In the evolving landscape of personal finance, the agility to move your capital is just as important as the ability to save it. Whether you are chasing higher yields at a digital-first neobank, consolidating your assets to simplify your mental load, or fleeing predatory fee structures, knowing how to close a savings account properly is a fundamental financial skill.

Closing an account is rarely as simple as withdrawing the cash and walking away. It requires a methodical approach to ensure that no “zombie” transactions occur, no interest is left on the table, and your credit reputation remains untarnished. This guide provides a professional roadmap for navigating the closure process while optimizing your broader financial strategy.

1. Evaluating the Strategic Necessity of Closing an Account

Before initiating the closure process, it is vital to analyze the “why” behind the move. Personal finance is not just about the numbers; it is about the efficiency of the systems you use to manage those numbers.

Identifying Better Interest Rates and Yields

The most common driver for closing a savings account is the search for a higher Annual Percentage Yield (APY). In a fluctuating interest rate environment, traditional “brick-and-mortar” banks often lag behind online-only institutions. If your current account is yielding 0.01% while High-Yield Savings Accounts (HYSAs) are offering 4.00% or more, the opportunity cost of staying is too high. Closing the old account is a proactive step toward inflation-hedging your liquid assets.

Consolidating Accounts for Simplified Management

“Financial sprawl” occurs when an individual has too many accounts across too many institutions. This fragmentation makes it difficult to track net worth, increases the risk of missing a statement, and complicates tax preparation. Strategically closing redundant accounts allows for a “cleaner” financial dashboard, reducing the cognitive overhead required to manage your money.

Avoiding Fees and Inactivity Penalties

Many traditional banks require a minimum daily balance to waive monthly maintenance fees. If your financial situation has changed and you can no longer maintain that balance, the account becomes a liability rather than an asset. Furthermore, many institutions charge “dormancy fees” if an account sees no activity for 6 to 12 months. Closing the account prevents these unnecessary erosions of your capital.

2. Essential Pre-Closure Preparations

Closing an account is a surgical procedure that requires preparation to avoid “bleeding” in the form of missed payments or lost interest.

Establishing the New “Financial Home”

Never close your primary or secondary savings account until the new account is fully operational. This includes verifying the new account, setting up login credentials, and ensuring the mobile app or web interface meets your needs. You want to ensure there is a seamless “bridge” for your capital to cross.

Auditing Automatic Transfers and Linked Accounts

Savings accounts are often the “engine room” for automated financial goals. Review your transaction history for the last 12 months to identify:

- Automated transfers from checking to savings.

- Direct deposits (if your employer splits your paycheck).

- Linked investment accounts (like Vanguard or Fidelity) that pull from or push to this specific account.

- Subscription services or utility bills that might be tied to the account’s routing number.

Update these links to your new account at least one full billing cycle before closing the old one.

The “Trailing Interest” Strategy

One of the most common mistakes is withdrawing the full balance on the 20th of the month and requesting an immediate closure. Interest is typically calculated daily but credited monthly. If you close the account mid-cycle, you may forfeit the interest earned during those 20 days. Professional strategy dictates moving the bulk of the funds but leaving a small buffer until the final interest payment hits, then closing the account immediately after.

