Understanding how to calculate your salary is more than just a basic math exercise; it is a fundamental pillar of personal finance and career management. For many professionals, the number discussed during a job interview or written in an employment contract feels abstract until it actually hits their bank account. However, there is often a significant discrepancy between the “sticker price” of a salary and the actual liquidity an individual possesses at the end of the month.

Mastering the nuances of salary calculation allows you to budget effectively, negotiate better raises, and plan for long-term financial milestones such as home ownership or retirement. This guide provides a deep dive into the mechanics of compensation, breaking down the variables that transform a gross figure into a net reality.

Understanding the Foundation: Gross vs. Net Salary

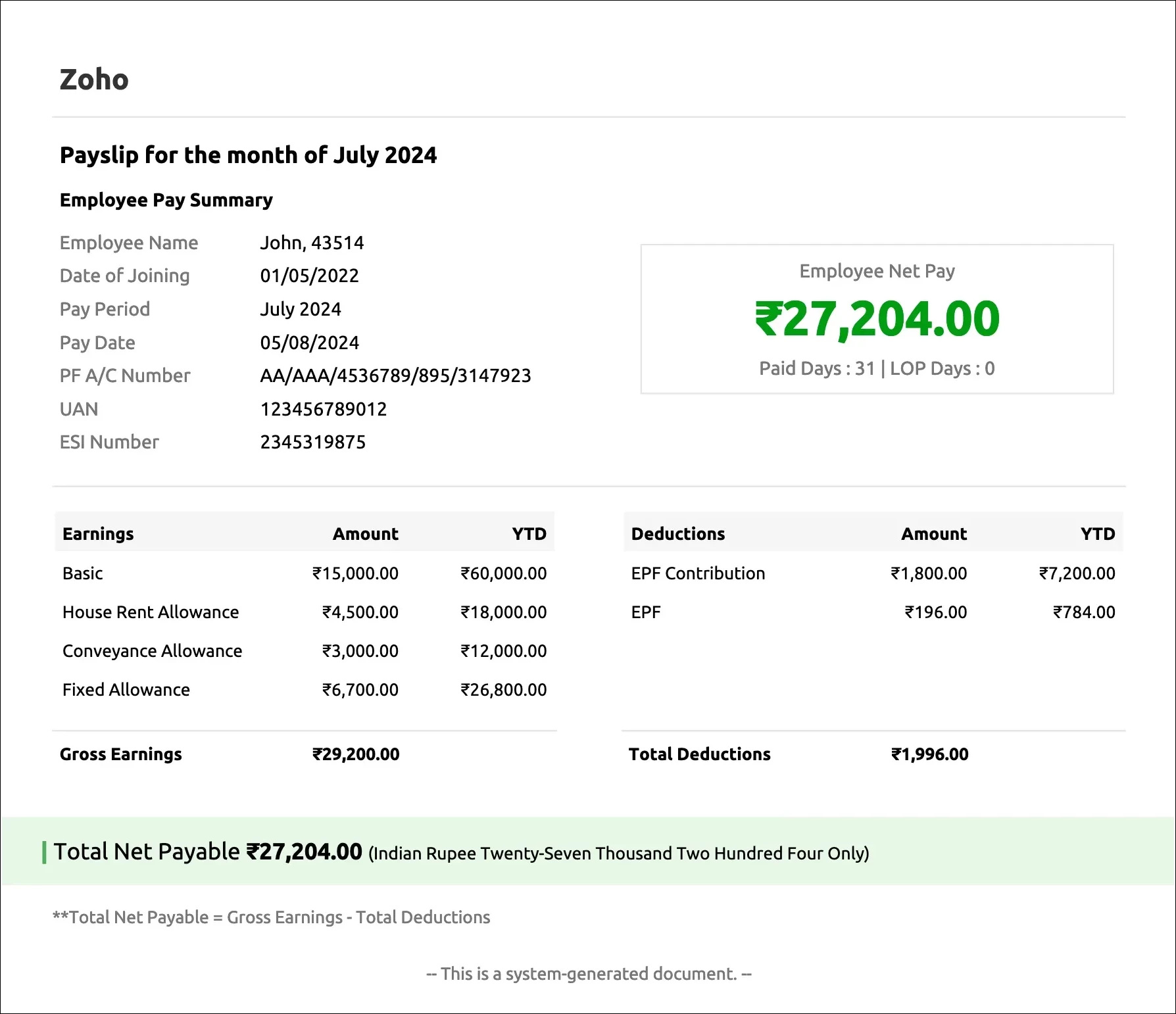

Before diving into formulas, one must distinguish between the two most critical terms in business finance: Gross Salary and Net Salary. This distinction is the primary reason why many employees feel a sense of “sticker shock” when they receive their first paycheck.

