger down payment also means lower monthly payments and less interest accumulating over the loan term. Aiming for at least 10-20% of the car’s purchase price as a down payment is generally recommended.

Vehicle Type and Age

The car itself can influence your APR. Newer, more reliable vehicles tend to command lower APRs because they hold their value better and are less likely to incur significant mechanical issues that could impair a borrower’s ability to pay. Older, high-mileage, or less reliable vehicles are considered higher risk because their value depreciates faster, and they may require costly repairs, potentially impacting your finances. Some lenders may even be hesitant to finance very old or high-mileage cars, or they may offer only very high APRs for them.

Lender Type (Banks, Credit Unions, Dealerships)

Different types of lenders have varying risk appetites, overheads, and rate structures.

- Banks: Offer competitive rates, especially to well-qualified borrowers. They typically have stricter lending criteria.

- Credit Unions: Often known for offering some of the lowest APRs due to their non-profit status and member-focused approach. You usually need to be a member to qualify.

- Dealerships: While convenient, dealer financing (often through captive lenders like Toyota Financial Services or through third-party banks) may not always offer the best APR. They might offer promotional rates for new cars or to move inventory, but these are often limited to specific models or credit tiers. It’s common for dealerships to “mark up” interest rates offered by their lending partners to earn a commission, which means you might not get the lowest rate you qualify for.

Shopping around with multiple lenders before you visit the dealership can give you a pre-approved offer, acting as leverage when negotiating at the dealership.

Practical Steps to Calculate or Estimate Your APR

While the lender is legally obligated to provide you with the APR, understanding how to estimate or scrutinize it can be invaluable during the car-buying process.

Utilizing Online APR Calculators

The easiest and most common way to get an estimate of potential APRs and their impact on your loan is by using online calculators. Many financial websites, lender sites, and car-buying platforms offer free car loan calculators. These tools typically ask for:

- The total loan amount (car price minus down payment).

- Your estimated credit score range.

- The desired loan term (in months).

- The estimated interest rate.

While these tools usually calculate monthly payments based on an interest rate, some advanced calculators allow you to input fees to estimate the APR, or provide an estimated APR range based on your credit tier. Use these for preliminary planning, but remember they provide estimates, not guarantees.

Deciphering Loan Offers and Disclosure Statements

When a lender provides you with a loan offer, it will include a Truth in Lending Act (TILA) disclosure statement. This document is your most reliable source for the actual APR. Key sections to look for include:

- Annual Percentage Rate (APR): This will be clearly stated as a percentage.

- Finance Charge: This is the total dollar amount the loan will cost you over its entire term, assuming you make all payments on time. It includes all interest and fees that make up the APR.

- Amount Financed: The total amount of money you are borrowing.

- Total of Payments: The total amount you will have paid by the end of the loan term (Amount Financed + Finance Charge).

Carefully compare the APR and Total of Payments across different loan offers. Even small differences in APR can lead to significant differences in the total amount you pay.