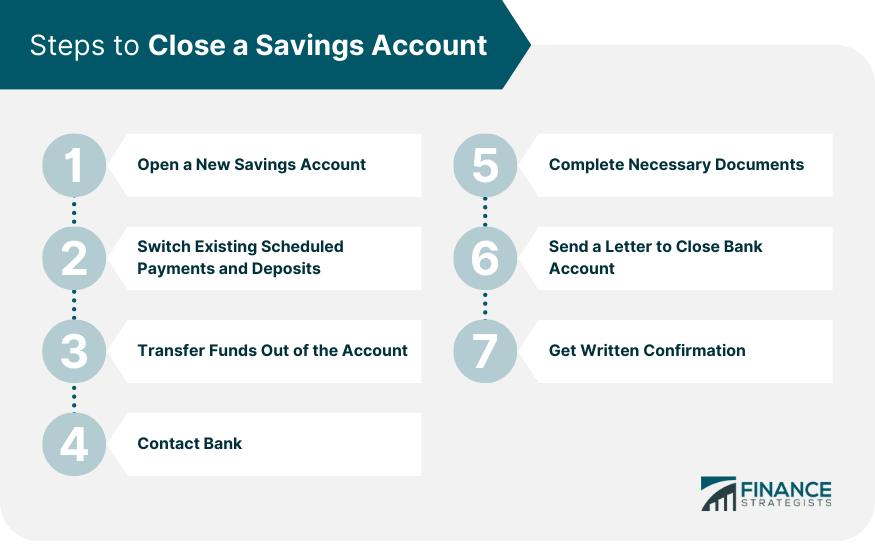

3. The Execution: Step-by-Step Account Termination

Once your “bridge” is built and your automated systems are rerouted, it is time to execute the closure.

Moving the Final Balance to Zero

The cleanest way to close an account is to transfer the remaining balance (minus any “buffer” for trailing interest) via an Electronic Funds Transfer (EFT) or ACH transfer to your new institution. While you can request a physical check, this often involves “check-cutting fees” and mail delays. An electronic transfer is faster and provides a digital paper trail.

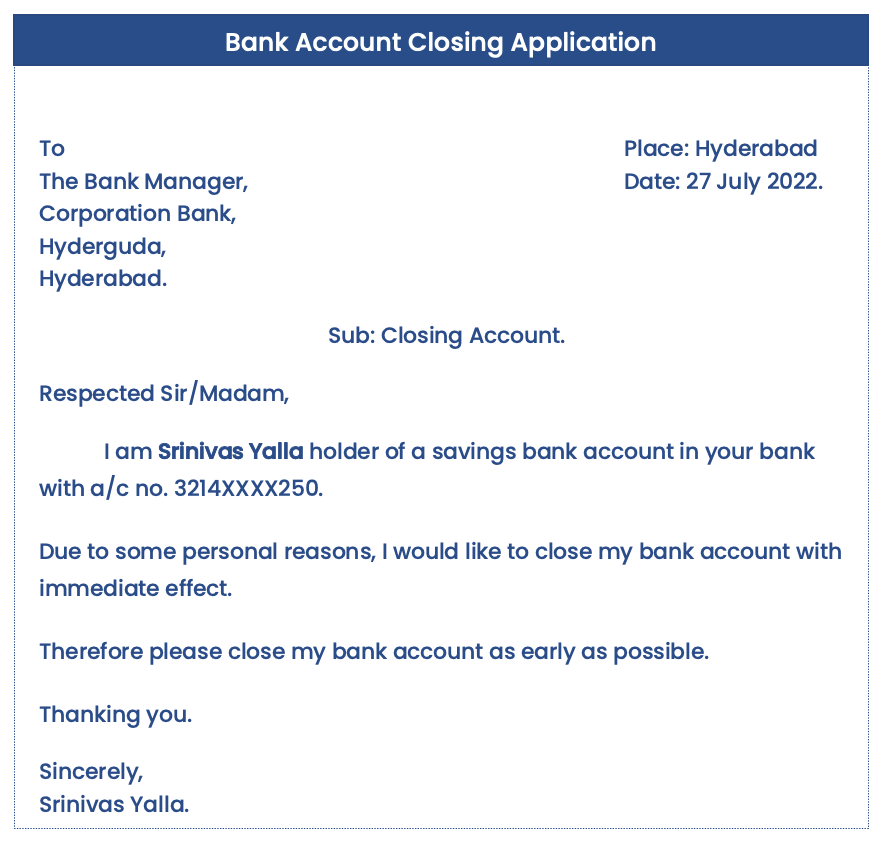

Initiating the Formal Closure Request

Simply leaving a balance of $0.00 does not close an account. In fact, an empty account can sometimes trigger “overdraft” fees if a stray automated charge hits it, or it can be flagged as “inactive,” leading to fees that put the balance into the negative.