Defining Gross Income

Gross income is the total amount of money an employer pays an employee before any deductions are taken out. If a job posting offers $80,000 per year, that $80,000 is your gross salary. For salaried employees, this is usually divided by the number of pay periods in a year. For hourly employees, gross income is calculated by multiplying the hourly rate by the number of hours worked, including any overtime premiums. It is important to remember that while gross income is the figure used for loan applications and credit checks, it is not the amount available for your daily expenses.

The Transition to Net Pay

Net pay, commonly referred to as “take-home pay,” is the amount remaining after all mandatory and voluntary deductions have been subtracted from the gross income. This is the actual amount deposited into your bank account. The “gap” between gross and net is comprised of federal, state, and local taxes, insurance premiums, and retirement contributions. Understanding this transition is vital for accurate budgeting; if you build a lifestyle based on your gross income, you will quickly find yourself in a deficit.

Fixed vs. Variable Components

Salary is not always a static number. Many compensation packages include fixed components (base salary) and variable components (bonuses, commissions, or shift differentials). When calculating your projected income, it is safer to base your essential living expenses on the fixed component while treating variable pay as a vehicle for savings or debt repayment. Overestimating variable income is a common financial pitfall that can lead to cash flow issues during “slow” months.

The Step-by-Step Calculation Process

To calculate your salary accurately, you must move beyond simple division and account for the calendar and the regulatory environment.

Determining Annual, Monthly, and Hourly Rates

The first step is establishing your baseline. If you are a salaried employee, your monthly gross is your annual salary divided by 12. However, if you are paid bi-weekly (every two weeks), you will have 26 pay periods, meaning two months out of the year will feature three paychecks.

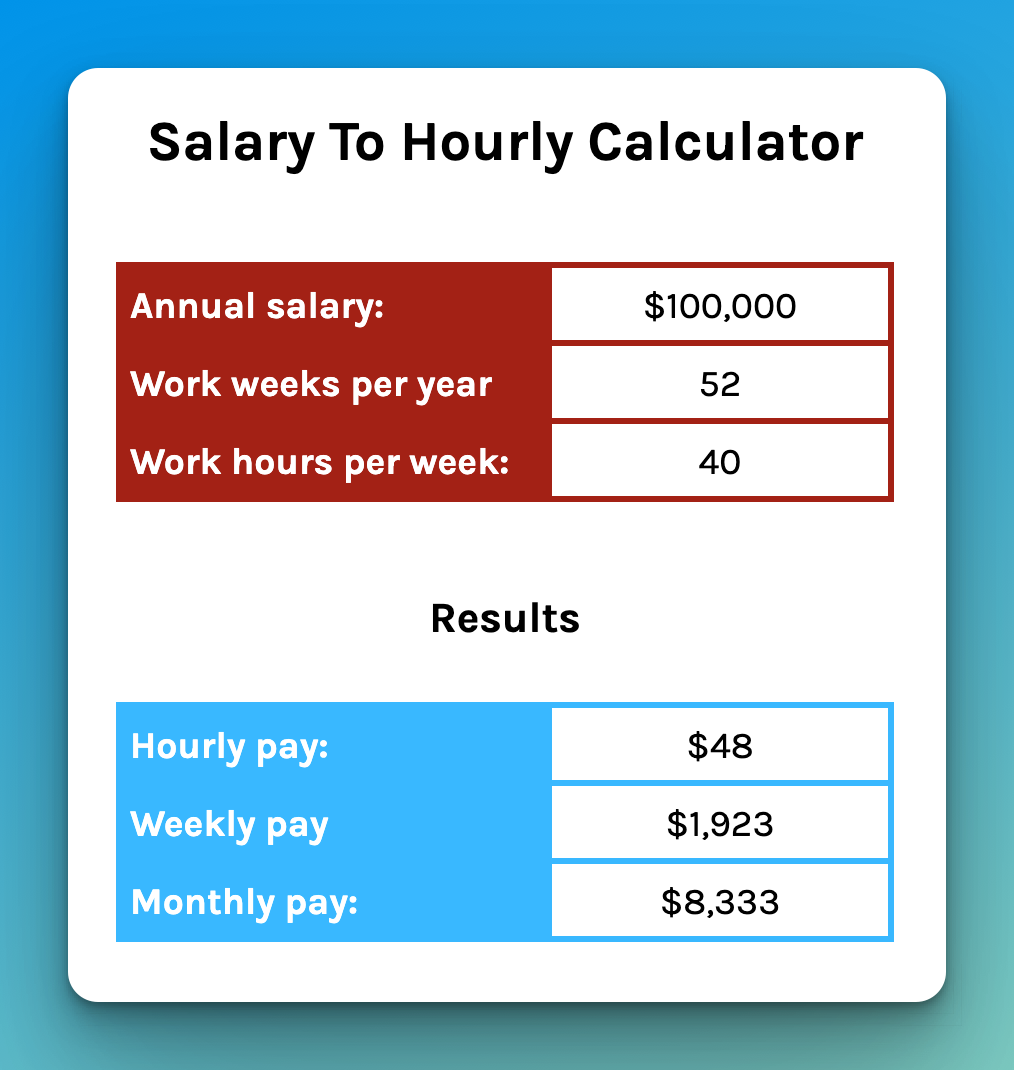

To find your hourly equivalent from an annual salary, the standard professional formula is to divide the annual gross by 2,080 (the number of work hours in a year based on a 40-hour week). Conversely, if you are an hourly worker looking to find your annual salary, multiply your hourly rate by 2,080. This baseline allows you to compare different job offers on an “apples-to-apples” basis.