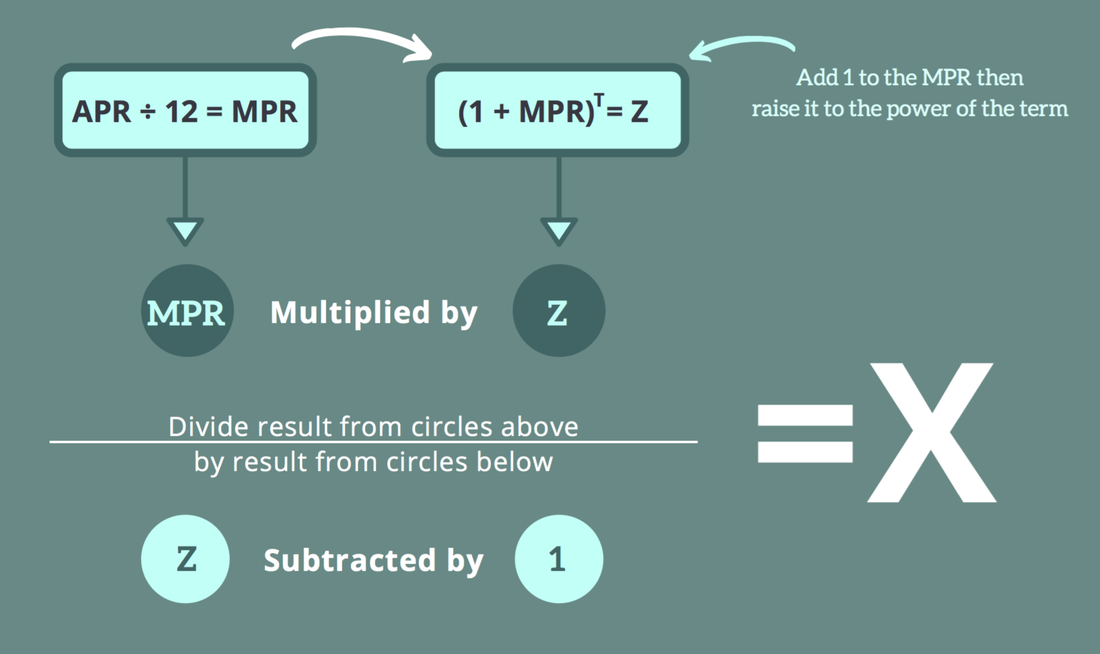

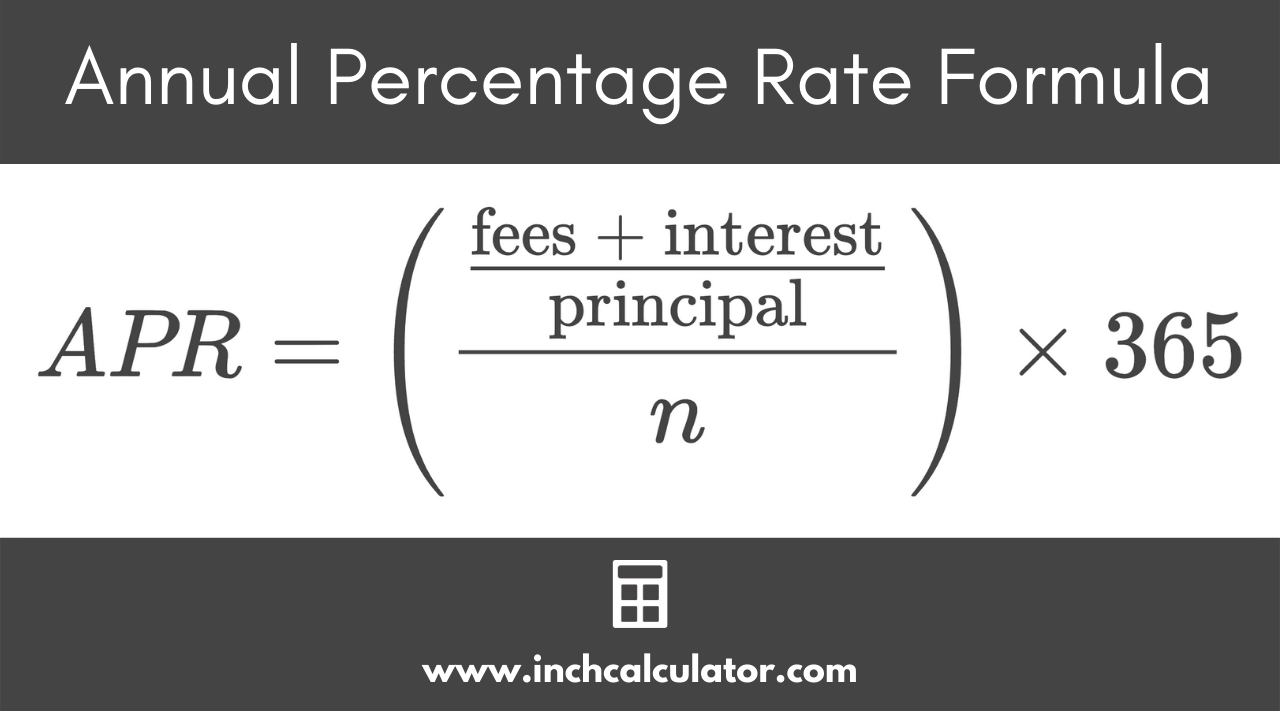

Manual Calculation (If Required) – Explaining the Limitations and Complexity

While you won’t typically need to manually calculate the precise APR yourself, understanding its components helps in identifying the costs. The actual mathematical formula for APR is complex, especially when factoring in various fees and compounding interest over different payment schedules. It typically involves iterative calculations or specialized financial functions, often represented by the RATE function in spreadsheet software.

A simplified conceptual approach:

- Identify the total cost of borrowing: Sum all interest and fees included in the APR calculation over the entire loan term.

- Divide by the loan term in years: This gives you an average annual cost.

- Divide by the principal amount borrowed: This will give you a rough percentage.

However, this simplification doesn’t account for the time value of money or compounding, which is why actual APR calculators or official disclosure statements are preferred. The key takeaway is to focus on the stated APR provided by the lender as it’s the legally mandated figure designed for comparison.

Gathering Key Information for Calculation

To effectively compare offers or use online calculators, have the following information readily available:

- Your Credit Score: An approximation is fine for estimates.

- Loan Amount Needed: Vehicle price minus your down payment.

- Loan Term Desired: How many months you want to pay back the loan.

- Any known fees: Origination fees, documentation fees, etc. (though often these are directly factored into the APR the lender provides).

Having these figures at hand allows for quick and accurate comparisons, enabling you to make an informed decision.