You must contact the bank through one of three professional channels:

- In-Person: Visit a branch and speak with a personal banker. This is the fastest way to get a signed receipt of closure.

- Secure Message/Online Portal: Many modern banks allow you to close accounts via their authenticated chat or messaging systems.

- Phone: Call the customer service line. Be prepared for a “retention script” where the representative offers incentives to stay. Be firm and stick to your decision.

Requesting Written Confirmation

Verbal confirmation is insufficient for significant financial moves. Always request a “Letter of Account Closure.” This document is your shield if the bank later claims the account is open and delinquent, or if there is an error reported to ChexSystems (the “credit bureau” for bank accounts). Keep this digital or physical copy for at least five years for your records.

4. Navigating Potential Pitfalls and Misconceptions

Closing a savings account involves nuances that, if ignored, can lead to unexpected financial friction.

Understanding the Impact on Credit Scores

A common myth is that closing a savings account will hurt your credit score. Unlike credit cards, where “age of accounts” and “utilization” are key factors in your FICO score, savings accounts are not reported to the major credit bureaus (Equifax, Experian, and TransUnion). However, they are reported to ChexSystems. As long as you close the account with a positive or zero balance, your ChexSystems report will remain healthy, ensuring you can easily open accounts in the future.

Dealing with Early Withdrawal Penalties

If the account you are closing is a Certificate of Deposit (CD) or a specialized Money Market Account, you may face “Early Withdrawal Penalties.” These penalties often equate to several months of interest. Professionally, you must calculate whether the higher interest rate at a new bank outweighs the penalty fee of leaving the current one early. If the “break-even” point is more than a few months away, it may be wiser to wait until the CD matures.

Managing Joint Accounts and Beneficiaries

Closing a joint account usually requires the consent or notification of both parties. If the account has a “Payable on Death” (POD) or “Transfer on Death” (TOD) beneficiary, that designation will be extinguished upon closure. Ensure that your new account has updated beneficiary information to maintain your estate planning strategy.

5. Post-Closure Best Practices and Security

The process is not complete until you have secured your data and prepared for the next tax season.

Secure Disposal of Banking Tangibles

If the savings account was linked to a specific ATM card or if you had a dedicated checkbook for the account, these must be destroyed. Use a cross-cut shredder for checks and a dedicated card-shredding tool for plastic. Even an “inactive” card contains data that could be exploited in a data breach.

Record Keeping for Tax Obligations (1099-INT)

Even if you close an account in January, the bank is legally required to issue a Form 1099-INT the following year if you earned more than $10 in interest. When you close the account, ensure the bank has your current mailing address or that you have downloaded all previous statements. Failing to report this interest to the IRS can lead to unnecessary audits or penalties.

Monitoring for “Zombie” Reactivations

In rare cases, a stray ACH credit (like a forgotten tax refund) can automatically “re-open” a closed account. Monitor your email for any communications from the old bank for 60 days following the closure. If you see activity, contact the bank immediately to reject the transfer and re-close the account.

Conclusion: Mastering Your Financial Fluidity

Closing a savings account should not be viewed as an administrative burden, but as an act of financial stewardship. By systematically evaluating your needs, preparing your transfers, and securing formal documentation, you ensure that your capital is always positioned in the most advantageous environment.

In the modern era of finance, your loyalty should belong to your financial goals, not to a specific banking institution. Mastering the art of the “clean exit” allows you to remain agile, minimize fees, and maximize the growth of your personal wealth. Whether you are consolidating for simplicity or pivoting for profit, a professional approach to closing an account is a hallmark of a sophisticated financial mind.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.