The dream of retirement often conjures images of leisure, travel, and pursuing long-held passions, unburdened by the demands of a daily job. However, transforming this dream into a tangible reality requires diligent planning and, most critically, a precise understanding of your financial needs. Calculating your retirement fund isn’t a one-time exercise; it’s a dynamic process that evolves with your life, market conditions, and personal aspirations. This guide will walk you through the essential steps, methodologies, and considerations to accurately estimate the nest egg you’ll need to secure your financial freedom in your golden years.

Laying the Foundation: Understanding Your Retirement Vision

Before you can crunch any numbers, you need a clear vision of what retirement looks like for you. Your desired lifestyle will be the primary driver of your financial requirements.

Defining Your Retirement Lifestyle and Expenses

Begin by painting a detailed picture of your ideal retirement. Will you stay in your current home, downsize, or relocate to a warmer climate? Do you envision extensive international travel, or a more sedate life of gardening and local activities?

Consider your current spending habits and how they might change. Some expenses, like commuting, work-related clothing, and mortgage payments (if paid off), might decrease or disappear. Others, like healthcare, leisure, and potentially insurance, could increase. It’s helpful to categorize your future expenses:

- Fixed Expenses: Housing (property taxes, insurance, maintenance), utilities, groceries, transportation, basic healthcare.

- Discretionary Expenses: Travel, hobbies, dining out, entertainment, gifts, support for family.

Many financial planners suggest aiming to replace 70-80% of your pre-retirement income. However, this is a general guideline. A more accurate approach is to create a realistic retirement budget based on your envisioned lifestyle.

Pinpointing Your Retirement Age and Horizon

Your retirement age significantly impacts the calculation. Retiring earlier means fewer years to save and more years to fund your expenses. Conversely, working longer allows your savings to compound further and shortens the period you’ll be drawing from your nest egg.

Equally important is estimating your life expectancy. While no one has a crystal ball, modern medicine and healthier lifestyles mean people are living longer. It’s prudent to plan for living well into your 80s or even 90s, especially if you have a family history of longevity. The longer your expected retirement period, the larger your fund needs to be.

Factoring in Inflation and Healthcare Costs

Two critical elements that can erode your purchasing power in retirement are inflation and healthcare costs.

- Inflation: The rising cost of goods and services over time means that a dollar today will buy less in the future. A common long-term average inflation rate used in financial planning is 3%. Failing to account for inflation means your retirement savings might not stretch as far as you anticipate. For example, if you need $50,000 per year today, you’ll need significantly more in 20 or 30 years to maintain the same lifestyle. Your calculations must use future dollar values for expenses.

- Healthcare Costs: Healthcare expenses tend to increase significantly with age and often outpace general inflation. Medicare covers a portion of costs, but it doesn’t cover everything, like dental, vision, or long-term care. You’ll likely need supplemental insurance or have significant out-of-pocket expenses. It’s wise to budget a substantial amount specifically for healthcare in retirement, potentially considering long-term care insurance.

The Core Calculation: Estimating Your Retirement Nest Egg

Once you have a clear understanding of your future expenses and timeline, you can begin to estimate the total capital you’ll need.

The “Multiple of Income” Rule of Thumb

A straightforward, though less precise, method is the “multiple of income” rule. Various financial institutions offer guidelines, such as:

- By age 30: Have 1x your salary saved.

- By age 40: Have 3x your salary saved.

- By age 50: Have 6x your salary saved.

- By age 60: Have 8x your salary saved.

- By retirement (67): Have 10x your salary saved.

While useful for quick checks, this method doesn’t account for individual spending habits, desired retirement age, or specific income sources beyond personal savings.

The “Expense-Based” Method: A Deeper Dive

This method is more accurate as it directly links your savings goal to your projected retirement expenses.

- Calculate Annual Retirement Expenses (in Future Dollars): Based on your detailed budget, estimate your annual expenses in the year you retire, adjusting for inflation.

- Example: If current annual expenses are $60,000, and you plan to retire in 25 years with a 3% inflation rate, your annual expenses at retirement will be approximately $125,487 ($60,000 * (1 + 0.03)^25).

- Determine Your Retirement Income Gap: Subtract any guaranteed income sources (Social Security, pensions, rental income) from your projected annual expenses.

- Example: If future annual expenses are $125,487 and you expect $30,000 from Social Security, your income gap is $95,487 ($125,487 – $30,000). This is the amount your personal savings must generate annually.

- Apply a Safe Withdrawal Rate: This is where the 4% Rule (discussed next) comes into play. If you plan to withdraw 4% of your portfolio each year, you can reverse-engineer the required nest egg.

- Example: If you need $95,487 annually and plan a 4% withdrawal rate, your required nest egg is $95,487 / 0.04 = $2,387,175.

Incorporating Expected Investment Returns

Your investments play a crucial role in growing your retirement fund. The rate of return your investments earn can significantly impact how much you need to save periodically.

- Conservative Estimates: It’s generally wise to use conservative estimates for long-term investment returns (e.g., 5-7% annually, adjusted for inflation if working with real returns). This accounts for market fluctuations and ensures you don’t overproject your growth.