Strategies to Secure a Lower APR on Your Car Loan

A lower APR can save you thousands of dollars, making it crucial to employ strategies to improve your chances of securing the best possible rate.

Improving Your Creditworthiness

Since your credit score is the biggest factor, dedicating time to improve it before applying can yield significant savings.

- Pay bills on time, every time: Payment history is the most important factor in your credit score.

- Reduce outstanding debt: Especially credit card debt. A lower credit utilization ratio (amount of credit used vs. available) is favorable.

- Avoid opening new credit accounts: Multiple hard inquiries within a short period can temporarily lower your score.

- Review your credit report for errors: Dispute any inaccuracies immediately with the credit bureaus.

Shopping Around for Lenders

Never take the first loan offer you receive, especially from a dealership.

- Get pre-approved: Apply to several banks, credit unions, and online lenders before visiting the dealership. This gives you a baseline APR and strengthens your negotiating position.

- Compare offers: Focus on the APR, total finance charge, and total amount payable.

- Consider credit unions: They often offer more favorable rates than traditional banks or dealerships.

Making a Substantial Down Payment

As discussed, a larger down payment reduces the principal amount borrowed and the lender’s risk, often leading to a lower APR. It also reduces your monthly payments and the total interest you’ll pay over the loan’s life. Aim for at least 20% if possible, especially for new cars, to avoid being “upside down” (owing more than the car is worth) early in the loan term.

Negotiating Terms Beyond the Sticker Price

While you can’t negotiate the APR directly once it’s set by a lender based on your credit, you can influence the overall cost of the loan by:

- Negotiating the car’s purchase price: A lower purchase price means you borrow less, which can reduce the total interest paid even at the same APR.

- Avoiding unnecessary add-ons: Dealerships often push extended warranties, paint protection, or other accessories that inflate the loan amount and thus the total interest.

Considering Shorter Loan Terms

While it means higher monthly payments, opting for a shorter loan term (e.g., 36 or 48 months instead of 60 or 72) typically results in a lower APR and significantly less total interest paid over the life of the loan. Only choose a shorter term if the monthly payments are comfortably within your budget, ensuring you don’t overstretch your finances.

The Long-Term Impact of APR on Your Financial Health

The APR on your car loan isn’t just a number; it’s a critical component that shapes your long-term financial landscape. Understanding its far-reaching effects allows for more strategic financial planning.

Total Cost of Ownership

The APR directly influences the total cost of owning your car. A higher APR means a larger portion of your monthly payment goes towards interest, not principal. Over a 5-7 year loan term, this can add thousands to the actual purchase price of the vehicle. When comparing two cars, the one with a slightly higher sticker price but a significantly lower APR might actually be cheaper in the long run than a “bargain” car with a high APR. Always factor in the total finance charge (part of the APR disclosure) when assessing the true cost of ownership.

Monthly Payment Implications

While a low monthly payment might seem attractive, especially with longer loan terms, it often comes at the expense of a higher APR and increased total interest. Conversely, a higher monthly payment from a shorter term and lower APR means you build equity faster and pay off the debt sooner. Your APR directly determines the size of your interest payment each month, which impacts how quickly your principal balance decreases. This has a direct bearing on your monthly budget and cash flow.

Opportunity Cost of Higher Interest

Every dollar you spend on higher interest due to a elevated APR is a dollar that could have been used elsewhere. This is known as opportunity cost. That money could have been:

- Saved for a down payment on a house.

- Invested in a retirement account.

- Used to pay down other high-interest debt (like credit cards).

- Allocated to an emergency fund.

A higher APR can therefore impede your ability to achieve other financial goals, slowing your wealth accumulation and increasing your overall debt burden.

Financial Planning and Budgeting

Understanding your car loan APR is fundamental for effective financial planning and budgeting. Knowing the precise cost of your loan helps you:

- Create accurate budgets: You’ll know exactly how much of your income is committed to transportation costs.

- Assess affordability: Determine if a specific vehicle is truly within your financial means, considering all costs, not just the sticker price.

- Plan for future expenses: A lower car payment due to a good APR frees up funds for other life events or investments.

By prioritizing a low APR, you’re not just saving money on a car; you’re making a strategic decision that supports your broader financial health and future aspirations.

Conclusion

Figuring out the APR on a car loan is not just about crunching numbers; it’s about empowering yourself with knowledge to make one of the smartest financial decisions possible when purchasing a vehicle. The APR is the truest reflection of your borrowing cost, encompassing both the interest rate and various lender fees. By understanding the factors that influence your APR, actively working to improve your creditworthiness, shopping around for the best rates, and meticulously reviewing loan disclosures, you position yourself to secure a more favorable deal. A lower APR means lower overall costs, reduced monthly payments, and more financial freedom, contributing positively to your long-term financial health. Don’t let the excitement of a new car overshadow the importance of understanding its financing; a vigilant approach to your car loan APR will serve you well for years to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.