Accounting for Mandatory Tax Deductions

Taxes are the largest variable in the salary equation. In most jurisdictions, employers are required to withhold income tax at the source. This is often a progressive system, meaning as your income increases, the percentage of tax you pay on the next dollar earned also increases.

- Federal Income Tax: Based on your tax bracket and filing status.

- State and Local Taxes: These vary wildly depending on your geography; some regions have no state income tax, while others have significant local levies.

- Payroll Taxes: In the United States, for example, FICA (Federal Insurance Contributions Act) taxes cover Social Security and Medicare, typically taking a flat percentage out of your gross pay.

Factor in Social Security and Retirement Contributions

Beyond government taxes, your “net” is influenced by your future self. Contributions to retirement accounts, such as a 401(k) or a private pension fund, are often deducted directly from your paycheck.

- Pre-Tax Deductions: These are taken out before taxes are calculated, which actually lowers your taxable income and can save you money in the long run.

- Post-Tax Deductions: These are taken out after taxes have been applied.

Calculating these amounts accurately requires looking at your contribution percentage and determining if your employer offers a “match,” which is essentially free money added to your total compensation, even if it doesn’t show up in your immediate take-home pay.

Benefits and Perks: The “Total Compensation” Perspective

When calculating salary, focusing solely on the cash deposit is a mistake. Professional financial planning requires looking at “Total Compensation”—the sum of your salary plus the dollar value of all benefits provided by your employer.

Health Insurance and Non-Monetary Benefits

For many, the employer-sponsored health insurance plan is a massive financial asset. If an employer pays $500 a month toward your premium, that is $6,000 of annual value that you do not have to pay out of pocket. Other benefits to quantify include dental and vision insurance, life insurance, disability coverage, and even wellness stipends. When comparing two job offers—one with a $90k salary and high premiums, and another with an $85k salary and $0 premiums—the lower salary might actually result in higher net wealth.

Bonuses, Commissions, and Performance Pay

Variable pay structures are common in sales, executive roles, and the tech sector. To calculate these into your annual outlook, look at historical data. Does the company typically pay out 100% of the target bonus? It is important to note that bonuses are often taxed at a “supplemental” rate, which can be higher than your standard withholding rate. This can lead to a smaller-than-expected check in the short term, though the excess tax is usually reconciled when you file your annual tax return.

Equity and Stock Options

In modern corporate finance, equity is a major component of salary calculation. Whether through Restricted Stock Units (RSUs) or Employee Stock Purchase Plans (ESPPs), owning a piece of the company can exponentially increase your net worth. However, calculating the value of equity is complex because it is subject to vesting schedules (you have to stay at the company for a certain period to “earn” it) and market volatility. Financial experts suggest viewing equity as a long-term investment rather than a liquid salary component.

Managing and Negotiating Your Worth

Once you understand how to calculate your current and potential salary, you can use that data to improve your financial standing. Knowledge is leverage in the world of business finance.

Tools and Calculators for Financial Accuracy

While manual calculations are great for understanding the logic, digital financial tools and salary calculators are essential for precision. Many online platforms allow you to input your specific zip code, filing status, and 401(k) contribution percentage to see an exact replica of what your paycheck will look like. Using these tools before accepting a new job offer ensures that you aren’t surprised by the impact of local taxes or insurance costs.

How to Budget Based on Your Final Calculation

The primary purpose of knowing your net salary is to create a functional budget. The “50/30/20 rule” is a popular framework: 50% of your net income goes to needs (rent, utilities, groceries), 30% to wants, and 20% to savings and debt repayment. If your salary calculation reveals that your “needs” are consuming 70% of your take-home pay, you know that you either need to reduce expenses or negotiate a higher salary to maintain financial health.

Leveraging Salary Data for Career Growth

Equipped with a clear understanding of your total compensation, you are better prepared for annual reviews. Instead of asking for a “raise,” you can speak in terms of market value and total packages. For example, if you know your net pay has stayed stagnant while your responsibilities have increased, you can use salary benchmarks to argue for a gross salary increase that offsets inflation and rising insurance costs. Understanding the math behind your paycheck transforms you from a passive recipient of income into an active manager of your financial future.

In conclusion, calculating salary is an essential skill that bridges the gap between earning and building wealth. By deconstructing your pay into gross, net, and total compensation, you gain the clarity needed to make informed decisions about your career, your lifestyle, and your long-term financial security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.