Understanding how to calculate interest on a loan is one of the most vital skills in personal and business finance. Whether you are taking out a mortgage for a new home, securing a car loan, or managing a line of credit for a small business, the interest rate is the price you pay for borrowing capital. To the untrained eye, a monthly payment might look like a single, monolithic number. However, that number is comprised of two distinct parts: the principal (the amount you borrowed) and the interest (the cost of “renting” that money).

Mastering the math behind these figures allows you to make informed decisions, compare different lending products effectively, and ultimately save thousands of dollars over the life of a loan. This guide explores the mechanics of interest calculation, from simple formulas to the complexities of amortization.

Understanding the Fundamentals of Interest Calculation

Before diving into the formulas, it is essential to understand the underlying logic of how lenders charge interest. Interest is not just a random fee; it is a calculated percentage of the outstanding principal balance. The way this percentage is applied depends on the type of loan and the compounding frequency.

Simple Interest vs. Compound Interest

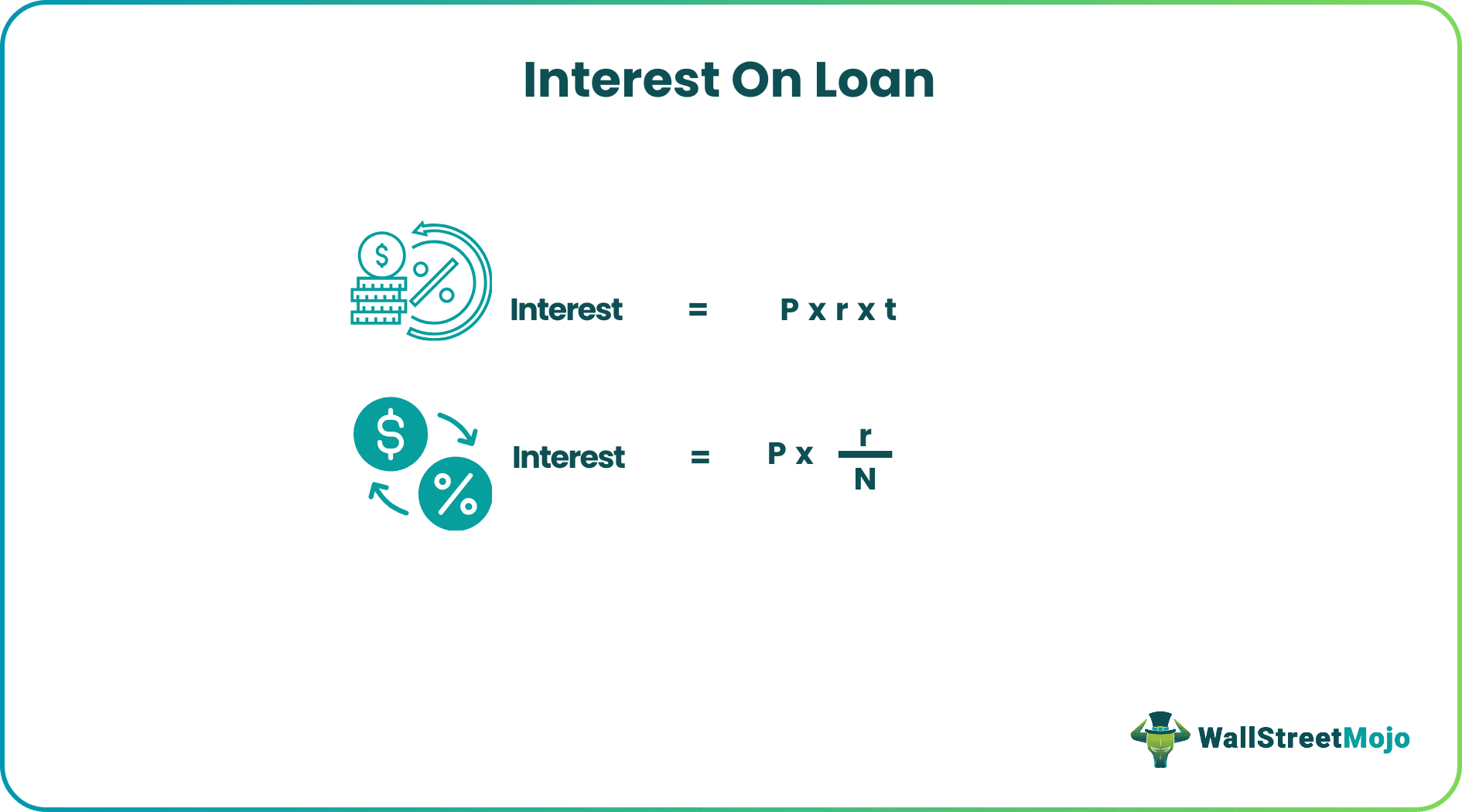

The most basic form of interest is Simple Interest. This is calculated only on the principal amount of the loan. It is most common in short-term personal loans or specific types of consumer financing. The formula is straightforward: you multiply the principal by the interest rate and the length of the loan. Because it doesn’t “snowball,” simple interest is generally the most borrower-friendly calculation.

Compound Interest, on the other hand, is the interest calculated on the initial principal and also on the accumulated interest of previous periods. While common in savings accounts and investments (where it works in your favor), it is also the standard for credit cards and some business lines of credit. If you do not pay off your balance in full, the interest itself begins to accrue interest, leading to a much higher total cost over time.