- Asset Allocation: Your asset allocation (mix of stocks, bonds, cash) will determine your expected return and risk level. As you approach retirement, you might shift towards a more conservative portfolio.

Accounting for Social Security and Pensions

Don’t overlook these vital income streams.

- Social Security: You can get an estimate of your future Social Security benefits by creating an account on the Social Security Administration’s website (ssa.gov). Your benefit amount depends on your earning history and the age you claim benefits. Claiming earlier (age 62) results in reduced benefits, while delaying (up to age 70) results in increased benefits.

- Pensions: If you’re fortunate enough to have a defined-benefit pension plan, understand how it calculates your benefit and when you’re eligible to receive it.

These income sources directly reduce the amount your personal savings need to generate.

Popular Methodologies and Rules of Thumb

Several widely cited guidelines can help benchmark your progress, though they are not without their caveats.

Demystifying the 4% Rule

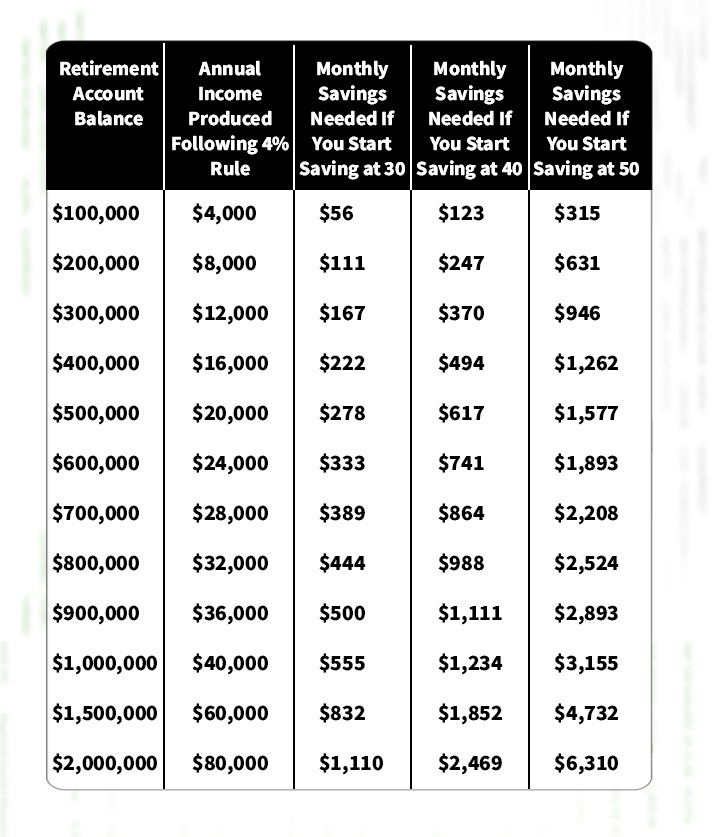

The “4% Rule” is a widely discussed guideline for safe retirement withdrawals. It suggests that if you withdraw 4% of your initial retirement portfolio value in the first year of retirement, and then adjust that dollar amount annually for inflation, your money has a high probability of lasting 30 years.

- How it works: If you have a $1,000,000 portfolio, you withdraw $40,000 in the first year. In subsequent years, you increase that $40,000 by the inflation rate.

- Origins: Based on historical market data (stocks and bonds) in the U.S. and popularized by financial planner William Bengen.

- Limitations: The 4% rule assumes a diversified portfolio, a 30-year retirement horizon, and doesn’t account for extreme market conditions (like sustained low returns or high inflation). Many advisors now suggest a more dynamic approach or a slightly lower withdrawal rate (e.g., 3-3.5%) given current interest rate environments and longer life expectancies.

The 25x Annual Expenses Guideline

Closely related to the 4% rule, this guideline states that you need to save 25 times your annual retirement expenses (the amount your personal savings needs to cover). This is simply the inverse of the 4% rule (1 / 0.04 = 25).

- Example: If your annual retirement expenses (covered by your savings) are $80,000, you would need $80,000 x 25 = $2,000,000 saved.

This is a powerful and easy-to-remember benchmark.

Understanding Safe Withdrawal Rates

The concept of a “safe withdrawal rate” acknowledges that the 4% rule is just one simplified model. A safe withdrawal rate is the percentage of your portfolio you can withdraw annually without running out of money, typically over a 30-year period. Factors influencing a safe withdrawal rate include:

- Portfolio composition: A higher stock allocation generally supports a higher withdrawal rate, but also carries more risk.

- Market conditions: Entering retirement during a bear market (sequence of returns risk) can significantly impact your portfolio’s longevity.

- Flexibility: Being willing to reduce spending during market downturns can enable a higher initial withdrawal rate.

- Retirement duration: Planning for a longer retirement might necessitate a lower withdrawal rate.

Many modern financial planners use Monte Carlo simulations to test various withdrawal rates against thousands of possible market scenarios to determine a personalized “safe” rate.

Tools and Resources for Accurate Projections

You don’t need to be a math wizard to calculate your retirement needs. Numerous tools and resources can help.