The Role of the Annual Percentage Rate (APR)

When comparing loans, you will often see two different numbers: the interest rate and the Annual Percentage Rate (APR). While the interest rate tells you the specific cost of the principal, the APR provides a more holistic view of the loan’s cost. The APR includes the interest rate plus any additional fees, such as origination fees, mortgage insurance, or closing costs.

When figuring out the “real” interest on a loan, always look at the APR. A loan with a lower interest rate but high closing fees might actually be more expensive than a loan with a slightly higher interest rate and no fees. In the world of finance, the APR is the “true” north for cost comparison.

Step-by-Step Methods for Calculating Interest

Once you understand the terminology, you can begin to run the numbers. Depending on your loan type, you will use different mathematical approaches.

The Simple Interest Formula

To calculate simple interest, use the following formula:

Interest = Principal × Rate × Time

- Principal: The total amount borrowed.

- Rate: The annual interest rate (expressed as a decimal).

- Time: The term of the loan in years.

For example, if you borrow $10,000 at a 5% interest rate for 3 years, the calculation would be:

$10,000 × 0.05 × 3 = $1,500.

Your total repayment would be $11,500. This method is the easiest to grasp but is less common for long-term debt like mortgages or student loans.

Calculating Interest for Amortized Loans

Most installment loans—like mortgages and auto loans—use amortization. This means that while your monthly payment remains the same, the ratio of interest to principal changes every month. In the beginning, the majority of your payment goes toward interest because your balance is at its highest. As you pay down the principal, the interest charge (calculated on that lower balance) decreases, allowing more of your payment to go toward the principal.

To calculate the monthly interest for an amortized loan manually:

- Divide your annual interest rate by 12 (to get the monthly rate).

- Multiply that monthly rate by your current loan balance.

If you have a $200,000 mortgage at 6% interest:

- Monthly rate: 0.06 / 12 = 0.005.

- Month 1 interest: $200,000 × 0.005 = $1,000.

If your total payment is $1,200, then $1,000 goes to the bank for interest, and only $200 goes toward your $200,000 debt.

Using Daily Balance Methods for Credit Cards

Credit cards operate differently. They typically use a Daily Periodic Rate (DPR). To find this, the lender divides your APR by 365. They then multiply this daily rate by your average daily balance and the number of days in your billing cycle.

Because credit cards compound daily or monthly, carrying a balance is significantly more expensive than an installment loan. If you understand this daily calculation, you realize that making a payment even a few days before the due date can reduce the “average daily balance,” thereby reducing the interest charged for that month.

Tools and Strategies for Smarter Debt Management

In the modern financial landscape, you don’t necessarily need a PhD in mathematics to figure out your interest. However, knowing which tools to use and how to interpret their results is a key component of financial literacy.

Leveraging Online Loan Calculators and Spreadsheets

For complex amortized loans, manual calculation can become tedious. Financial professionals and savvy consumers often use Amortization Schedules. Most spreadsheet software (like Excel or Google Sheets) has built-in functions such as =PMT (to calculate the payment) and =IPMT (to calculate the interest portion of a specific payment).

Using an online calculator allows you to perform “what-if” scenarios. For instance, you can see exactly how much interest you would save by increasing your monthly payment by $100. Seeing the visual decline of the interest portion on a chart can be a powerful motivator for debt repayment.

The Impact of Extra Payments on Total Interest

One of the most effective ways to “beat” the interest calculation is to pay more than the minimum. Because interest is calculated based on the current principal balance, any extra payment made directly to the principal reduces the base for all future interest calculations.

This is the logic behind the Debt Avalanche method. By focusing extra payments on the loan with the highest interest rate, you minimize the total interest paid across all your debts. Even one extra mortgage payment per year can shave years off the loan term and save tens of thousands of dollars in interest, effectively giving you a massive “return” on your money.

How Loan Terms and Credit Scores Influence Interest Costs

Figuring out the interest on a loan isn’t just about the math; it’s about understanding the variables that determine the rate you are offered in the first place.

Fixed vs. Variable Interest Rates

When you secure a loan, you must choose between a Fixed Rate and a Variable (or Floating) Rate.

- Fixed Rates remain the same for the duration of the loan. This provides stability and makes it easy to figure out exactly how much interest you will pay over the life of the loan.

- Variable Rates are tied to an index (like the Prime Rate). If the index goes up, your interest rate and monthly payment go up. While variable rates often start lower than fixed rates, they carry the risk of becoming significantly more expensive if the economy shifts.

The Long-Term Cost of Longer Loan Terms

Borrowers are often tempted by 72-month car loans or 30-year mortgages because they offer lower monthly payments. However, when you calculate the total interest, these longer terms are far more expensive.

For example, a $30,000 car loan at 7% interest:

- 60-month term: Total interest paid is roughly $5,645.

- 72-month term: Total interest paid is roughly $6,835.

While the 72-month payment is lower, you pay nearly $1,200 more for the same car. When figuring interest, always look at the Total Cost of Borrowing, not just the monthly obligation. Your credit score also plays a pivotal role here; a “Prime” score (720+) can result in interest rates several percentage points lower than “Subprime” scores, which can be the difference between a manageable debt and a financial burden.

By understanding these calculations and the factors that drive them, you move from being a passive borrower to an active manager of your personal wealth. Interest is a powerful tool when you are the one earning it, but when you are the one paying it, knowledge is your only defense against unnecessary costs.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.