Leveraging Online Retirement Calculators

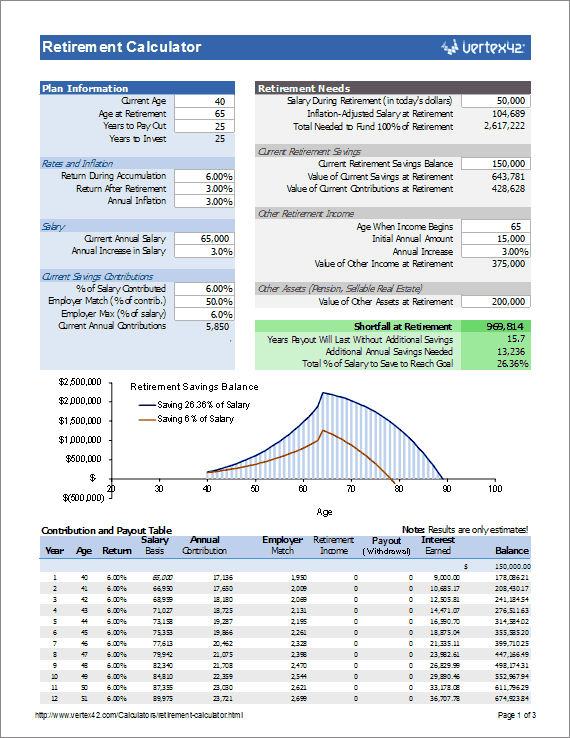

The internet offers a plethora of free retirement calculators from financial institutions, investment firms (e.g., Fidelity, Vanguard), and independent financial planning sites. These tools often allow you to input your current age, desired retirement age, current savings, annual contributions, expected returns, and estimated retirement expenses. They can provide a quick estimate of whether you’re on track or how much more you need to save.

- Pros: Easy to use, provide quick estimates, often interactive.

- Cons: Rely on generalized assumptions, may not account for all personal nuances, can be overly simplistic.

The Power of Personal Spreadsheets

For those comfortable with numbers, a spreadsheet (Excel, Google Sheets) offers unparalleled flexibility. You can build a customized model that precisely reflects your unique situation, including:

- Detailed year-by-year cash flow projections.

- Variable inflation rates for different expense categories.

- Specific tax considerations in retirement.

- Modeling different investment return scenarios.

- Integrating specific income streams like part-time work or annuities.

Creating your own spreadsheet forces a deep engagement with your financial plan.

When to Consult a Financial Advisor

While self-calculation is empowering, a qualified financial advisor brings expertise, objectivity, and advanced tools to the table. They can:

- Help you clarify your retirement vision and conduct a thorough analysis of your projected expenses.

- Develop a personalized financial plan that integrates your current assets, future income, and risk tolerance.

- Utilize sophisticated software for detailed projections, including Monte Carlo simulations.

- Advise on complex issues like tax-efficient withdrawal strategies, estate planning, and long-term care insurance.

- Help you navigate market volatility and keep your plan on track.

For complex financial situations or simply for peace of mind, a certified financial planner (CFP) can be an invaluable partner.

Adjusting and Maintaining Your Retirement Plan

Calculating your retirement needs isn’t a static event; it’s an ongoing process of monitoring and adjustment.

Strategies for Bridging the Gap

If your initial calculations reveal a shortfall, don’t despair. You have several levers you can pull:

- Increase Savings: Automate larger contributions to your 401(k), IRA, or other investment accounts. Even small, consistent increases can make a big difference over time due to compounding.

- Reduce Expenses: Identify areas in your current budget where you can cut back, freeing up more money for savings.

- Delay Retirement: Working a few extra years allows your existing savings more time to grow and reduces the number of years you need to fund your retirement. It also means more contributions to your retirement accounts.

- Increase Income: Explore side hustles, ask for a raise, or consider a career change that offers better compensation.

- Optimize Investments: Review your portfolio to ensure it’s adequately diversified and aligned with your risk tolerance while aiming for reasonable growth.

The Importance of Regular Reviews

Life happens, and your retirement plan needs to adapt. Review your calculations and overall plan at least once a year, or whenever significant life events occur (e.g., marriage, birth of a child, job change, inheritance, major market shift).

Regular reviews allow you to:

- Update your income and expense projections.

- Re-evaluate your investment performance.

- Adjust your contribution amounts.

- Ensure your plan still aligns with your evolving goals and risk tolerance.

Adapting to Life’s Changes

Unforeseen circumstances, such as health issues, caring for aging parents, or market downturns, can impact your financial trajectory. A flexible retirement plan is a resilient one. Be prepared to make adjustments, whether it’s temporarily reducing discretionary spending, exploring part-time work in retirement, or re-evaluating your investment strategy.

Calculating your retirement needs is arguably one of the most critical financial exercises you’ll undertake. It empowers you to take control of your future, providing a roadmap to financial independence. By understanding your vision, applying sound methodologies, utilizing available tools, and regularly reviewing your progress, you can build the confidence and capital required to enjoy the retirement you’ve always envisioned.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.